Chapter 11 - Forms of Ownership

Learning Objectives

At the completion of this chapter, students will be able to do the following:

1) Explain the difference between ownership in severalty and concurrent ownership.

2) Explain the difference between a tenancy in common and joint tenancy.

3) Explain the difference between a condominium and a cooperative.

11.1 Ownership in Severalty

Transcript

As a real estate professional, you will probably come across a variety of different forms of ownership for real estate. In this section, we’ll explore several of those forms.

Real estate may be owned in severalty or may be owned by multiple co-owners who take title together as joint tenants or as tenants in common.

Property may instead be owned by a business, like a partnership, a corporation, an LLC or syndication.

Finally, we’ll explore ownership of condominiums, cooperatives and time-shares. These types of real estate communities may present some differences real estate professionals should understand.

Let’s look at each of these forms of ownership more closely.

Ownership in Severalty

First, ownership in severalty may sound complex, but it’s not. Don’t let the word “severalty” confuse you.

Although it sounds like “several”, when someone owns real estate in severalty, there is just one owner for the property. Instead of associating “severalty” with “several,” try thinking of it as “severed” or separated.

When you have ownership in severalty, one person owns all of the rights that come with owning that piece of real estate. That means they can use the property themselves, allow others to use it or formally lease or rent it to others.

The person who owns the property in severalty can also take out a mortgage against the property, sell it to someone else or transfer it by gifting it to someone else.

Finally, an owner in severalty can also “devise” their real estate, meaning they can leave it to someone else as a bequest in their will after they die. In states where “transfer on death” or “beneficiary” deeds are authorized, the owner of property in severalty has the authority to devise property through the use of those tools too.

It is important to understand that although “severalty” means one owner, that owner does not need to be an individual person. A business entity, or a trust, may also own property in severalty.

One important caveat is that some states provide for a “marital interest” in real estate, even if property is owned only by one spouse. So, even if one spouse owns property in severalty, the other spouse will be required to sign deeds or other conveyances affecting the property, because of their marital status.

Example

Let’s look at a couple of examples of ownership by severalty in action:

Joe and Sally sold their home and executed a quit claim deed to transfer ownership of their home to their friend, John. The deed shows that the grantee is “John Doe, an unmarried person.” John now owns the property in severalty.

Now, let’s assume John was married, but he and his wife decided that her name will not be listed on the title. Even if the quit claim deed shows that the grantee is “John Doe, married to Jane Doe,” John still owns the property in severalty.

Key Terms

Severalty Ownership

Real property that is owned by only one person. Sole ownership.

11.2 Concurrent Ownership

Transcript

Forms of Ownership: Concurrent Ownership

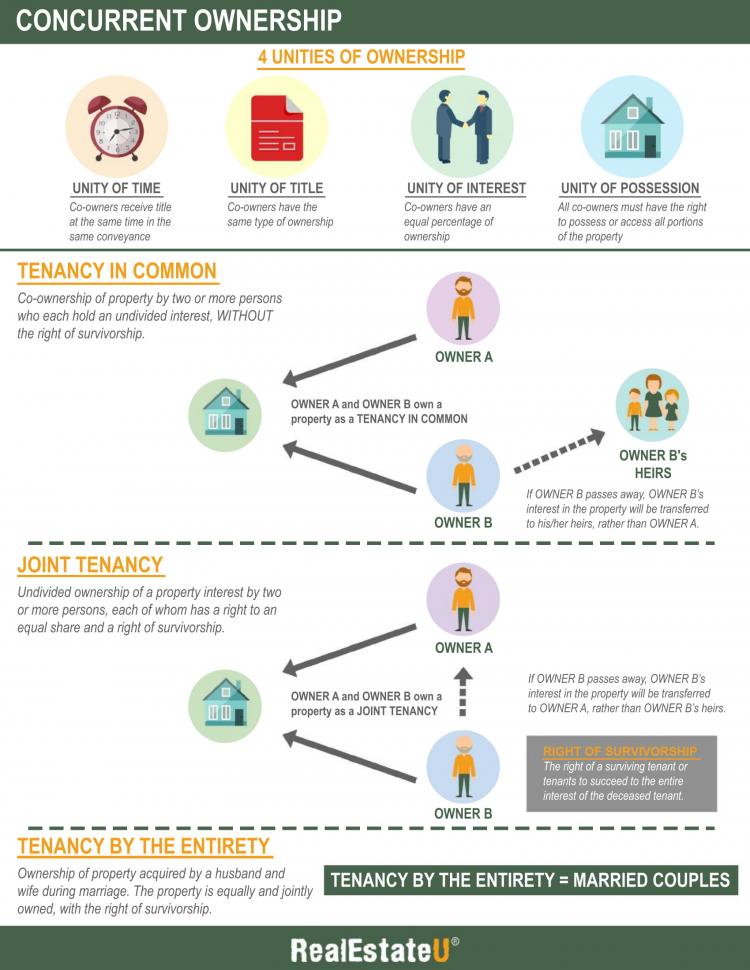

Frequently, real estate is owned by more than one owner. This is referred to as concurrent ownership, and it can take different forms including tenancy in common and joint tenancy with rights of survivorship.

Although “tenancy in common” and “joint tenancy” sound similar to one another, they have some important differences. You should pay close attention in order to understand the distinctions between the different ways multiple people can own real estate together, because it affects a number of things ranging from what happens to real estate when an owner dies, to what happens when real estate owned by more than one party is sold.

Tenancy in Common

When two or more parties own a piece of real estate as tenants in common, each owner owns a divided piece of the overall parcel of real estate. You can imagine a cake, which in this case it will be the property. Each owner will get a piece of cake however the pieces are not necessarily equal as some owners may own a larger portion of the property than the others.

This means that when one owner dies, their share does not automatically pass to the other owners. Instead, the deceased owner’s share will pass according to their Will. Or in case there is no will then it will pass according to state law. In states that allow owners of real estate to create transfer on death deeds, or beneficiary deeds, a tenant in common can use those tools to pass their section of the real estate to one or more named beneficiaries, outside of probate court, at their death.

Tenancy in common is frequently the way property is held when siblings inherited their parents’ property, or when business partners purchase a piece of real estate together.

When multiple people own property as tenants in common, each owner may have a different percentage of ownership. That is to say, they do not need to be equal property owners.

Let’s look at an example of tenancy in common:

John, a widower, who owned a cabin in his name alone, died. His will left all of his assets, including his real estate, to his five children. When the cabin property passes through probate court, the deed transferring title lists each child’s name as a grantee, specifying that each owns an “undivided one-fifth interest” in the property. So, the property is now owned by the five children equally.

However, if one of those children died leaving their property to her four adult children, ownership of the property becomes even more fractionalized.

Each of John’s surviving children still owns their undivided one-fifth interest. The four adult grandchildren (the children of John’s deceased daughter) now own one-fourth of one-fifth, or a one-twentieth share of the real estate.

Joint Tenancy

Joint tenancy is another way more than one party can own real estate together. When parties own real estate as joint tenants, they have the equal, undivided right to sell, mortgage, transfer or encumber their property. No one owner has a greater share than another.

If we come back to our cake analogy, in a joint tenancy every owner will get an equal piece of the cake.

When property is owned in joint tenancy, the deed or title should reflect this.

When property is owned jointly, there are four “unities” of ownership:

- unity of possession,

- unity of interest,

- unity of time …and

- unity of title

Simply put, this means that all of the owners have equal rights and responsibilities for the property.

Property held in joint tenancy has “rights of survivorship.” This means that when one joint owner dies, their share of the property passes by law to the other joint owner(s), rather than passing through their will or other legal document.

Joint tenancy with rights of survivorship is terminated when one owner dies. Also it is terminated if the owners join together to sign and record a deed transferring ownership into someone else’s name. That someone else could be the other joint owner or owners.

Here's an example of joint tenancy that you might encounter when you're working as a real estate professional:

Amy and Chris, a married couple, are buying their first home. They will own it as joint tenants with rights of survivorship so if either one of them dies while owning the home, ownership will pass to the survivor of them, outside of any court proceedings. Let’s assume Amy dies then her property share will automatically be transferred to Chris. Even if Amy and Chris have children Amy’s property share will go to Chris and not to their children.

Termination of Co-Ownership by Partition

A partition, in real estate, refers to a court proceeding that officially severs co-ownership of the parcel of land or property. This may be necessary when there is a disagreement among the owners about how to use, maintain or dispose of the real estate.

Sometimes, when the parties cannot agree to voluntarily partition the real estate, the court will require the owners to sell the property and divide the proceeds.

Tenancy by the Entirety

In some states, there is another option for concurrent ownership: tenancy by the entirety with rights of survivorship. Simply put, property owned by a married couple held as tenancy by the entirety means that both spouses have an equal, and undivided, interest in the real estate.

Tenancy by the entirety functions much like joint tenancy with rights of survivorship for a married couple in those states. That means that when one spouse dies, the ownership of the real estate passes to the surviving spouse.

Tenancy by the entirety is terminated when one spouse dies, or when both spouses join together to transfer ownership to another party. Neither spouse can sell or transfer ownership of the property without the other spouse’s consent.

Community property

There are nine states today that have specific community property laws on their books, designed to protect both spouses in a marriage. These states are commonly referred to as “Community Property states”. Such states include Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin.

Simply put, property owned by married people in any of those nine states is considered property of both, or either, of the spouses.

There are two common exceptions to the community property treatment. The first exception is when property was acquired specifically as a separate property by one of the spouses before the marriage (so it was owned before the marriage by just one of them). In that case it can continue to be held as individual, or separate, property.

The second exception is for real estate or other property that one spouse inherits or receives as a gift in their name alone after the marriage. In most cases, that property can also be treated as separate property, even in a Community Property state.

With community property, each spouse has an equal right to any real estate the couple owns, where with joint tenancy, spouses own the property together in an undivided fashion. With community property essentially, each spouse owns one-half of the property. Neither spouse can sell or transfer ownership without the other spouse agreeing to the transfer.

Let’s look at an example that will make this concept more sense:

Jill and Ken were married and owned their home together in California. Unfortunately, their marriage fell apart and they filed for divorce. Because California is a Community Property state, neither Jill nor Ken could dispose of their share of the property before, or during the court proceeding without the other’s agreement.

And, again, because the state of California is a Community Property state, odds are that the court will divide the real estate 50/50, meaning that both Jill and Ken will receive a one-half share.

Although an attorney is best suited to advise clients on what form of ownership applies best to their case, you might be asked by buyers for some guidance on this issue. As a real estate agent it is generally prudent to never give advice and you should direct your clients to an attorney. Too many agents fall pray at confusing helping clients with giving them legal advice, which is a BIG NO NO. So please do not advise your clients on what type of ownership will suite them best, even if they ask. You can politely recommend an attorney that they can speak with and emphasize the fact that you are there to provide them with guidance regarding the property.

Key Terms

Community Property

Property acquired by husband and/or wife during a marriage when not acquired as the separate property of either spouse. Each spouse has equal rights of management, alienation and testamentary disposition of community property.

Joint Tenancy

Undivided ownership of a property interest by two or more persons each of whom has a right to an equal share in the interest and a right of survivorship, i.e., the right to share equally with other surviving joint tenants in the interest of a deceased joint tenant.

Partition

A division of real or personal property or the proceeds therefrom among co-owners.

Right of Survivorship

The right of a surviving tenant or tenants to succeed to the entire interest of the deceased tenant; the distinguishing feature of a joint tenancy.

Tenancy by the Entireties

Under certain state laws, ownership of property acquired by a husband and wife during marriage, which property is jointly and equally owned. Upon death of one spouse it becomes the property of the survivor.

Tenancy in Common

Co-ownership of property by two or more persons who each hold an undivided interest, without right of survivorship; interest need not be equal.

11.2a Concurrent Ownership Infographic

Please spend a few minutes reviewing the Infographic below.

11.3 Trusts

Transcript

When you hear the words “living trust,” do you automatically think of a tool that’s only for the ultra-wealthy among us? Trusts are actually a common estate planning tool used by all kinds of people – not just those with millions of dollars in assets.

Odds are good that, as a real estate professional, you will encounter transactions where the buyer or the seller is acting as a trustee on behalf of a trust, so it’s important to have a basic understanding of trusts.

Why Are Trusts Used?

Trusts can be used for many purposes. Let’s explore some of the most common reasons.

Number 1 - When someone dies, a probate court proceeding may be necessary to clear title to real estate and other assets.

Probate court can be expensive and time-consuming. In addition, when real estate has to go through probate court, state laws often impose lengthy restrictions on how, and when, that real estate can be sold.

Creating a trust, and making that trust the owner of real estate and other assets, is one way to avoid the expense and hassle of probate court.

Number 2 - Another common reason for using trusts is to make sure that assets will pass according to your wishes after your death.

Trusts can be used to manage from beyond the grave, with assets managed and distributed years or even decades after the original owner’s death. People whose children or other heirs have difficulty managing money may find comfort in being able to control distributions even after death, through a trust.

Number 3 - Blended families often use trusts as an important part of their estate plans. Trusts can be used to ensure a current spouse will have assets they need during their lifetime, while making sure children from previous marriages are protected.

Number 4 - Tax planning is another common reason for using trusts. Through “credit shelter” or “disclaimer” provisions, people may be able to limit the amount of federal and state estate taxes due after their deaths.

These are the most common reasons people create trusts. Some other reasons include providing for a beneficiary who has special needs without jeopardizing their eligibility for government assistance or leaving a charitable legacy.

Understanding the Parties Involved in Trusts

Sometimes the terminology of trusts can be confusing, but don’t let the “legalese” confuse you.

The person creating the trust is called the “grantor”, the “trustor” or the “settlor.” This may be an individual, or a couple.

The people who will inherit trust assets are referred to as the beneficiaries.

As a real estate professional, you will likely come into contact with the trustee. The trustee is the person or company charged with managing the trust assets.

The trustee is often the same person (or people) as the grantor. This is often the case when someone prepares a living trust to hold assets in order to avoid probate court. When real estate is inside of a trust, the owner will sign documents in their official capacity as trustee, rather than as an individual property owner.

The trustee may be another family member, or even a professional trust company or other professional fiduciary. The trust document itself will identify who has the authority to act as trustee.

Understanding Different Types of Trusts

Just as there are many different reasons for creating trusts, you should also know that there are different types of trusts.

Living trusts are trusts created by the grantor during his or her lifetime. After creating the trust, the grantor transfers ownership of some, or, all of their assets into the trust, to be managed according to the terms of the trust by the trustee.

Testamentary trusts, on the other hand, are trusts that do not actually exist until the grantor dies. The terms of the trust, including who will serve as trustee, the identity of beneficiaries and how assets should be managed and distributed are all spelled out in the grantor’s will, rather than in a separate trust agreement. Testamentary trusts are most commonly used when people want to provide for their minor children in the event of the parents’ premature deaths.

Understanding Land Trusts

As a real estate professional, you will likely also encounter land trusts at some point.

A land trust is a specific type of living trust specifically used to hold title to real estate for the benefit of someone else. People creating land trusts may want to safeguard their privacy and protect their real estate from liens, title claims, homeowners’ association claims or other litigation.

Putting it Into Practice

Now that we’ve explored what trusts are and how they work, let’s look at an example of how you might encounter trusts when you’re working as a real estate professional.

Example Number 1:

John and Jane Doe want you to help them sell their house. When you review the property deed, you see that the house is owned by:

John Doe, as Trustee for the John Doe Living Trust under agreement dated January 1st 2010.

This tells you that John and Jane do not actually own the home as joint tenants or tenants in common. Instead, John established a living trust on January 1st 2010 that owns the home. So, assuming John is not incapacitated, he will sign the purchase agreement and closing documents as trustee, rather than as an individual.

In the event John is incapacitated, the trust agreement should specify who will serve as trustee in his stead. John’s attorney can provide a certificate of trust to document who has legal authority to act, and whether or not there are any restrictions on that person’s (or company’s) actions as trustee.

Example Number 2:

Sally Smith, a wealthy celebrity, created a land trust on the advice of her attorney, to limit exposure and legal liability.

Sally wants to buy a new mansion. Rather than dealing with Sally, you will instead be working with her trustee, a professional trust company, who will be the nominal buyer on behalf of Sally’s land trust.

You do not need to be an expert on trust law to be a successful real estate professional, but this introduction to how trusts work should help you when you encounter them in real life.

Key Terms

Beneficiary

The recipient of a gift of personal property by will.

Land Trust

A legal agreement where a trustee is appointed to maintain ownership of a piece of real property for the benefit of another party.

Living Trust

An agreement where the trustee holds the legal possession of an asset (e.g. real estate) that belongs to another person, the beneficiary, and it is created while the person is alive.

Testamentary Trust

A trust which arises upon the death of the testator, and which is specified in his or her will.

Trust

A legal relationship under which title to property is transferred to a person known as a trustee.

Trustee

A person who holds title to property for the benefit of another called a beneficiary.

Trustor

A person who conveys title to a trustee.

11.4 Partnerships

Transcript

Partnerships

A partnership is a form of business ownership where two or more people share in the profits, and the liabilities, for the business. There are two main types of partnerships: general partnerships, and limited partnerships.

In a general partnership, all of the partners participate in the day-to-day operations of the business. Some of the kinds of businesses that are frequently established as general partnerships include law firms, medical or dental clinics and consulting firms.

This is different from a limited partnership. In a limited partnership, one (or more) of the partners is a partner on paper, with a financial stake in the business, however he or she is not directly involved in running the business. That person is the limited partner. The partners actually running the business are referred to as general partners. This is often the case when someone wants to start and run a business but does not have the financial wherewithal to do so. A limited partner can add additional capital to help the business owner run the business without being involved on a daily basis. A limited partner is also not responsible for contributing more capital to keep the business going.

In either type of partnership, the business will have legal documents establishing the percentage of ownership and voting rights each partner has in the company. When a partnership owns real estate, it is typically owned in the name of the partnership alone.

Let's look at an example of how you might encounter partnerships in your work as a real estate professional:

Mary, Susan and Ann are friends who decided to open their own consulting firm as a general partnership called MarSuAn. When they buy real estate for their business, the grantee on the deed will be MarSuAn, rather than being each individual partner.

Key Terms

Partnership

An arrangement in which two or more individuals share the profits and liabilities of a business venture.

11.5 Corporations

Transcript

Corporations

Incorporating a business is a common way of establishing a new company, or changing the form of ownership from an existing company. Corporations are legal entities, separate and distinct from their owners (also called shareholders.) The shareholders are not liable for the company's debts or obligations, beyond the risk of losing the value of their investment in the business (in other words the share value of the company stock).

Corporations have directors and managers overseeing the business, and the corporation itself can live forever in theory, with different people at the helm over time.

Corporations can own assets, including real estate, in the name of the business. When a corporation owns real estate, its governing documents will identify who is authorized to sign on behalf of the company to effect purchases, sales or other transactions.

Here is an example of how you may encounter corporations in your work as a real estate professional:

Dorothy, Henry and Emily own a grocery store together. On the advice of their accountant, they incorporated the business with their state, and named themselves as the initial board of directors for their store, which they called “Over the Rainbow Foods, Inc.” The corporate charter specifies that Emily is the company's treasurer, and she is the authorized signer for financial transactions, including real estate matters.

Because business is booming, the three shareholders have decided to look for larger retail space to move their store to. When they find the perfect location, Emily will sign the purchase agreement on behalf of Over the Rainbow Foods, Inc. When they take title to the property, at closing, Emily will be the authorized signer again, and the deed and title will reflect that the owner is "Over the Rainbow Foods, Inc.", not Dorothy, Henry or Emily individually.

When Emily decides to retire, the other directors will simply appoint a new authorized signer who can transact business for the corporation.

Key Terms

Corporation

An entity established and treated by law as an individual or unit with rights and liabilities, or both, distinct and apart from those of the persons composing it. A corporation is a creature of having certain powers and duties of a natural person. Being created by law, it may continue for any length of time the law prescribes.

11.6 Limited Liability Company

Transcript

"LLC" stands for "Limited Liability Company." An LLC is a common form of business ownership, and serves to limit the owners' liability in the company to the extent of their investment in it.

An LLC can have one or more owners, who are also called "members", and is formed when the owners file articles of organization, or similar documents, with the state where they plan to organize to do business. An LLC with more than one member should also have a board of governors, which is similar to a board of directors for a corporation.

LLCs are separate legal entities with their own tax ID numbers, so when the owners of the LLC decide to open a bank account, invest assets in securities, or purchase real estate for the business, it is done under the LLC's name, not under the owners' names individually. This provides some privacy protection for the owners.

There are many reasons a business owner might consider establishing an LLC. They are generally easy and inexpensive to set up, require minimal ongoing legal maintenance, provide pass-through taxation to the owners, and protect the owners' investments in the business to the extent of their investments in it.

Here is an example that illustrates one of the ways you might encounter LLCs when you are working in the real estate field:

John and Jane Sample are real estate investors who buy, renovate and re-sell properties. Because they want to limit their liability during the time they own a property, they set up an LLC to be the owner, calling it Sample Holdings, LLC.

When they buy or sell a home, the name on the purchase agreement and deed will be "Sample Holdings, LLC", rather than their names as individuals.

You will encounter the LLC form used quite a lot in real estate, especially when it comes to larger projects, or when investors are putting together a syndication to purchase multi-family properties and commercial properties. Investors love LLCs as they provide them with the ease of purchasing a property, similar to Partnerships, and what is more important is that they offer protection against liabilities in case problems occur.

It is important that you get familiar with the Limited Liability Company as an entity type given it is the most popular form of owning real estate in the recent years.

Key Terms

Limited Liability Company (LLC)

A business structure that combines the pass-through taxation of a partnership or sole proprietorship with the limited liability of a corporation.

11.7 Syndicates

Transcript

A real estate syndicate (also called real estate syndication) refers to a legal entity (typically an LLC or an LLP) that is formed when numerous investors pool their money together for the purpose of buying real estate. Typically, syndicates are used for commercial, income-producing real estate rather than residential real estate. Think of real estate syndicates as being similar to "crowd funding" the purchase of real property.

The sponsor of the syndicate serves as the General Partner. He or she typically puts up between 5 percent and 20 percent of the equity. The sponsor is responsible for bringing the members together and managing the property on a day-to-day basis.

The other syndicate's investors, who provide the remainder of the capital needed to buy the property, typically serve as limited partners, and are not directly responsible for day-to-day management or operations.

Syndicate investors must meet the Securities and Exchange Commission's definition of "Accredited Investors", meaning each investor must have made at least $200,000/year (or $300,000 jointly) for the previous two years, or they must have a net worth of at least $1 million.

When you are acting as a real estate professional, you may encounter syndicates purchasing or selling commercial property. Because real estate syndicates are established as LLCs or LLPs, the underlying organizational documents will give the sponsor the legal authority to act on behalf of the syndicate.

Let's look at an example:

John wants to invest in real estate and is seeking to purchase a large commercial building. Since he doesn’t have enough cash and credit to purchase the building on his own, he decides to form a real estate syndication. He puts up 10% of the equity needed to purchase the property and finds a group of investors to contribute the remaining 90%. The syndicate is established as an LLP, with John as the general partner and the other investors as limited partners. Once they purchase the property, John will earn a management fee, while the limited partners will earn a quarterly return on their investment, based on the net income collected from the property. When the property is eventually sold, both John and the limited partners will share in the profits from the sale.

Key Terms

Real Estate Syndicate

An organization of investors usually in the form of a limited partnership who have joined together for the purpose of pooling capital for the acquisition of real property interests.

11.8 Condominium and Cooperative Ownership

Transcript

Condominiums / Cooperatives

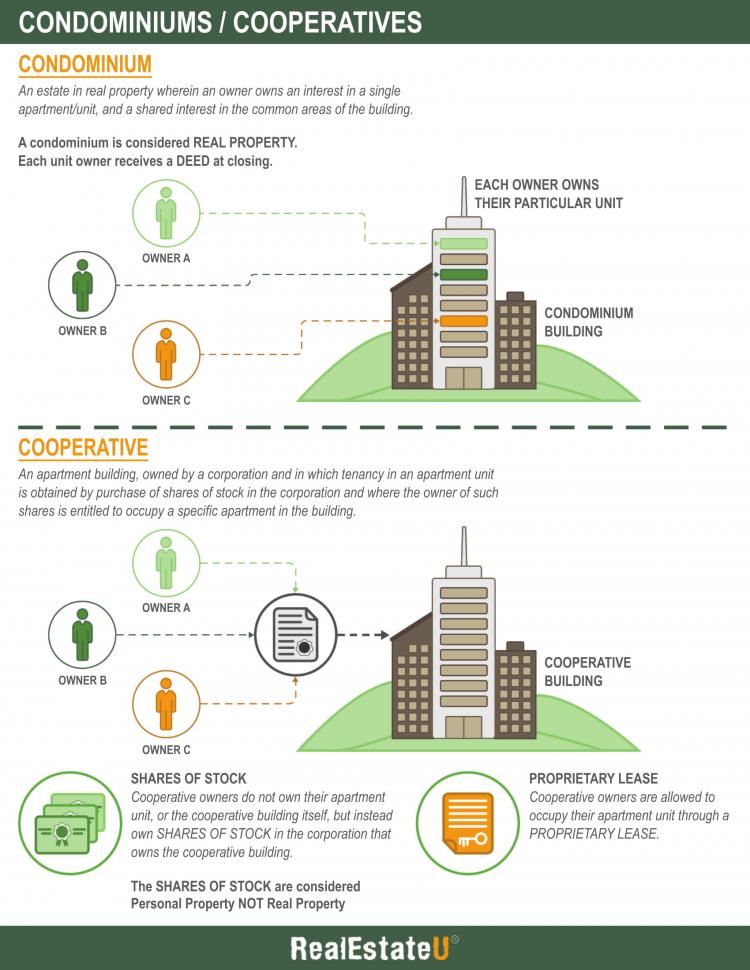

As a real estate professional, you will encounter various types of real property other than one-owner single-family homes or commercial buildings. Two common types of real estate you will likely see on a fairly regular basis are condominiums and cooperatives.

Condominiums

Let's explore condominiums, more commonly known as "condos", first. Odds are good that you already know someone who lives in a condominium - maybe you even live in a condo yourself.

Condominiums are a very common form of residential real property. Condominiums are created when a real estate developer or owner executes a legal document called a "declaration of condominium" (and sometimes also called the "master deed") with the county where the real property is located. This document officially divides the property into separate parcels (units). Traditionally, condominiums were apartment-style homes, however more and more condos are townhouse or duplex-style buildings, or even free-standing single-family homes.

Each unit in the condominium is considered a separate parcel of real estate, and each owner holds a fee simple title to his or her unit. The owner of a condo unit has a deed for their property just like the owner of a single family home or any other type of real estate.

In addition to owning a separate interest in their individual condo unit, owners also own an undivided interest in the condominium's common areas. In an apartment-style condo building, the common areas include things like lobbies, stairs and elevators. In town-house or duplex-style living, common areas include driveways, private roads, lawns and landscaping.

In addition to making any mortgage payments and property tax payments for their condo unit, owners of condominiums must also pay their share of dues each month, which pays for the maintenance and upkeep of their share of the common elements of the building that they own as tenants in common with the other residents of the condominium.

Condominiums are managed by a group of condo owners called the homeowners' association (H.O.A.). The HOA is the group that makes decisions about making changes, improvements or repairs to the condominium's common areas.

Here's an example of condo ownership in practice:

Bob is a young, single professional who wants to buy his first home, but doesn't have a lot of free time and doesn't want to bother with things like yard work or snow removal. However, he wants to take advantage of all of the benefits of being a homeowner and he is wondering what his options are. Bob is willing to pay a little bit extra to have someone else take care of those maintenance tasks for him.

It sounds like condo ownership might be perfect for Bob. He would still own his own home, but wouldn't have to worry about the upkeep of the common areas or outside of the unit. You could help Bob explore various types of condo units that are up for sale, including apartment-style, duplex-style and townhome-style condo units, to find something in his price range, style and location.

When Bob finds a unit he wants and closes on the sale, he will have a title showing he owns his individual condo unit as well as an undivided interest in the common areas for the condo community.

Cooperatives

Now, let's look at cooperatives, which are similar in some respects to condominiums, however different in several other important ways.

A cooperative, also called a co-op, is an apartment building that is owned by a corporation. Instead of leasing/renting an individual apartment unit from the company, people who want to live in a co-op buy shares of stock of the corporation which entitle them to occupy a specific apartment unit in the building.

Where condominiums are considered real property, a cooperative unit is not real property. Instead, it is considered personal property. The holder owns shares of stock; however their ownership is structured as a proprietary lease. So, the individual residents do not own the cooperative the way individual residents of a condominium own the condo.

Cooperatives are created when a real estate developer files an offering plan and issues shares of stock (the proprietary leases). People who want to live in a cooperative either buy their shares outright, or take out a "share loan", which is similar to a mortgage.

Similar to condominiums, which are managed by homeowners' associations, cooperatives are managed by a board of directors which makes decisions about improvements or repairs. Each resident of a cooperative apartment unit pays a monthly maintenance fee, similar to the condo association fees paid by condominium owners.

Cooperatives can be more attractive than renting an apartment unit for some people, particularly in metropolitan areas where the cost of living is higher.

Some cooperatives cater specifically to certain types of residents, like senior citizens.

Both condo owners and cooperative residents are generally responsible for maintaining the interior of their individual units, and are responsible for paying their own utility costs.

Here is an example of how you might encounter cooperatives when you're working as a real estate professional:

Pat is a real estate developer who decided to build a 50-unit cooperative building for senior citizens. Pat formed a corporation and filed an offering plan with the county. The corporation is the owner of the property deed. The corporation issued 50 shares of stock, one share for each unit, and has offered them to sale to potential residents at $200,000/share.

Amy is an active senior citizen looking to downsize her home and thinks the new senior living co-op Pat built will meet her needs well. She bought one share of stock in the corporation. In exchange, she has an exclusive lease to live in unit #102. If she later decides to move somewhere else, she can re-sell her shares back to the corporation, which effectively terminates her lease. Amy's name never appears on the property deed or title with the county; the corporation that owns the building will continue to be the owner of the entire building, including all units and all common areas.

Key Terms

Common Elements

Refers to the spaces in a building shared by residents of the building. These include lobbies, corridors, stairs, elevators, etc.

Condominium

An estate in real property wherein there is an undivided interest in common in a portion of real property coupled with a separate interest in space called a unit, the boundaries of which are described on a recorded final map, parcel map or condominium plan.

Cooperative

An apartment building, owned by a corporation and in which tenancy in an apartment unit is obtained by purchase of shares of stock of the corporation and where the owner of such shares is entitled to occupy a specific apartment in the building.

11.8a Condominium and Cooperative Ownership Infographic

Please spend a few minutes reviewing the Infographic below.

11.9 Creation of Community Associations in Georgia

Transcript

What comes to mind when you hear the word condominium? Is it a small single-family home? A privately-owned apartment in a luxury high-rise? Maybe it is a vacation rental in the mountains with ski-in/ski-out access to the slopes.

In Georgia, the term condominium arrangement does not refer to a particular architectural style or location. A condominium project doesn't even have to include residential units. As long as there are clearly defined privately-owned spaces, and co-owned common areas, such as sidewalks, parks, green spaces, and community centers, any property type can be converted to a condominium regime.

Examples of non-residential condos include:

- A single slip in a marina

- An individually-owned parking space in a parking garage

- A business located in a strip mall or office park unit owned rather than leased

- A separate unit in a storage facility

- A hotel room

- An airport concourse

Any space that can be clearly defined with words and visual floor map or plat can be part of a condominium arrangement, including single-story homes, apartments, town homes and residential units in a high-rise building.

How Does Condominium Ownership Work?

An owner in a condominium arrangement owns his or her unit separately from other properties. Generally speaking, owners have total control and financial responsibility over the interior spaces of a home or commercial property unit, while all co-owned spaces within the condominium are managed by an association board, even though ownership is shared with other community property owners. HOA membership is usually voluntary; however community residents/owners must always abide by covenants and by-laws even when they decide not to join the association.

Property owners may choose paint colors and textures for the kitchen and bath in their 2-story home, while the association by-laws govern the color and finishes for exterior siding, window trim and sidewalks. Property homeowners are also responsible for repair inside the unit, while the association assumes responsibility for maintenance and repair of the common elements.

So, homeowners would hire a plumber to clear a clogged drain, while the association would be responsible for replacing damaged sprinkler system parts in the neighborhood park or playground.

It is important to note that a condominium association is typically a non-profit corporation established to manage common elements of a condominium project, the association rarely owns any property.

Each owner also owns a percentage of the common elements. Calculating percentage of ownership may involve assigning each unit owner the same percentage. In a community with 36 private owners, each owner would have a common area interest of 1/36th. Sometimes, the common area ownership is unequally divided, based on square footage, property type or another formula approved by the association board or community developers.

There are two types of co-owned condominium common areas:

- Limited common elements: Everything outside privately-owned units not available to everyone owner. For example, covered parking available only to some property owners, outside storage units available to those who live on a certain street with a community or people with shared balconies or terraces.

- Common elements: Everything outside the privately-owned unit, including roadways, elevator shafts, roof systems, clubhouses and open parking.

Establishing the Condominium Unit

Legal documents identify specific unit boundaries. Typically, a single-story unit includes the flooring material and everything above it, up through and including the lower surface of the roof. Multi-story condominium regimes may identify unit boundaries as including the floor material and all air space up to and including the uppermost part of the ceiling.

State statute and covenants established by the association may vary in wording, but generally describe the unit boundaries clearly, so that all common areas and privately-owned spaces are easily identified. Simply put, common elements are all those spaces that are not part of the unit, and the unit is the space clearly defined in legal documentation.

Condominium communities created before 1975 are governed by the Georgia Apartment Ownership Act (AOA). All condominium communities created after July 1, 1975, and those that voluntarily submitted to the GCA, are governed under the Georgia Condominium Act. Both groups are also subject to all general statutes and common laws in Georgia.

Three Documents Necessary to Create an Approved, Compliant GCA condominium

Each of the following legal documents must be recorded in the Land Records office to officially create a GCA Condominium.

1) Declarative Statement

The Declaration of Condominium must include:

- A written description of legal boundaries for each unit and for common areas.

- A complete list of private encumbrances, liens, rights, use and management covenants, and easements (such as utility right-of-way, alley access, and common area traffic paths).

- Percentage of common area ownership for each unit.

- Limited common elements; unit assignment per element.

2) Floor Plans

An accurate, visual representation of the written description of interior legal boundaries.

3) Plats

Plats are a visual representation of the condominium project exterior.

What Else Must be Done to Create a Condominium Community?

Recording GCA documentation is only the first part of creating a condominium community. Since virtually all community associations — homeowner associations (HOAs), property owners associations (POAs) and Condominium Owner Associations (COAs) — is a Georgia non-profit organization, almost every Georgia community association will create a corporation to manage the common areas.

The first step is developing articles of incorporation. These straight-forward documents list:

- Initial directors

- An organization's physical and mailing address

- Registered agents

- Person(s) initiating the incorporation process.

Once the initial paperwork is filed, many organizations never review their Articles of Incorporation again, unless the organization is sold, files for bankruptcy or faces legal challenges.

Unlike the Articles of Incorporation, community by-laws are often referred to at least several times every year. They contain specific information about how the organization will operate and detail rules governing:

- Special called meetings

- Regularly scheduled monthly, quarterly, or annual board meetings

- Proxy, notice, quorum and voting requirements

- Board member and officer service guidelines (including how, when and where office election is held, term limits, reasons for early discharge/termination, and more)

Association by-laws are subject to change based on membership and/or board approval and do not need to be recorded. Articles of Incorporation must be recorded with the Georgia Secretary of State.

The declarant of a condominium project must make two disclosures to first time buyers.

#1 states, “Oral representations cannot be relied upon as correctly stating the representations of the seller. For correct representations, reference should be made to this contract and the documents required by code section 44 3 111 of the “Georgia Condominium Act” to be furnished by a seller to a buyer.”

#2 states, “This contract is voidable by [the]buyer until at least seven days after all of the items required under code section 44 3 111 of the Georgia Condominium Act” to be delivered to buyer have been received by buyer.”

The items covered under disclosure #2 are:

- 1. A floor plan of the unit(s) being sold/purchased;

- 2. Declaration and Amendments thereto;

- 3. The Association’s Articles of Incorporation, covenants or bylaws, and Amendments thereto;

- 4. Any ground lease;

- 5. Any management contract having a term in excess of one year;

- 6. The estimated or actual budget for the condominium;

- 7. Any lease of recreational or other facilities that will be used solely by unit owners;

- 8. Any lease of recreational or other facilities that will or may be used by the unit owners with others;

- 9. A statement describing the seller’s commitments to build or submit additional units, additional recreational or other facilities, or additional property;

- 10. If this contract applies to a condominium unit which is part of a conversion condominium, a statement describing the condition of certain components and systems, a statement regarding the expected useful life of certain components and systems, and certain information regarding any notices of violations of county or municipal regulations. A dated, written acknowledgment of receipt of all said items signed by the buyer shall be prima facie evidence of the date of delivery of said item.

The Disclosure Package provides important information for the buyers. And, if anything is omitted or changed that materially affects the buyer's rights or property value, the buyer has an additional seven days to void a contract from the original date of signing.

Any other required disclaimers must be printed in a font not smaller than the largest font in the disclosure package, and be bold or CAPITAL LETTERS to draw attention to the notice.

In summary:

- Any type of property – residential or commercial – can become a unit in a homeowner association as long as the owner has title or deed of trust to the land under any improvements and the “airspace” above them. In other words, properties cannot be stacked vertically.

- It is important to store original by-law and Articles of Incorporation documents in a safe, accessible place even though they aren't reviewed frequently.

- Full disclosure is required by law when selling condominium properties.

- Association membership is optional, but beneficial for property owners.

- Most community associations are non-profit corporations.

Key Terms

11.10 Administration of Community Associations in Georgia

Transcript

The first community association board is formed sometime before the first lot is sold in a new community. Typically, the developer, or a project investor/owner, files articles of incorporation with the Georgia Secretary of State to create a governing body that manages the community neighborhood.

The person completing the initial corporation paperwork, will normally appoint original board members, and record the covenant documents in the county land records office. The first community association board is often a small group of people, perhaps 3-5 people from the declarant's family or employees.

In Georgia, specific state laws govern when a developer-appointed board must turnover the reins to a condominium community elected board.

The original board will manage the association until the earliest of:

- A voluntary surrender of management privileges by declarant, or

- Three years after recording the declaration for a typical condominium corporation or seven years for an expandable corporation where new property may be added, or

- 80 percent of the undivided interest in common area property/elements have been sold.

While the turnover transition process can be quite complicated, the turnover is really simple:

Schedule a meeting, hold an election, done.

The community corporation sends notice to property owners that a turnover meeting is scheduled after the board:

- Chooses a date, time, and place of meeting

- Decides whether they plan to call a special or annual meeting

- Solicits nomination (if bylaws mandate nomination prior to meeting)

- Establish terms of office for newly elected board members/directors

- Determines the number of officers to be elected at the owners' meeting

Some declarants prefer a special meeting because they can limit the meeting discussion to creating a new board through the election process, eliminating any negative comments about current management or problems within the community at large.

Before we talk about the transition challenges, let's back up a minute and talk about terms of office for directors.

Whether an association has 3 officers, 5 or 15, it is preferable to establish staggered term lengths. This strategy usually ensures both continuity and a regular infusion of fresh ideas and diverse thought. If some board members are elected in even-numbered years after the turnover transitions and others are elected in odd-numbered years, there will always be some officers with at least one year's experience serving on the community board.

But, let's say the board has 7 officers, and 3 positions are subject to election every two years, while the other 4 positions are elected every four years. This scenario would mean that all positions come up for re-election every four years. It is possible, although not likely, for all officers to be newly-elected every four years.

Georgia's law does not dictate for officers to come from the board member pool. Also directors may all be “outsiders,” so to speak, unless bylaws specifically prevent non-board members from being officers. The typical association officer term in George is one year.

Since many elected board members are non-paid volunteers, and may or may not have related business experience, this continuous turnover could lead to inefficiencies as new board members learn the rules, regulations and nuances of running a non-profit corporation.

The typical board may have:

- A president who presides over all association meetings, sets the meeting agendas, appoints special committees and signs most legal documents.

- A vice president who assumes presidential duties when a president resigns, is recalled, or cannot perform for any other reason.

- A secretary (and, assistants as needed) who maintains all books and records for the community, although state statutes don't define “books” or “records,” so these files may or may not include organizational records as well as financial transaction documents. The secretary is usually responsible for internal and external communication — such as sending written notice of upcoming meetings, community events and assessments.

- A treasurer (and, assistants as needed) who maintains budgets, files annual tax returns, confirms or makes payments for utility bills, federal, state and local taxes, insurance and other operating expenses. The treasurer may provide financial statements to owners quarterly or annually.

- Other positions described in community bylaws, or created by the board. For example, some association boards have a human resource officer or security director on the board.

Boards and brokers may also delegate duties to a community association manager (CAM). Some common administrative tasks that CAMs assume include:

- Paying association bills

- Sending meeting notices via email, paper-mail, text, telephone call or other communication channel.

- Taking meeting notes

- Maintaining common area elements and property

- Managing social media and website platforms

- Depositing payments received

- Collecting assessments in person, online or through physical “drop boxes”

Paying Board Members For Services

Compensation is optional for non-profit corporation board members. The Non-Profit Corp Codes state that waiving payment for services does not allow a director to waive responsibility or liability. Covenants typically cover who shall and shall not receive compensation for services; and bylaws can be changed with an association membership vote of approval.

However, these general guidelines are commonly applied in Georgia:

Federal tax law requires associations issue a 1099 to all board members with a taxable benefit of $600 or more, the same way that a for-profit corporation would handle outside vendor and independent contractor payments.

- Community associations rarely, if ever, waive association dues or assessments for board members.

- Paid board members should never be paid in cash or in-kind, only via association check. For example, it would not be proper to waive monthly HOA dues in exchange for serving on a committee. If an association desires to pay board members, and the bylaws prevent this action, bring the matter up before the membership in a special assigned meeting or annual meeting. Covenants and bylaws can be usually changed with a majority member vote.

Removing and/or Replacing Board Members

Standard non-profit corporate code allows directors singularly or collectively, be removed with or without cause by a simple majority vote of membership during a meeting called specifically for removal. Formal notice must state the sole purpose of the meeting, and whether the vote is for a particular director, or the entire board.

Unless otherwise stated in current bylaws:

- A board-elected director to fill a vacancy can be removed for cause by the board.

- Members can vote to remove a replacement director with or without cause.

- A positive member vote of corporation membership can fill a vacancy on the board.

- A new director may be approved by a majority of the board of directors to fill a vacancy.

As an example, the bylaws state any director may be removed from the board for missing three consecutive meetings. The other directors could vote to remove that director for cause immediately after the third meeting was missed, and vote on a replacement, even if there was not a quorum.

Members, on the other hand, could vote to remove the director after the second meeting missed, because the membership is allowed to remove directors with or without cause. The members could then vote to fill the board vacancy, if they had an appropriate nomination.

As we wrap up, let's talk about a unique challenge for associations. The issue of majority rules.

Achieving a quorum is often difficult. While the GCA and POA rules are silent on board voting and quorum standards, the Corporate Code for condominium, property owner association and HOA organizations is taken from section 14-3-824 of the Georgia Code

14-3-824 states [quote] “No action permitted unless quorum is present at time of vote. Unless the legal documents specify otherwise, the affirmative vote of a majority of the directors present when a vote is taken is the act of the board of directors as long as a quorum is present”

Association bylaws may state a particular number of board members and/or homeowners must be present to hold certain votes, or the covenant documents may be silent.

A majority is based on the votes cast, not the body. For example, if there are 13 directors, and 9 are present, there is probably a quorum, since 7 would be enough to satisfy the “simple majority rule.” However, only 5 votes would be needed to take action, since 5 is the lowest vote count necessary to demonstrate a majority opinion when 9 people are present.

Key Terms

11.11 Managing Community Associations in Georgia

Transcript

This lesson builds on previous community association lessons about starting and running a community association. We will continue using acronyms and terms introduced in previous lessons.

For example, “GCA” means the Georgia Condominium Act and “POAA” refers to the Property Owner Association Act.

If necessary, please refer to previous lesson notes for clarification.

Let's start by talking about the financial side of running an HOA or POA organization. Properly handling money is an essential part of good governance.

Boards manage association financial matters like any other business, tracking income receipts (revenue) and outgoing expenditures (expenses). The corporation must file federal, state and local tax returns, and issue 1099s and owner statements to people who will use those documents to file their own tax returns and claim refunds or make their liability.

Even when an organization hires an outside accountant to prepare tax forms, the board — or an appointed office — assumes responsibility for ongoing record keeping and cash management.

Organizations typically use one of the following accounting methods.

The cash accounting method, which records expenses and revenue on the date of occurrence. For example, if the board ordered new landscaping equipment, and paid for the machinery on March 12, 2019, the records will reflect an expense entry on March 12, 2019.

The accrual basis accounting method, which records transactions on the scheduled date of payment or income. For example, if an insurance policy payment is due on the 20th of May, but the check is not written until the 20th of June, the expense is still recorded in May as an accounts payable line item.

The last method is the hybrid accounting method, which uses a combination of accrual basis and cash accounting methods. Most organizations use this method, although the IRS does not officially recognize the hybrid as an approved accounting method for tax reporting.

Each community association sets their own financial statement policies. However, every HOA or POA issues periodic financial statements to owners and investors. Lenders — and some potential buyers — may also ask for financial statements prior to establishing credit worthiness.

Examples of financial statements include the annual budget, income statement, profit and loss report and the balance sheet.

Income statements reflect the corporation's profitability for a given period, such as a month, individual quarter, or fiscal operating year.

The balance sheet represents the assets, liabilities, and shareholder equity, at a specific moment in time.

The balance sheet may be generated at any time, as often as necessary, to monitor the current financial health of the organization or show the exact value of all assets wholly owned by the corporation.

Budgeting is a very important job for the Chief Financial Officer and executive board members. A working budget informs spending decisions, and helps the board set reasonable membership fees and one-time assessments for capital improvements or compliance penalties.

Budgeting is the process of calculating expenditures and income for the entire year in advance. Board members review the prior year as a basis. Then, they predict increases in utility expense, decide whether major repairs are needed — such as new fencing, replacing the roof on common area buildings, or repairing sidewalks and parking areas — and try to estimate how many properties will be sold that may impact expenses and income during the twelve-month period.

The budget is a guide, and there are no legal requirements to prepare an annual budget beyond the GCA requirement to provide a budget in the full disclosure package during the first-time sale of each condominium unit.

Many associations review the budget each month, and the board makes recommendations as warranted. Budgets increase and decrease based on reality. So, if a natural disaster destroys or severely damages the community clubhouse, a budget adjustment allows financial leaders to revise the plan to allow new assessments to cover repair or replacement in the amount over any insurance payment received.

There are many ways to structure a budget, including zero-based budgeting and incremental budgeting.

A zero-based budgeting strategy means that no historical data is used as a basis because each line item is thoroughly investigated and established based on projected “necessity.”

An incremental budgeting plan uses historical data as a base, and each line item is increased incrementally.

Budgets include both income and expense line items. Under the assets, you might find listings for general assessments, special assets, and specific fees and assessments representing income. The expense line items would include things like:

- Utility bills

- Property insurance

- Landscaping and pool supplies

- Common area plumbing repairs, paint, tools, office supplies, and other operating expenses

- Capital reserves — deposits into a savings account for future capital improvements

- Capital improvement expenses — adding a gated entrance or pool is an example of capital improvement possibilities.

Before we continue, here is a little more information for the non-accountants among us.

Capital reserves are monies set aside for future improvements, where coming up with the money all at once would be financially challenging. By collecting special assessments for roof replacement based on life expectancy, and depositing that money into a savings account, owners make a series a small payment over several years, and the association is prepared well in advance for large expenditures.

While Georgia statutes do not require reserve funding for HOAs and POAs, FNMA and FHA require “adequate” reserve funds prior to funding condominium loans. Generally accepted accounting principles recommend all businesses regularly fund reserve accounts.

Best practices for establishing reserve funding plans include determining:

- The life-expectancy of each capital asset,

- The cost of replacing each capital asset based on maximum life-expectancy, and

- The total the corporation should set aside each year to satisfy future capital investment needs

Let's assume a new roof was installed over the community meeting center, and an association board is preparing the budget. With an expectancy of 10-years, barring some type of disaster, and a future cost of $20,000, the corporation would need to set aside $2,000 each year to cover a replacement.

Of course, some roofs age prematurely, and replacement costs could unexpectedly rise if there is a wobble in the construction material supply chain, so it is wise to shorten the “savings” period, and slightly increase the minimum reserve to strengthen financial health and preparedness of the organization.

Creating a budget is the board's responsibility. The budget approval process is clearly defined in the association bylaws and covenants, and almost always gives the owners the responsibility to approve or vote down the budget.

Most bylaws require owners to approve a working budget before the board can act on it. However, if homeowners are satisfied with a proposed budget, they may not bother to show up for the special meeting to cast their vote. This could, in effect put the board in a position to either take action on an unapproved budget or forgo certain projects because a new budget was not adopted.

Boards can work with members to change bylaw phrasing to stipulate that proposed budgets are owner-approved unless voted down. This works much better than the previous situation, because we all know that everyone expresses dissatisfaction with an issue quicker than they would an outcome that makes them very unhappy. People show up to vote NO... it is just human nature.

A properly adopted budget reduces legal liability, ensures the board stays motivated to follow best-practices and keeps all stakeholders equally responsible for their shared property.

Like budgets, most “legal” action taken by association boards is guided by specific covenant and bylaw language, even if there isn't a Georgia law or statute that requires or denies certain activities.

For example, condominium owners in Georgia are required to pay assessments. Legal precedents in Georgia lawsuits support an association's right to assess liens and collect past due assessment based on provisions in bylaws and covenants.

It is important to follow best-practices when collecting past due fees and assessments. The acceptable path to winning a legal battle, and ultimately receiving monies owed is:

- File a lien

- Start a lawsuit

- Send a FiFa notice to the default owner

- Initiate Association foreclosure proceedings

- Find owner assets eligible for lien attachment beyond community property. Other assets subject to a lien include real property, vehicles, watercraft, and anything that can be seized and sold to recover debt.

When an association does these five things out of order, or in a manner not consistent with the community association bylaws, owners may counter-sue. Even if the owner loses their cases, it could cost the association thousands of dollars to defend their case in court.

Boards have the responsibility to establish a comprehensive collections policy as quickly as possible after they assume management rights from the developer. The policy should be crafted based on current bylaws and covenants, or documents should be properly amended before the policy takes effect.

This policy should include:

- The date late fee; this could be something like “five days after the assessment due date” or “late fees will apply if not paid by the fifth of the month following the date of mailing the first notice.”

- The amount of the late fee. This could be a fixed amount or a percentage.

- The amount of interest to be changed, if applicable.

- The date interest will be charged, and the way it will be calculated. For example, simple interest, compounded daily or annually, etc.

- Date of acceleration

- Due date of an assessment

- Date notices will be sent to delinquency property owners

- The threshold that will trigger hiring an attorney

- The date attorney's fees will be charged

The GCA and POAA both stipulate that attorney fees are collectible, providing assessments and collection processes follow covenants and bylaws.

Managing a condominium association is a complex process. When boards diligently strive to make sure policies accurately reflect covenants, bylaws and Georgia law, they reduce legal liability and generally have higher owner compliance rates.

Key Terms

11.12 Time-Share Ownership

Transcript

A time share is another form of ownership for real estate that you might encounter when you are working as a real estate professional. Time shares are typically located in areas that are popular with tourists or people on vacation.

When someone owns a time share in the United States, they own the rights to use or occupy a lot, parcel, unit, or segment of real property, and their ownership is evidenced by a deed or title showing they own a fee simple interest.

Time share ownership typically allows the owner to use the property on an annual or other recurring basis for a specific period of time. Most time share interests are sold as one-week interests to use a specific unit, or a specific size or type of unit, such as using a one-bedroom unit for the 14th week of each year. Time shares are often also sold on a "floating" time basis, so the owner can use their week any time of the year, subject to availability at their resort.

Buying a time share interest is significantly cheaper than purchasing a separate vacation property, which is part of what makes them attractive to many purchasers. Owners pay an annual maintenance fee to their resort, but are otherwise not responsible for maintenance or upkeep of the property.

Another attractive feature is the opportunity to trade time share weeks through an exchange system so the owners can vacation in other locations instead of returning to their home resort each year.

Let's look at a short example of time share ownership in practice:

Tom and Diane are married and in their 40s. They want to vacation every year, but don't want to be tied down to a specific piece of real estate or assume another mortgage. Time share ownership would be a way for them to own property they can use every year without the hassles that can come with owning a vacation home.

They own a time share in Florida, and after vacating there several times already, they decided to do an exchange with another time share owner, for a similar property, in Spain. So next year Tom and Dian will enjoy their vacation, for a week, in Spain and the owner of the timer share from Spain will enjoy a vacation in Florida, in Tom and Diane’s property.

Key Terms

Time-Share

A form of subdivision of real property into rights to the recurrent, exclusive use or occupancy of a lot, parcel, unit, or segment of real property, on an annual or some other periodic basis, for a specified period of time.

11.13 Georgia Time-Share Act

Transcript

This lesson will cover the George statutes and regulations governing time-share programs.

A time-share program refers to an agreement for the use, occupancy, or possession of real property where the property is divided into predetermined and recurring time periods.

The buyers may divide the property access on either a fixed or floating schedule, as long as:

- The timing occurs annually, and

- The time period is over one year in duration.

For example, six co-owners of a single condominium unit may share a property based on each owner having access and full use to the property twice each year for a calendar month each stay.

The time-share program can be created as either a fee simple estate or a use arrangement (leasehold). An estate in fee simple is an absolute ownership characteristic where there are no restrictions on use or tenancy, other than those issued by the government. A leasehold arrangement is considered to be an ownership defined in years, such as a 99-year lease that either expired or may revert to prior owners, or be renewed by a new contract.

The Georgia Time-Share Act, adopted in 1983, governs time-share programs in the State of Georgia. The Act was amended in 1995. Provisions of this Act, and any amendments, apply to all time-share programs within Georgia state boundaries, and any out-of-state programs sold within Georgia.

The Act allows timeshare buyers the same privilege afforded to condominium buyers, the right to rescind a contract to purchase within seven days of entering into a contract.

A timeshare program developer creates a timeshare program by filing a set of required documents with the Superior Court of the county (or counties) where the proposed program will be located.

The initial document package must include:

- The county name(s);

- A legal description or other description that completely identifies the property;

- Identification of timeshare estates, and the method for creating future estates, if applicable;

- The method used to calculate common expenses, voting rights assigned to each divided interest, and any units in a development not assigned to the timeshare program;

- Restrictions on use, occupancy, modification, and alienation of timeshare intervals;

- Owner interest, if applicable;

- Personal property contained on the property, and provisions for repair and maintenance; and

- The reasonable arrangement for managing common areas, units and property repair and maintenance, including unit furnishings – this is similar to requirements for condominium projects, in that owners share benefits and responsibility for areas not necessarily contained within an individual dwelling.

Developers have certain responsibilities to prospective buyers. The Georgia Time-Share Act requires developers to provide written documentation that describes the property care and maintenance plan, and they must only use licensed real estate agents to make the program and negotiate contracts.

Developers must also make sure any marketing promotions and/or contests comply with the Fair Business Practices Act as administered by the Office of Consumer Affairs.

The Time-Share Act has other buyer protections, such as a provision that prohibits any person from charging an advance fee when helping an owner resell a timeshare interval. Advertising fees must be paid to a non-affiliated third-party, not the agent brokering the sale.

In other words, a real estate agent could not ask for money upfront to run newspaper ads or create a social media ad, but an owner could run an ad in the local newspaper himself, providing he pays the media company directly.

The Act also stipulates that timeshare documents must create an association of timeshare unit owners to manage and operate the program. The association must create bylaws, arrange for a program manager, establish and collect assessments to cover repair and maintenance, insurance and other shared operating expenses.

Key Terms

COPYRIGHTED CONTENT:

This content is owned by Real Estate U Online LLC. Commercial reproduction, distribution or transmission of any part or parts of this content or any information contained therein by any means whatsoever without the prior written permission of the Real Estate U Online LLC is not permitted.

RealEstateU® is a registered trademark owned exclusively by Real Estate U Online LLC in the United States and other jurisdictions.