Chapter 13 - Title Matters

Learning Objectives

At the completion of this chapter, students will be able to do the following:

1) List at least two types of deeds.

2) Describe at least two elements found in a valid deed.

3) Describe the difference between actual and constructive notice.

13.1 Types of Deeds

Transcript

Let's take a look at deeds, something you encounter every day in the real estate industry.

Before we delve into deeds and what they are, we have to first understand the nature of ownership of real estate. Legal scholars define ownership in real property as a "bundle of rights," like a bundle of sticks. One can do many things with real estate... you can own it outright, you can rent it, sell it, sell part of it, sell rights to the parts underground or on top, sell rights to the fruits that come from the land, lease it, pledge it as collateral for a loan, sell it to someone for the duration of their life, even set conditions for future ownership. With all of these rights to land, it's no wonder that there are a significant number of different deeds that can be involved in a transaction.

The first rule of real estate conveyance (having the rights to real estate change hands) is that you can only convey that which you own. In other words, you can't sell something you don't already own. If a piece of property is pledged as collateral for a loan, then the owner has given up a few sticks in her bundle of rights. The person buying the property takes it subject to the rights of the lender. The new owner only has the sticks the prior owner had leftover. The only way to recover those missing sticks and make a complete bundle is to pay off the lender and have him convey his rights back to the owner. It all sounds very theoretical and esoteric. But these are the transactions we deal with every day in the real estate industry. The type of deed used in a transaction is based on the bundle of rights that the seller has, and what part of the bundler she wishes to sell.

A deed is a document that conveys, or transfers, an interest in real property. As we said before, the interest could be total ownership or a limited form of ownership. The concept of the deed dates back to the Bronze Age, and perhaps earlier. The Jewish Talmud, Tractate Bava Basra, discusses how ownership of land can be shown by a "shtar," a document reflecting a change of ownership from one person to another. For safekeeping, these documents were placed in clay jars and stored underground. The concept carried down to the present day (though today we store deeds in a county record room in books and file cabinets).

From here we see that deeds have two purposes... to transfer ownership of land from one person to another, and to prove ownership of a parcel of real estate.

Usually, there are two parties to a deed, the grantor and grantee. Later we'll talk about judicial deeds where an officer of the court is a third party. The grantor is the person selling the land and the grantee is the person buying the property. So when you're confirming ownership of a property, you would look at the "grantee" of the deed.

It's important to note here that "person" doesn't have to be a human being. A person in the legal sense can be any legal entity like: a corporation, a limited liability company, a trust, or a partnership. All of these entities can own and convey property similar to a human being.

The deed itself contains the names of the grantor and grantee, the date of the transaction, a legal description of the real estate (described by its boundaries relative to other real estate), and the signature of the grantor. The grantor's signature is notarized, meaning an independent person confirmed the identity of the signer to be the owner of the property listed in the deed.

A significant part of the deed is the "warranties." Warranties are promises about the property made by the grantor. Essentially, the grantor is saying, "I own this property, my rights to the property are limited by certain conditions, and I promise you (the grantee) are getting the property as it is described in the deed." The warranties are what distinguishes one deed from another. Here are some of the deeds you will see in your travels in the real estate industry:

A general warranty deed (or warranty deed in some states) is the most common type of deed in real estate transactions. It provides the most protection for the buyer (the grantee). In a general warranty deed, the grantor promises that no one has other claims of ownership of the property, no encumbrances, like mortgages or liens, no boundary disputes, and also promises that, based on the prior owner's period of ownership, these warranties are valid forever. In order to give a warranty deed, all liens have to be paid off at closing, and a title search must be conducted to make sure there are no other outstanding liens or issues.

A special warranty deed has fewer warranties than a general warranty deed. With a special warranty deed, the grantor only covenants that the property is not encumbered by mortgages or other liens, and that the grantor has title to the property. This type of deed is commonly used in commercial real estate transactions where the grantor is a company that wants to limit its liability in the event a problem with the title pops up, years down the road. Also, commercial real estate may be more complex than a simple home lot which has been a home lot for over a century. Commercial real estate can be carved and re-shaped over years of transactions between companies.

A grant deed is similar to the special warranty deed. The grant deed assures the grantee that the property has not been sold to anyone else, therefore the word "grant." Also, warranties are limited to the grantor assuring that he has ownership of the property and that the property has no liens or encumbrances.

A bargain and sale deed is an even more limited list of warranties. Here, the grantor simply warrants that they have done nothing to harm or cloud the title to the property. This vaguely means that there are no liens or encumbrances, but there may be issues from prior owners that were not resolved by the current owner. A bargain and sale deed is commonly used where neither party wants to undergo the expense of a title search, or does not want to take on the expense of clearing up earlier title issues. The hope is that they won't cause the owner problems like losing the property to an unknown lien. The price of the property may be lower if it's conveyed by a bargain and sale deed than by a traditional warranty deed.

A quitclaim deed offers the least protection for buyers. Here, the grantor is conveying whatever interest they have... which could be none! In this case, the buyer is urged to conduct a thorough title search to make sure that they're getting a property free of liens, easements, and encumbrances. If the seller is not willing to warrant any rights of ownership, the buyer should beware. Like the bargain and sale deed, properties conveyed by quitclaim deed may have a lower market price. But the buyer will assume the risk of whatever surprises are found in the title history of the property.

Sometimes property transfers aren't voluntary. Occasionally, courts get involved in real estate disputes. The dispute may involve two owners fighting over a boundary line, or a lender exercising their right to seize property pledged as collateral for a loan. Certain courts have the power to order the seizure, division, or transfer of real estate. This power is called "equity." If the court finds, based on a state law or a contract, that the transfer of property is appropriate, then it will issue one of the following types of deed. The type of court-ordered deed will depend on the nature of the dispute.

The sheriff is usually the primary law enforcement officer of the court. When the court exercises its power to order the seizure or re-sale of real property, the sheriff usually conducts the sale. An example is when the court issues a money judgment against a defendant, but the defendant refuses to pay. If the defendant owns real estate free and clear of other leans, the judge can order a sheriff's sale of the property to satisfy (or pay off) the judgment. The sheriff conducts an auction sale on the courthouse steps and conveys the property to the buyer by sheriff's deed. The warranties of the sheriff's deed are similar to a quitclaim deed.

You'll encounter a tax deed when the owners of real property do not pay their property taxes. State law allows a county official to sell the property to pay off the taxes. This is a type of seizure of property. Buyers have to be careful of a tax deed. A tax lien is a kind of "super-lien" that allows the county government (or whatever division of government is owed taxes) to auction off the property even though it still has other mortgages or liens on the title. The buyer takes the property subject to all existing liens. The buyer may also have to wait a period of time to fully have title. The previous owner may have a right of redemption, which allows the previous owner to pay off the owed back taxes and fees, to recover his property.

A Trustee's Deed is a type of deed used after a foreclosure sale. In states where a mortgage on property is accomplished by the owner giving a Deed of Trust to the lending bank, a foreclosure sale ends with a Deed of Trust going from the bank to the new owner. Like other deeds based on foreclosure, the warranties are limited. All liens subordinate to the mortgage will be wiped out by the mortgage sale, but tax liens, easements, and certain other limitations on title may follow with the property.

Like a Trustee's Deed, a Deed Under Power is a type of foreclosure deed used when a mortgage is conveyed by a security deed. It also contains limited warranties and title may be taken by the grantee subject to easements, tax liens, and other limitations.

The simple and efficient concept of the deed is complex. Understanding their nature and flavors will help you understand the world of real estate in all its variety and possibilities.

Key Terms

Bargain and Sale Deed

Any deed that recites a consideration and purports to convey the real estate; a bargain and sale deed with a covenant against the grantor’s act is one in which the grantor warrants that grantor has done nothing to harm or cloud the title.

Deed

A written instrument which when properly executed and delivered conveys title to real property from one person (grantor) to another (grantee).

Grant Deed

A limited warranty deed using the word “grant” or like words that assures a grantee that the grantor has not already conveyed the land to another and that the estate is free from encumbrances placed by the grantor.

Grantee

A person to whom a grant is made.

Grantor

A person who transfers his or her interest in property to another by grant.

Quitclaim Deed

A deed to relinquish any interest in property which the grantor may have, without any warranty of title or interest.

Sheriff's Deed

A deed given by court order in connection with the sale of a property to satisfy a judgment.

Special Warranty Deed

A deed in which the grantor warrants or guarantees the title only against defects arising during the grantor’s ownership of the property and not against defects existing before the time of the grantor’s ownership.

Voluntary Alienation

Transfer of title to an asset with the consent of the owner.

Warranty Deed

A deed used to convey real property which contains warranties of title and quiet possession, and the grantor thus agrees to defend the premises against the lawful claims of third persons.

13.2 Elements of a Deed

Transcript

A deed is a written document that has two purposes: (1) to transfer ownership of real estate, and (2) when properly recorded, to tell the world who currently owns a parcel of real estate. To understand how a deed works, we have to understand the parts, or elements, of a deed. As a real estate agent, you’ll occasionally have to review deeds as part of your research for clients. To be an effective advocate for your client, you have to know what information is in the deed, what each part means, and how that information is useful for your transaction.

While there are many types of deeds, like warranty deeds and quitclaim deeds, nearly all have the same elements. Certain details vary from state to state, but the elements we’ll talk about today can be found in just about every state. Where there are notable exceptions, we’ll let you know.

Note first the title of the deed. Is it a warranty deed, a quitclaim deed, a life estate?

This will be a flag whether more detailed research, like a title search or survey, is needed before the transaction goes forward. If it’s only a quitclaim deed, the seller (or grantor) did not provide many warranties or protections for the buyer (or grantee). You may want to do a survey or more extensive title and tax search. The title is not necessarily a legally required “element,” but it is important to understand what sort of paper you’re holding.

The first legally required element is that the deed be in writing.

This sounds obvious, but people rely on oral contracts every day. The law in all 50 states, as handed down from our English “legal” ancestors, is that real estate can only be conveyed in writing. This is to protect against fraud and people stealing land. In fact, the ancient law where this rule was created is called the Statute of Fraud. There are rare exceptions, like adverse possession, but even that eventually requires a court order for recognition as a valid transfer. For all practical purposes, a deed must be in writing.

The grantor, the person conveying title to the property, must have legal capacity to be the grantor. This means that they own the interest in the property that they are conveying. If the grantor doesn’t own the interest he’s conveying, then there hasn’t been a transfer of title. The deed is meaningless. It would be as if you wrote a deed to yourself for the Brooklyn Bridge. You don’t own the Brooklyn Bridge, so you can’t give it to anyone.

Capacity also refers to the ability of a person to represent a corporate entity or other non-human grantor. Corporations, partnerships, trusts, and all manner of entities can own real estate. The person signing on behalf of the entity must have the legal capacity, or power, to sign. A trust can be represented by a trustee. A partnership by a designated partner. A corporation by an officer authorized by the Board of Directors or by-laws.

The deed must also be conveyed, meaning handed over to the grantee, the person receiving title to the property. If you write a deed and keep it in your file cabinet, you haven’t transferred title to the property. It has to get into the grantee’s hands. Practically, at most closings, the seller will sign the deed and give it to the closing attorney or title company. Then the attorney will have the deed recorded with the proper government authority. And finally the attorney will send the original, recorded deed to the buyer a few weeks later.

These are the parts of a deed that won’t necessarily appear on the face of the document. So what are we looking at when we see a deed?

First, the deed will have a date. The date tells you when the property was conveyed. This isn’t just a nice frame of reference. It is important for the order of the title history. If deeds are dated out of order, there will be a question about who really owns the property. If Kim sells one of her houses to Khloe, and the deed is dated May 10, 2017, and Khloe sells the same house to Bruce, but the deed is dated May 9, 2017, Bruce does not own the property in the end. Why? Because, on May 9, Khloe didn’t own the house yet! Even if the transactions were done in the correct order in real life, the title owner of the property is still Khloe, and not Bruce because of the dates on the deeds.

Next, the deed lists the parties to the deed, the grantor and grantee. The grantor is the person (or entity) selling or giving the property. This is the prior owner. The grantee is the person or entity buying or taking the property. This is the current owner.

When looking at the grantor and grantee, it is important to note the capacity in which they’re buying or selling. In the case where the grantor is an entity, the signor will have next to their name, something like, “the duly authorized representative of the corporation,” or “in his capacity as president of the corporation.” If the person signing doesn’t have legal capacity, or the grantor does not have the legal capacity to convey the property, then there is a problem with your deed. In that case, consult with an attorney about your options for helping the transaction go forward.

In order for a contract to be valid, there has to be consideration, in other words, the exchange of something of value. For the conveyance of title to property from the grantor to grantee to be complete, the grantee has to give the grantor something of value. The deed must state that something of value was given by the grantee to the grantor in exchange for title to the property.

The consideration clause takes a few different forms depending on your state. In some states, consideration has to be “nominal,” meaning something symbolic. In those states, the deed will state the following words: “in consideration of $10 paid in hand…”

Now, was a piece of real estate sold for $10.00? No, of course not. It’s just a legal convention to make a valid contract and show that the property was given for something of value. The actual sale price of the property will be listed on another form or a tax filing. In other states like Tennessee, the actual sale price has to be included on the deed itself. In transactions between family members where property is given as a gift, some states allow the deed to state something like: “in consideration of a lifetime of love and affection…”

The deed must state that the property is being transferred. This is called the granting clause. It will have wording something like: “the grantor does hereby convey, transfer, sell, alienates… the Subject Property to grantee.” These are the legal words that reflect the grantor conveys his entire interest in the property to the grantee.

The specific interest in the property being conveyed is called the habendum clause. The deed will state the type of interest being conveyed to grantee. Usually, this will state a “fee simple” interest, meaning all possible ownership rights. But there are other types of interest like a leasehold or life estate. Practically, most conveyances fee simple.

What property is being conveyed by the deed? You’ll find this in the legal description. All deeds must contain a description of the property being conveyed. Legal descriptions can be included in the deed itself, or an “Exhibit A” attached to, and recorded with, the deed. The description can be simple, referred to a deed book and page number of a plat, recorded with the county real estate records. Or it can be more complete, listing the metes and bounds of the property. This is a technical description of the borders of the property. The description will begin at a point, usually created by the county, and then extend for a distance and turning at angles to eventually complete a border. Most residential real estate has well-established metes and bounds. Commercial property or raw land may have a more complex description.

The last element of every deed is the notarized signature of the grantor. If the grantor is a corporation or other entity, an authorized representative with authority and capacity will sign, with their authority indicated by their signature. The signature must be witnessed by a notary public, who will sign next to the grantor's signature and affix their seal or stamp. This is to show that a person authorized by the state to administer oaths has verified through identification that the person signing is, in fact, the grantor listed on the deed. Some states require one or two non-notary witnesses to the signature in addition to the notary signature. The notary block on the deed varies by state. Some are quite large, like California. Others are shorter, like Georgia. But they all essentially say the same thing... that “I, the notary, have verified the identification of the person signing and it is the right person.”

Once the deed has been written with all of its elements and signed, it must be given to the grantee. As we discussed earlier, in modern real estate closings, the closing attorney or title agent takes the signed deed and brings (or mails) it to the county real estate clerk for recording. Recording means that the deed is scanned or copied into the official books of the county for everyone to see. A stamp is placed on the deed with the deed book and page number. In earlier times, the county maintained a physical book of copies of deeds. So the deed book is the book number. The page is the page in the book. Older records are still kept in the books, but many counties have switched over to an electronic system that can be searched by computer. The deed book and page is a reference for the deed. It can be referred to in other deeds or legal documents, and will forever be the point of reference for that specific transaction.

Recording the deed is generally considered evidence of delivery by the grantor and acceptance by the grantee. This completes the process of transferring title to the new owner.

Key Terms

Acknowledgement

A formal declaration made before an authorized person, e.g., a notary public, by a person who has executed an instrument stating that the execution was his or her free act.

Consideration

Anything given or promised by a party to induce another to enter into a contract, e.g., money, personal services, or even love and affection.

Grant

A technical legal term in a deed of conveyance bestowing an interest in real property to another. The words “convey” and “transfer” have the same effect.

Grantee

A person who receives title to real property by deed.

Grantor

A person who conveys title to real property by deed.

Habendum Clause

The “to have and to hold” clause which may be found in a deed.

Legal Description

A land description recognized by law; a description by which property can be definitely located by reference to government surveys or approved recorded maps.

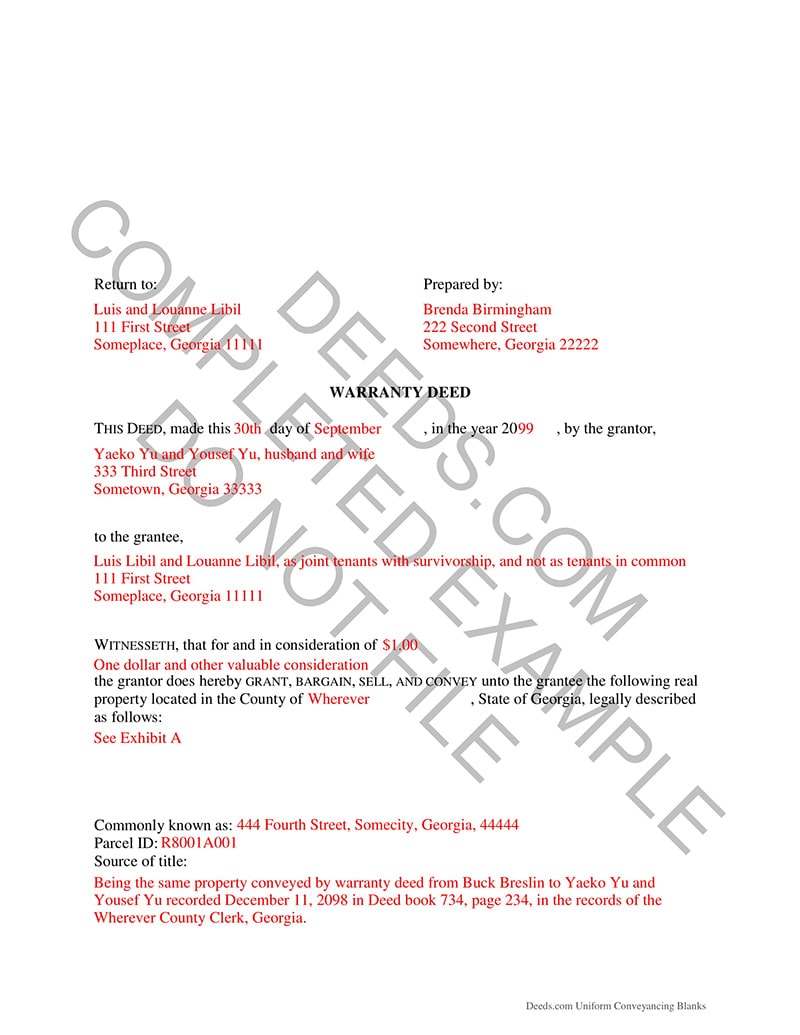

13.2a Example of a Warranty Deed (also known as a General Warranty Deed)

Please spend a few minutes reviewing the document below.

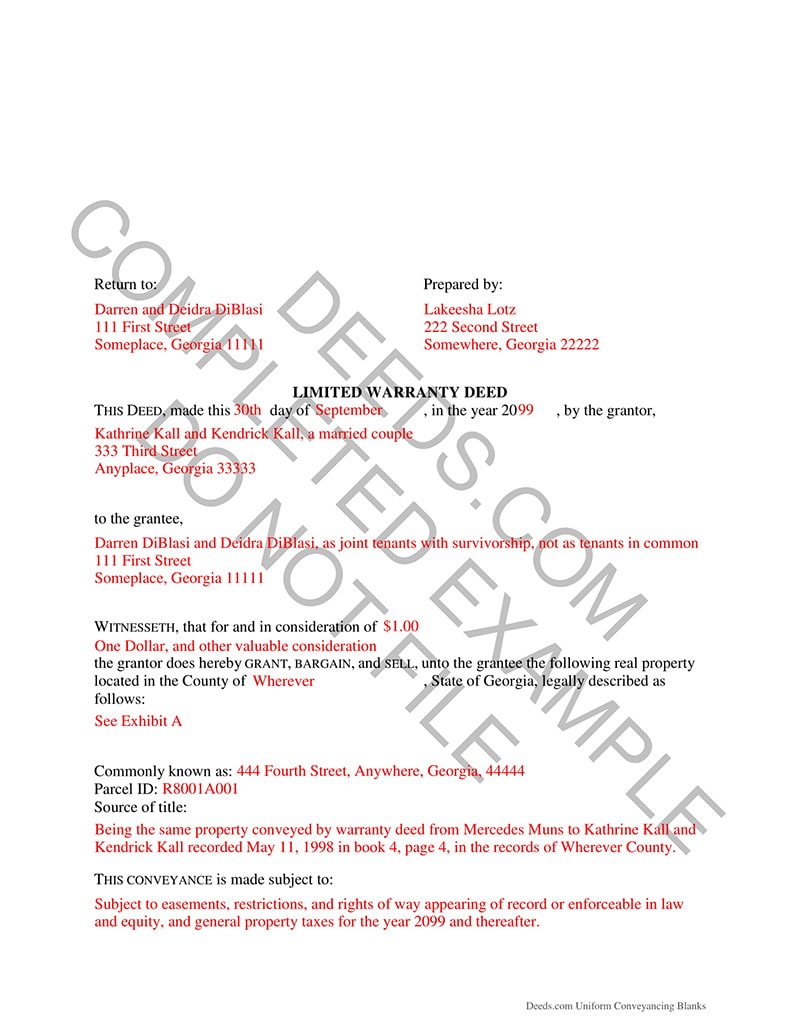

13.2b Example of a Special Warranty Deed

Please spend a few minutes reviewing the document below.

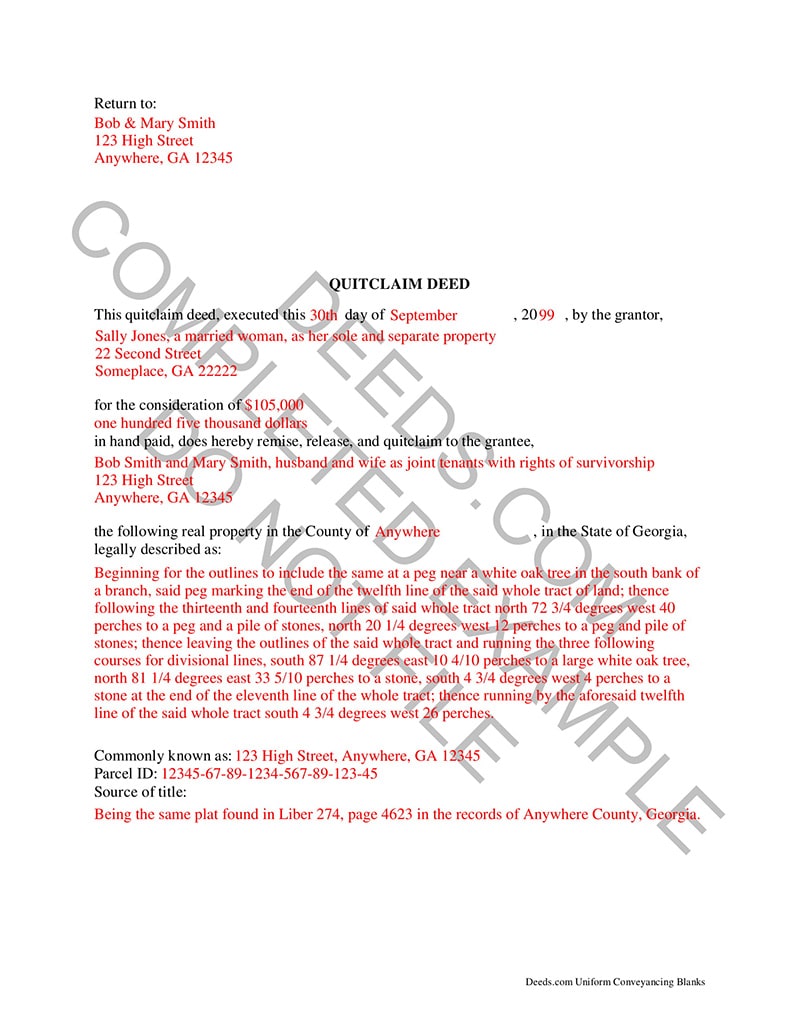

13.2c Example of a Quitclaim Deed

Please spend a few minutes reviewing the document below.

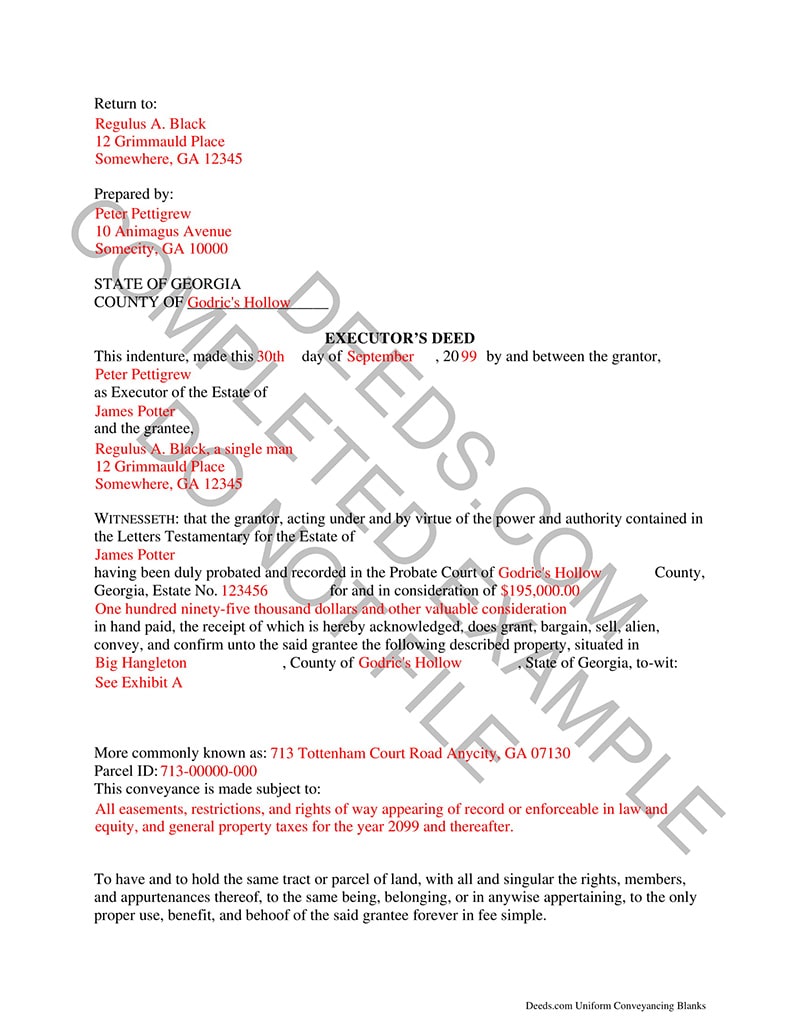

13.2d Example of an Executor's Deed

Please spend a few minutes reviewing the document below.

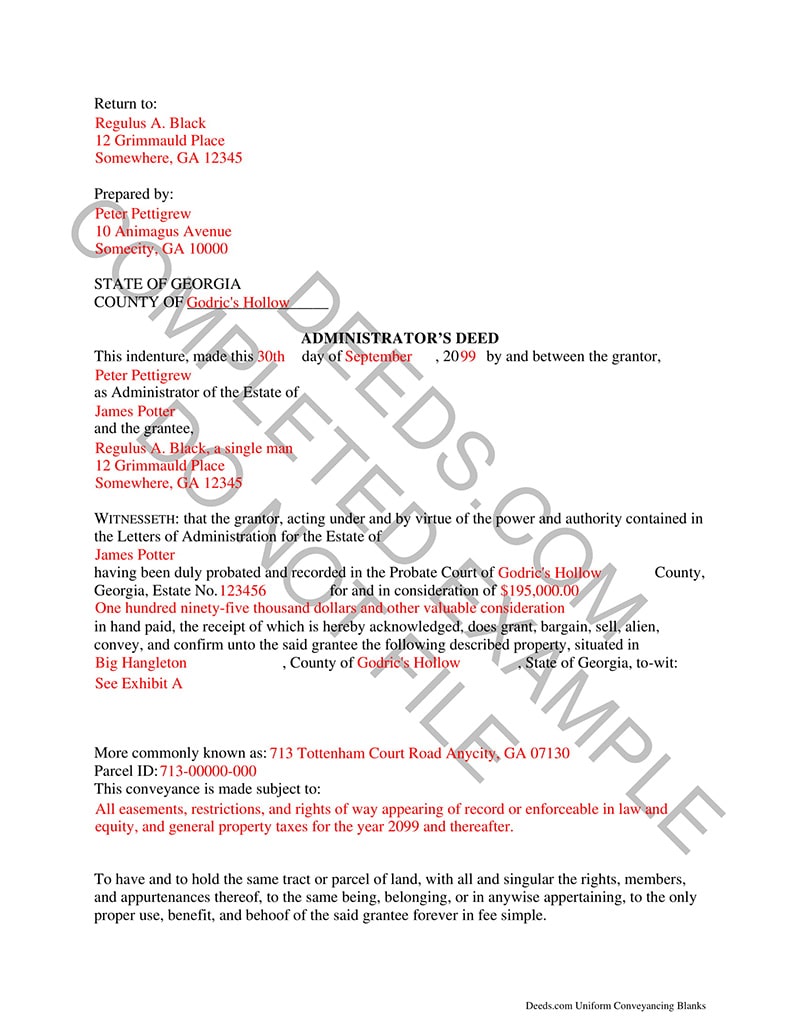

13.2e Example of an Administrator's Deed

Please spend a few minutes reviewing the document below.

13.3 Delivery and Acceptance

Transcript

In order for title ownership of real estate to pass from one person to another, there must be delivery and acceptance of a written deed. The grantor simply writing and signing a deed is not enough. The grantor has to give it to the grantee, and the grantee has to accept the document.

Delivery can be done through any means, as long as the signed original deed gets into the hands of the grantee. It can be mailed, delivered by hand, or delivered through an intermediary. Typically in a real estate closing, the buyer and seller of the property will be present. The seller, or grantor, will sign the deed, but hand it back to the closing attorney. The closing attorney then has the deed recorded in the county real estate records.

After the deed has been stamped and recorded by the county clerk, it's returned to the closing attorney who sends it to the grantee. The grantee can designate an agent to receive the deed on his behalf. This is typically done with corporations and other entities. At that point, the transaction is legally complete and title to the real estate has passed to the grantee.

Acceptance is not merely taking hold of the deed!

There has to be a "meeting of the minds." The grantee has to know what he's accepting, what the deed says, and agree to its terms. This includes an understanding regarding what specific property is being transferred. Also, what warranties and covenants are being made by the grantor, and what rights are being transferred to the grantee. If there is no meeting of the minds, and if the grantee does not accept the terms of the deed delivered, then the transaction may be voided and have no legal significance.

Key Terms

Acceptance

The act of agreeing or consenting to the terms of an offer thereby establishing the “meeting of the minds” that is an essential element of a contract.

13.4 Acknowledgement and Recording

Transcript

A deed to real estate serves two purposes: (1) to convey real property from one person to another, and (2) to let the world know who owns, or owned, a parcel of real estate. Necessary parts of these two functions are acknowledgement and recording of the deed.

Acknowledgement is a statement, written into the deed, that the grantor is signing the deed and conveying the property by his own free will. Acknowledgement is confirmed by a notary public, who signs a declaration that the party signing the deed is, in fact, the grantor (or the grantor's duly authorized agent), and that it is done by free will. The notary will place their official stamp or seal with their signature.

A notary public is a person authorized by the state to administer oaths. The person signing the deed effectively (and actually) swears before the notary that they are the grantor. The notary will also check the signer's identification before affixing their seal. Some states require a lengthy notary declaration. Others allow a short sentence.

All of this is necessary to allow recording!

Recording is when a deed (or other document related to real estate) is copied and entered into the records of the county office of real estate records. This provides notice to the world (or anyone looking) that title to the property is vested in a new person, and the date of the transaction. Once a deed is recorded, it is considered as if everyone is on notice that title to the property transferred, and it is vested in the new owner.

In some states these records are maintained by the superior court clerk. In others, there is an independent clerk. When a document is recorded it is stamped "received" by the clerk's office with a date and time of recording. The deed will also be stamped with a deed book and page. Real estate records were kept in physical books, with each book being numbered sequentially. So the deed was stamped with the book number where it was saved and the page where the deed appears in the book. In modern times, most counties in the United States have moved over to electronic recording. Many maintain the class deed book and page method of cataloging real estate records.

Remember that without acknowledgement, the clerk will not record the deed!

Key Terms

Acknowledgement

A formal declaration made before an authorized person, e.g., a notary public, by a person who has executed an instrument stating that the execution was his or her free act.

Recording

The process of placing a document on file with a designated public official for public notice. This public official is usually a county officer known as the County Recorder who designates the fact that a document has been presented for recording by placing a recording stamp upon it indicating the time of day and the date when it was officially place on file. Documents filed with the Recorder are considered to be placed on open notice to the general public of that county.

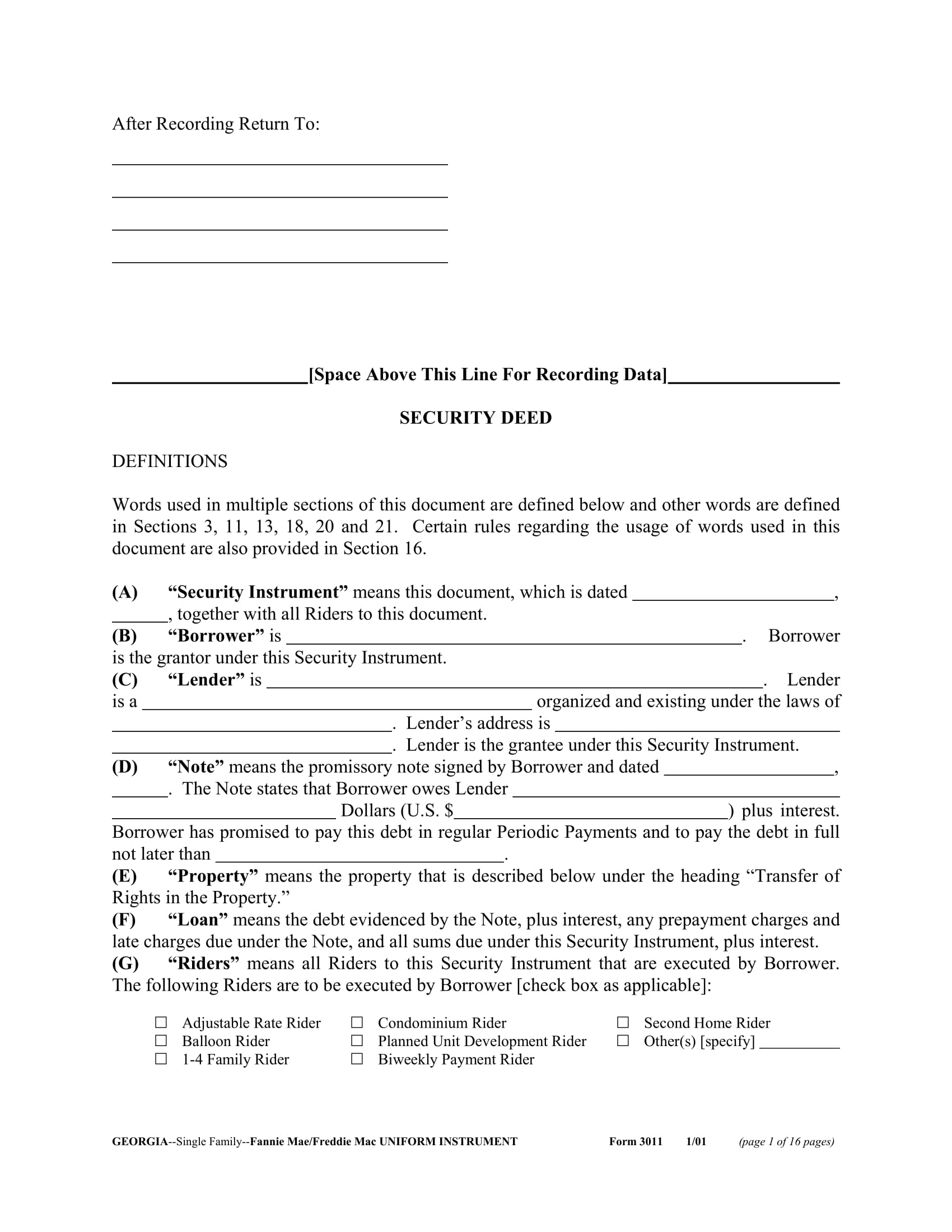

13.5 Security Deed

Transcript

Both a mortgage and a security deed (also referred to as deed to secure debt, loan deed, or warranty deed to secure debt) can be used to secure a financing instrument for real estate loans. Most lenders in Georgia use a security deed because it involves a transfer of title to the property in order to secure the debt whereas a mortgage only creates a lien on the property. A security deed minimizes the risk for lenders in the event of default, allows for non-judicial foreclosure, and speeds up recovery of the real estate collateral for their loans.

Hypothecation and Title to Property

When a security deed is used it gives the lender legal title and it gives the borrower equitable title to the property, with a right of redemption, meaning the borrower can reacquire legal title to the property by paying off the loan. In addition, the borrower retains the right of possession and all rights of ownership except those that interfere with the lender's legal title and any rights given up in the security deed. This concept is called hypothecation: the owner/borrower hypothecates, seeming to “own” the property, but limited by the lender’s rights.

History of the Security Deed

With a mortgage, the property is subject to other liens and/or legal claims. As a way to reduce the risk to lenders, they started requiring a warrant deed from borrowers in the 1800s. In return, they gave borrowers a "bond for title" and agreed to reconvey the property when the loan was paid in full. Eventually, those two instruments combined into a single instrument known as a security deed.

Georgia Code

Georgia Code section 44-14-60 provides that the security deed is an absolute conveyance of title, but that the borrower has the right to have the property reconveyed upon repayment of the debt. The current Act, however, does not require a reconveyance. Instead, upon satisfaction of the debt, the lender simply marks the original security deed as paid and the public records are updated. Only if the original security deed is lost must the lender reconvey the property to the borrower by quitclaim deed.

What Is Included in a Security Deed?

A security deed is an absolute conveyance of title to land from borrower to lender that includes the following provisions:

- A statement that the deed secures an indebtedness;

- A power of attorney from the borrower to the lender authorizing foreclosure upon default;

- A statement that when the debt is paid, the lender will cancel the security deed or otherwise reconvey the property to the borrower; and

- Other provisions defining the rights and obligations of the parties.

Who Are the Parties to a Security Deed?

The two parties to any security deed are:

- Lender/Grantee — has legal title without the right of possession nor obligations of ownership.

- Borrower/Grantor - retains the equitable title to the property and has the right of possession and redemption upon repayment in full. The borrower is liable for property taxes, lawsuits for personal injuries (such as an injury to a third party while that person is on the property), and all the other usual obligations of ownership.

Formal Requirements of a Security Deed

For a security deed to be valid and recordable it must contain the following provisions:

- An identification of the Grantor and the Grantee;

- Sufficient language conveying the property from the Grantor to the Grantee;

- A valid legal description of the property;

- Proper execution (signed by the owner of the property or another person under a valid power of attorney);

- Proper attestation (witnessing by an unofficial and an official witness) which allows the deed to be recorded. Note: Lack of proper attestation will not affect the validity of the deed between the Grantor and Grantee; and

- An effective delivery, meaning the Grantor must put the deed into the possession of the Grantee or the Grantee's agent with the intention that it shall pass title to the Grantee, which usually occurs at closing.

What Are Some Common Clauses in a Security Deed?

While the FHA, VA and FNMA/FHLMC have created their own standardized versions of a security deed, a standardized security deed form for the general public does not exist. In fact, a complex security deed could be 50 pages long while a simple one could be contained on a single page. There are, however, some common clauses in security deeds, including:

- Escrow for Taxes and Insurance — Because property taxes supersede most liens, including a lien created by a security deed, lenders typically require borrowers to maintain escrow accounts to protect the lender from the possibility of a tax lien for unpaid taxes. In addition to the principal and interest payment, the borrower pays one-twelfth of the property taxes every month to the lender and the lender pays the taxes when they are due. A borrower may also be required to pay one-twelfth of the annual hazard insurance premium each month to protect the lender from uninsured losses. Usually, the value of improved property is the building and improvements. If a building is destroyed, and there is no insurance, the lender will be able to foreclose on the land only which will not satisfy the debt on foreclosure. To protect the lender, the lender pays the insurance using the escrow funds and purchases a policy that is payable to the lender in the event of a loss. This requirement is often waived if the borrower has significant equity in the property (typically a 20 percent down payment).

- Due on Sale Clause — This gives the lender the right to call the entire loan balance due upon the sale or ownership transfer of the property. This is a right that the lender may exercise or may choose to waive.

- Waiver of Homestead — The borrower waives the right to claim the benefit of any homestead laws that would affect the rights of the lender to collect the debt.

- Non-Recourse Provision — Not typically included, this is a provision that is sometimes negotiated into a security deed that limits a lender's remedies to foreclosure. In other words, the lender cannot sue for a deficiency judgment after the foreclosure sale if the sale price is less than the balance due to the lender.

- Release Provisions — If the security deed secures unimproved acreage, the borrower and lender may negotiate for the lender to release certain tracts of acreage as the loan is paid down. Most often used when a developer is the borrower who subdivides and develops tracts that are purchased by buyers. The cash from those sales is then used to pay down the loan and release those tracts from the blanket security deed.

- Default — There is no legal definition of default in real estate loan instruments, leaving the borrower and lender free to negotiate what acts will constitute a default. Residential real estate loan instruments for VA, FHA and FNMA/FHLMC loans, however, are standardized, leaving no room for negotiation. Failure to do anything promised in the real estate loan instruments will be a default on the part of the borrower.

The Promissory Note

A security deed requires an underlying debt for the deed to be valid. The evidence of a debt is usually a promissory note, defined as a written instrument in which a borrower promises to pay a lender a sum of money under certain terms and conditions. Both the security deed and the promissory note are forms of contracts.

What Provisions Are Found in a Promissory Note?

A promissory note contains the following provisions:

- Promise to Pay — A promise by the borrower to repay the debt to the lender.

- Amount — The principal amount of the loan stated in US dollars or legal tender.

- Payee — The person or entity who will be receiving the payments. The original designated payee in the note can assign the right to collect the debt to a different party. It is this characteristic that makes the note a negotiable instrument.

- Payor — The person(s) or entity liable for the repayment of the debt.

- Interest and Payments — The annual rate of interest, the date when interest begins to accrue, and the amount and due dates of payments.

- Default, Late Fees, and Acceleration — Default is usually defined as the failure to make the payments when due. Most notes provide that if the payor does not make the payments on time, the lender may charge late fees. Most notes also include an acceleration clause, making the entire amount of the note due upon default.

- Other Agreements — The parties may agree to other provisions, such as attorney's fees if the lender is forced to sue to collect the debt.

- Recourse Provisions — Based upon lenders' rights, there are two kinds of promissory notes: recourse notes and nonrecourse notes. In a recourse note, the lender may look to either the promissory note or the security deed to satisfy the debt. That is, the lender may elect to sue the borrower on the note, which is a personal promise to repay the debt, or the lender may elect to foreclose on the security deed. In a nonrecourse note, the lender's remedy is limited to foreclosing on the property under the security deed. Thus, if the foreclosure sale does not produce the total amount of the debt, the borrower in a nonrecourse loan would not be liable for any deficiency resulting from the foreclosure.

- Prepayment — The borrower does not have a right of prepayment unless the loan documents provide for one; however, most residential loans allow prepayment. Prepayment rights are negotiated in commercial loans with the lender frequently charging a prepayment penalty.

Key Terms

13.6 Example of a Security Deed

Please spend a few minutes reviewing the document below.

13.7 Transfer Taxes

Transcript

Any time real property is transferred from one owner to another a tax is paid to the local government. This is called the real estate transfer tax. The tax is collected when the deed vesting title is recorded in the county real estate records. The body that collects the tax varies from state to state, but the principle is generally the same.

Real estate transfer tax is collected at the closing. Usually it is paid by the buyer or grantee of the deed. While this is the standard practice, it can be negotiable as part of the purchase and sale agreement. The closing attorney or escrow agent will collect the tax at closing and pay the appropriate county agency. This is part of the usual basket of services that the closing attorney, escrow agent, or title agent provides. Often, the vesting deed cannot be recorded unless the real estate transfer tax is paid. In many states, a supplementary form is filed with the deed that shows how transfer tax was calculated and that it was paid.

The amount of the transfer tax varies by state. As an example, the transfer tax may be calculated as $1.00 per $1,000.00 of the sale price. So, if a property is sold for $300,000, then $300 in transfer tax will have to be paid.

In the case of a gift, where there is no purchase price, transfer tax may be avoided. It is best to check with an experienced attorney or tax professional before quoting transfer tax amounts to a client. While transfer tax is a relatively small amount compared to the purchase price of a home, it is very important that the correct amount is collected and paid. Unpaid taxes are a liability for the new owner.

Key Terms

13.8 Involuntary Alienation

Transcript

Most real estate is conveyed through voluntary alienation. In other words, the grantor got rid of the property voluntarily, either through sale or gift. But real property can be conveyed involuntarily as well. These are cases where property is taken from the owner by operation of law.

Under the 5th Amendment to the US Constitution, property cannot be taken without due process of law. The examples of involuntary alienation we’ll discuss here are legal procedures. During economic downturns, there’s an increase in involuntary alienation cases. So today, it is common to see houses for sale that were seized by banks one way or another. These are the most common types of involuntary alienation.

The most common lien is mortgage foreclosure. Even this can be divided into a few sub-types. Bank mortgage foreclosure is the one you’ll see most often. In this situation, the owner of the property did not pay their mortgage. Pursuant to the mortgage documents, the note, deed of trust, mortgage, or security deed, the lender has the right to sell the property to recover its unpaid loan.

Different states have different laws regarding mortgage foreclosure. There are judicial and non-judicial foreclosure states. In states like Florida and New York, which are judicial, the mortgage lender must go to court to get an order allowing the foreclosure sale to go forward. In non-judicial foreclosure states like Georgia and Tennessee, foreclosure can go forward after notice is given to the borrower through mail and advertisement in the local newspaper.

Whichever procedure is required, the involuntary alienation is done by auction on the county courthouse steps. Bidders come for the auction and the highest bidder wins. The property is then conveyed by the bank, on behalf of the old owner, to the new owner, usually in a document called a “Deed under Power”, or “Foreclosure Deed”.

Another type of lien foreclosure is tax sale. In this case, the owner did not pay their property taxes, and the county, city, or state, under statutory law, auctions the property to collect the unpaid taxes. This is not as simple as a foreclosure sale. The new owner takes the property subject to all existing mortgages and other liens. Also, the prior owner usually has a right of redemption, meaning a period of time to pay off the taxes and buy the property back, whether the new owner agrees or not.

A third type of lien foreclosure is levy of a judgment lien. In this type of case, the defendant in a lawsuit did not pay the judgment amount. The sheriff of the county where the defendant lives has the power to take and sell off the defendant's property until the judgment is paid. This can include real estate. Similar to mortgage foreclosure, the defendant is given notice of the sale and it is advertised in the local newspaper. The sheriff holds an auction, and the proceeds from the sale are used to pay off the judgment.

Bankruptcy is another way that an owner can lose their real estate though involuntary alienation. The two main types of consumer bankruptcy case Chapter 7 and Chapter 13. In a Chapter 7 case, the debtor liquidates his property to pay off as many debts as possible. Whatever is not paid off is discharged, meaning it no longer has to be paid. Under the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, the most recent revision of the American Bankruptcy Code, the debtor usually has to surrender his real estate to the mortgage lender to get a discharge of his other debts. If there is no mortgage, the property is sold by the bankruptcy trustee to pay off debts. Chapter 13 bankruptcy involves the debtor reorganizing his debts. Sometimes the debtor has to surrender property for which he cannot afford the mortgage payments.

Another form of involuntary alienation is eminent domain. As we said before, under the 5th Amendment, property cannot be taken without due process. Sometimes the government needs to take private property for the good of the city or state. Eminent domain is when the government exercises its power to confiscate private property for public use. Before land can be taken by eminent domain, the government must pay fair market value for the property. If the owner and government disagree about the value, the case will go to court for a determination of the proper value.

The most common forms of eminent domain are taking a few feet of land along the edge of a road to build a sidewalk. Sometimes the government takes a house or several structures to build a road. Eminent domain has always been controversial. Recently there have been cases where the government used the power of eminent domain to seize land under the guise of "public good" but immediately re-sells the land to private developers. This is an issue being considered by the US Supreme Court.

Lesser known forms of involuntary alienation are adverse possession and escheat. Adverse possession is where real property is taken by the open and notorious use of the land by another person. Title to property passes to a new owner, essentially, by living on someone else's land. The conditions for adverse possession are onerous. Usually, the use of the land has to be for seven years, and some states require 20 years. The use has to be open and notorious; meaning everyone around sees the non-owner on the land, acting as if he's the owner. And the true owner could not have protested during the occupation. Even then, for title to pass in the real estate records, a court has to determine that the land was taken by adverse possession. Usually this applies to property border disputes where a fence is located on another person's land.

Another common example of adverse possession is when there are two adjacent lots and only one of them has access to the main road. The owner of the lot which has no access to the main road must pass through the land of the first owner in order to reach the main road. The second lot needs its driveway to pass through the first lot in order to reach the main road and be able to drive in and out of a garage.

Escheat is a concept in estates of deceased people. If a person dies with property, but there are no living relatives who come forward to claim or distribute the assets of the estate, the property will fall to the state. This happens very often with bank accounts, where the family of a deceased person did not know that the bank accounts existed. But it can happen with real estate as well.

Key Terms

Adverse Possession

A method of acquiring title to real property through possession of the property for a statutory period under certain conditions by a person other than the owner of record.

Eminent Domain

The right of the government to acquire property for necessary public or quasi-public use by condition; the owner must be fairly compensated

Escheat

The reverting of property to the State when heirs capable of inheriting are lacking.

Involuntary Alienation

The transfer of title to real property as a result of a lien foreclosure sale, adverse possession, the filing of a petition in bankruptcy, or condemnation under power of eminent domain or upon the death of the titleholder, to the State when there are no heirs.

13.9 Transfer of a Deceased Person's Property

Transcript

There's a legal maxim that a ghost cannot own property. When a person passes away all of their property (real estate and personal property) automatically passes to their estate. Who administers the state and how the process is carried out depends on whether or not the deceased person had a will.

A will is a document signed by a person giving instructions on how to distribute and dispose of their assets after they die. In most states the will must be written to be valid, and must be signed by multiple witnesses. The person making the will is called the testator. A person who dies with a valid will in force is called testate. In the will, the testator will appoint an executor (or an executrix, if it's a woman) to carry out the instructions in the will. The executor may go to the state's probate court to obtain a document called letters testamentary, which give court-ordered power to the executor to do her job. This is done through a process called probate, where the will is proven to be valid.

However, many people do not have a valid will. When they die, they are intestate. In order for their property to be disposed of, a person, usually a relative, applies to the probate court for a document called “Letters of Administration”. That person will have the power to catalog and distribute the assets of the estate according to state law.

When transfer of property is done by will, it is called a devise. A devise is a gift or distribution of property by a last will and testament. The person making the distribution is the devisor, and the person receiving the property is the devisee. For real estate, the executor will usually use the assets of the estate to make sure all liens on the property are paid off, if that is the instruction in the last will and testament. Then the executor will issue an Executor's Deed or similar deed transferring property from the estate to the devisee. The deed is recorded in the county real estate records, sometimes with a copy of the death certificate, letters testamentary showing the executor's authority, or even a copy of the will itself.

When the deceased is intestate and there is no will, property passes by state law known as descent. Property goes to the deceased's heirs according to their priority in the state statute. Each state is different. Usually, the first to receive property are the deceased's spouse and children. A person cannot take title to property of the deceased simply by being their child. A deed still has to be filed showing the transfer. This is where the letters of administration come in. As we said above, when a person dies intestate, a person, usually a family member, will petition the probate court for authority to dispose of the assets of the estate. The administrator will sign an Administrator's Deed to convey property according to the state laws of descent.

Estates and real property are very complicated areas of the law. When these cases come up, it may be prudent to speak with a competent and experiences estates attorney to make sure that title will pass properly and to avoid any problems during and after closing.

Key Terms

Devise

A gift or disposal of real property by last will and testament.

Devisee

One who receives a gift of real property by will.

Devisor

One who disposes of real property by will.

Intestate

A person who dies having made no will, or one which is defective in form, is said to have died intestate, in which case the estate descends to the heirs at law or next of kin.

Probate

The official proving of a will. The legal process wherein the estate of a decedent is administered.

Testate

Having made a valid will before one dies.

Testator

One who makes a will.

13.10 Public Records and Recording

Transcript

In order for the transfer of property by deed to be valid, the deed has to be given by the grantor to the grantee. But that only serves one purpose of having deeds, and that is conveyance. The other purpose is to let the world know who owns a parcel of real estate, and what liens are already on that property.

To accomplish this, every state has a system of recording deeds. When we talk about recording deeds, we mean all documents that have a relationship to real estate, and the right, title or interest in land. So this includes mortgage liens, easements, tax liens, judgment liens, materialman's liens, notice of lawsuit pending, right-of-way, and any other document that could relate to, or affect the rights of real estate. Without an organized system of recording, no one would know who the true owner of real estate is, whether there were existing liens on the property, or who else has some right to use the property. Mortgage lenders would never lend money. No one would want to buy real estate because they can't trust that the alleged owner is the actual owner.

Each state has its own system of recording deeds. Also, each state has their own standard of what needs to be in a deed for it to be recordable. Though certain similarities exist across most jurisdictions. In order for a deed of any type to be recorded, it must be signed by the grantor or the lien holder. Usually, the signature must be witnessed by a notary public who affixes their seal to the deed. The deed or lien must be written and legible.

Deeds, liens, and other recorded documents are stored in books by the county real estate clerk. When a new deed is received for recording, it is stamped with the deed book where it will be stored with the page number within the book. In modern times, this is done electronically, and physical books are falling out of use. Some states, like Tennessee, have moved over to totally electronic recording, and just stamp the deed with a document number. Though the old deeds are still referred to by their book and page. Once a deed has been recorded, it's book and page numbers, or document number, will be its place for reference forever. Other deeds or liens will cross-reference to the deed by using its deed book and page number.

The county clerk will usually charge a fee for recording.

Recording provides constructive notice to the world of a change in ownership of real property, or of the existence of a lien. Constructive notice means that, even though a person wasn't specifically told of the recording, everyone is deemed by law to know about it because of the nature of the public recording. This is different from actual notice, when a person is specifically told or made aware of the existence of a deed. The assumption is that anyone who is interested in the parcel of real estate will check the real estate records and deeds, to find out about ownership or liens. If they do not take the time to check, that is at their own risk. They will be subject to any deed or liens that have been recorded because of the principle of constructive notice.

In addition, recording deeds and liens establishes priority. The first document recorded has the highest priority, meaning it is the one that has the most affect. Priority is usually established by time. The first deed or lien recorded gets the highest priority. At a typical real estate closing, all liens are paid off, like the mortgage or any tax liens, before the new warranty deed, changing ownership, is recorded.

By clearing out all the other liens, the warranty deed will get the highest priority. If the deed is recorded while an earlier mortgage lien is on the title, then the warranty deed is below the mortgage in priority, and the mortgage lender can take the property very easily. More common, if there are multiple judgment liens on the title to a property, the judgment lien, recorded first, will get the first crack at proceeds from the sale of the property. If there is no money left for later lien holders, they are out of luck. There is a concept of super-priority, which is created by state law. Often tax liens get higher priority than other liens. Sometimes condominium liens also get higher priority.

Key Terms

Actual Notice

Express or implied knowledge of a fact.

Constructive Notice

Notice of the condition of title to real property given by the official records of a government entity which does not require actual knowledge of the information.

Recording

The process of placing a document on file with a designated public official for public notice. This public official is usually a county officer known as the County Recorder who designates the fact that a document has been presented for recording by placing a recording stamp upon it indicating the time of day and the date when it was officially place on file. Documents filed with the Recorder are considered to be placed on open notice to the general public of that county.

13.11 Types of Liens

Transcript

A lien is a claim against the property of another. Liens are usually recorded in real estate records like deeds. They let the world know who has a claim against property, how much the claim is, and when the claim was filed, establishing priority. A lien is usually filed to make sure that the lien holder is paid before title to the lien-debtor's property can pass to someone else.

There are many types of liens. The basis for the claim, the type of claimant, and the rights of the lien holder are all reflected in the different types of liens.

A voluntary lien is one where the landowner himself signs to place the lien on the property. This is a voluntary act done by consent of the owner. The most common type is a mortgage. A mortgage is the bank's claim to the property should the owner miss mortgage payments. Any time real property is used as collateral for a loan, it will be through a voluntary lien, like a mortgage or security deed.

On the other side are involuntary liens. This type of lien is placed on the real estate without the owner's consent, but usually because the owner failed to follow an obligation. Common types of involuntary liens are: state or local tax liens for unpaid property taxes, IRS liens for owing money to the IRS, homeowners association or condominium liens for unpaid dues, and judgment liens.

When renovation is being done on a house, or the house itself is being built, it is common for the contractors and sub-contractors to file a mechanic's or materialman's lien on the property undergoing renovation. This secures payment for the work being done. Each state has its own system of dealing with mechanic's liens. For example, if the contractor during the renovation wishes to exercise his rights under the lien and file a lawsuit for unpaid bills, he must do so within one year of filing the lien, and file a notice in the real estate records that a lawsuit has been filed. Otherwise, when a person searches the title to the property and finds the mechanic's lien, if it's more than one year old the title searcher will assume that it is expired as a matter of law. A mechanic's or materialman's lien is essentially voluntary, because the lien would not be placed if the homeowner didn't consent to the work being done.

Similar to mechanic's liens, there are attorney's liens. This type of lien is filed, usually pursuant to a state law, when an attorney is owed money for legal fees. This ensures that if the property is sold, the attorney will get paid before title can pass to the new owner.

Liens can be general or specific. A specific lien relates to one specific parcel of real property. This is common with a mortgage or materialman's line. But a general lien relates to all property owned by a person within the county. Therefore, general liens have to be filed in all counties where the lienholder believes the debtor has property. Tax liens are general liens. A Uniform Commercial Code lien, or UCC lien, is also a general lien, but it usually relates to movable property, or chattel. You may find this in the real estate records, but it's usually recorded with a different office.

There are also statutory liens. These are liens that exist as a matter of law, by operation of a statute, or state law. A lien for condominium association due is statutory in some states. The condominium association does not have to file a lien document in the county real estate records in order to establish its claim, or priority of its claim. The claim exists immediately when the homeowner becomes delinquent in paying dues or assessments, whether or not a lien document is filed. Often, as a matter of courtesy, to give notice to other lien holders, and to make the homeowner take the claim seriously, the condominium association will file a notice of lien in the county real estate records anyway.

There is also something called an equitable lien. This is a lien imposed by a court to maintain fairness. This type of lien can be used when one person is holding the property of another. Judgment liens are also equitable liens. A judgment lien comes into existence when a court issues a money judgment against a defendant. Again, each state has their own rules and procedures. Usually, the judgment creditor takes the court's final order and judgment and has the county clerk issue a lien that is recorded in the real estate records. This will make sure that the judgment is paid off before title to the property is transferred through a sale.

How long liens are valid varies by state and depends on the type of lien. Some expire in a year, some four years, and some never expire. Check your local laws and talk to an experienced attorney to see the status of a lien you encounter during a closing.

Key Terms

Equitable Lien

A lien on property imposed by a court in order to achieve fairness, particularly when someone has possession of property which he/she holds for another.

General Lien

A lien on all of the property of a debtor.

Involuntary Lien

A lien imposed against property without consent of an owner; example – taxes, special assessments, federal income tax liens, etc.

Mechanic’s Lien

A security interest in the title to property for the benefit of those who have supplied labor or materials that improve the property.

Specific Lien

A lien that attaches to one specific property only.

Statutory Lien

A charge or claim upon property that arises by virtue of specific statutes that address the relationship between the property owner and the party given the ability to place the lien.

Voluntary Lien

Any lien placed on property with consent of, or as a result of, the voluntary act of the owner.

13.12 Chain of Title

Transcript

Every parcel of real estate in the United States has a history and a story of its own. The story could be simple, how the land went from one owner to the next throughout the centuries. More likely, the parcel of land that you're closing on has a long and complex history. Over the centuries, land maps were drawn, owners added and subtracted land to their estates, took and paid off mortgages, and allowed easements to be claimed across the land. The story of the parcel of real estate is the chain of title.

Before a closing, the buyer of the property will check the chain of title. The purpose of checking the chain of title is to make sure that the current owner is, in fact, the legal title holder, and there are no questions regarding title. The chain of title means the history of ownership of the property, from the current owner, back to the original land patent, from seller to buyer to seller to buyer. The chain of title also includes all liens, encumbrances, and easements that attached to the property at one time or another. As part of the title search, the buyer must make sure that all liens in the chain have been released. If a link in the chain of title is broken, the person who thinks they own the property may not really have it, and the closing can't go forward. Or if there was an unpaid lien somewhere back in the title history, it may have to be paid off before the closing can occur.

The chain of title is confirmed by a title search. The title search is done by the closing attorney or title agent conducting the closing. Usually, the closing attorney will hire a company that is expert in title searches. They go into the county land records and reconnect all the links in the chain from the current owner. They look at the deed vesting title in the current owner, then look at the deed vesting title in the current owner's grantor, and so on back into history. The title search company will also look at the lien records to see what liens were filed against the property and make sure that they have all been either canceled or accounted for. A good title search company will also research easements to make sure the property can be used as intended. Different states have different rules and customs regarding how far back a title search has to go. Sometimes ten years back is enough to satisfy the title insurance company. Fifty years is also very common. In one famous case, a title insurance company in Louisiana demanded that title for a property be searched all the way back to the Louisiana Purchase of 1803!

The title search company will produce an abstract of title. The abstract is a summary of the title history showing continuity of ownership, payment of taxes, placing and cancellation of liens, and significant easements on the property. The abstract will also identify issues that may have to be cleared up. Issues can be as minimal as an unpaid tax bill or as significant as a break in the chain of title, which would draw current ownership into question. The abstract will also confirm that the legal description correctly describes the property under closing. The title abstract is sent to the closing attorney with the documents supporting the abstract, including copies of the referenced deeds, liens, and easements.

The closing attorney will review the abstract and the accompanying documents and issue an attorney's opinion of title. The attorney's opinion is the legal determination of the condition of title to the property. If the property has no title defects, meaning the chain of title is complete, and there are no outstanding lien or easement issues, the attorney will issue an opinion that the property is ready for closing and title insurance can be issued. However, if there is a cloud on title, meaning there is something keeping the current owner from saying he owns the property "free and clear," then the attorney will issue an opinion identifying the cloud on the title and, depending on the circumstances, recommend options to resolve the problem. A cloud on title can include a deed in the chain of title that is not legally sufficient or there could be errors such as, a property line dispute, a pending lawsuit relating to the property, or an old mortgage lien that was not properly canceled of record. To fix these issues and establish a complete chain of the title, the attorney could recommend simple actions, like having a corrective deed filed, or may need to file a quiet title lawsuit.

Key Terms

Chain of Title

A history of conveyances and encumbrances affecting the title from the time the original patent was granted, or as far back as records are available, used to determine how title came to be vested in current owner.

Abstract of Title

A summary or digest of all transfers, conveyances, legal proceedings, and any other facts relied on as evidence of title, showing continuity of ownership, together with any other elements of record which may impair title.

Opinion of Title

An attorney’s written evaluation of the condition of the title to a parcel of land after examination of the abstract of title.

13.13 Marketable Title

Transcript

Using the chain of title, the closing attorney will determine whether the property up for sale has marketable title. Generally, in order to close a deal, the property will have to have marketable title. Marketable title means title to real property that a reasonable purchaser, after being informed of the facts and legal importance regarding the title to the property, and acting with reasonable care, would, or should, be willing to accept title and proceed with the closing. Marketable title is key for lenders and title insurance underwriters. As a basic standard, title must be marketable for the lender to issue a mortgage loan to purchase the property, and for a title insurance company to issue a policy insuring the clearance of title.

It's easier to understand what marketable title is if we look at it from the point of view of what makes title not marketable. A number of factors could lead to title being considered not marketable.

- There may be a flaw in the legal description. As title passed from one owner to the next, by deed after deed, it's possible that a clerk made an error in typing up a legal description. The owner may have no idea that there is a mistake in his property line because a survey hadn't been done for decades. And the flaw may be so small that subsequent attorneys missed the error. This would require corrective deeds or other legal action to make the title marketable.

- A break in the chain of title is a big problem for marketability. This could happen because a deed in the title history was cross-referenced incorrectly, and there is a valid deed out there completing the chain, but no one knows where it's recorded. It's also possible that someone in the chain of title thought they had title to the property when they didn't. This is common in situations of divorce, family gifts, and estates. Similar to flaws in the legal description, this will need legal action to make the title marketable.

- An unresolved lien on the property will make it unmarketable. At some point in the title history, if a mortgage, mechanic's lien, judgment lien, tax lien, or any other type of lien had not been paid off prior to the property being transferred, the lien is still valid, and may be superior in priority to the warranty deed itself. This creates a significant cloud on title that must be resolved prior to closing.

- Unexpected easements, shifting boundaries, and a survey that reveals encroachment by a neighboring land owner can all cause problems for marketable title. If the legal description established certain boundaries, but over the years, a neighboring land owner built a fence into the subject property, or gained an easement by years of using a path through the subject property, that can cause title to not be marketable.

The standard for marketable title does not require absolute assurance that the chain of title is perfect. The standard is whether a reasonable person would accept title, given the flaws. For example, an unpaid lien that is well-beyond the statute of limitations for enforcement may be a cloud on title, but the property will still have marketable title.

Key Terms

Marketable Title

Title which a reasonable purchaser, informed as to the facts and their legal importance and acting with reasonable care, would be willing and ought to accept.

13.14 Proof of Ownership

Transcript

Knowing who owns a parcel of real property should be a simple matter. But when it comes to a real estate closing, where hundreds of thousands, and sometimes millions, of dollars are at stake, you must be absolutely sure that the person who claims to own the property has title to the property. A closing or title insurance attorney will issue a certificate of title, prior to closing, stating who definitely owns a parcel of real estate. To make this determination, the attorney looks at the chain of title, abstract, and all available documents and information to confirm that the last grantee, on the last deed, has good, clear title to the property. The attorney has made sure there are no breaks in the chain of title, and there are no questions about the legitimacy of each and every deed in the title history.

But it's difficult to be 100% sure. For that reason, we have title insurance. A title insurance policy is purchased by the purchaser in a real estate transaction. Often, if the buyer is using a mortgage lender, for purchase money, the lender will also require a title insurance policy.

Title insurance will cover losses incurred if it turns out there is a problem with the title after closing. The lender's insurance policy will cover the amount of the loan, while the owner's policy will cover the full value of the property.

Most title insurance companies offer standard and extended coverage policies. Standard policies cover defects in the chain of title that can be found off record, or documents filed with the county clerk's office or tax office. Extended policy terms cover those defects that cannot be found in the documents.

The standard policy will cover documents mistakes. These can include: a forged deed; a deed with a grantor who did not have capacity to sign; a deed without a necessary party, such as a spouse or second owner on title; mistakes in the legal description; trouble caused by an easement that was filed of record, but not found in the title search; a lien or mortgage that was not canceled, which was recorded in the county, but not found during the title search; or a deed that was recorded improperly, with the incorrect indexing information in the clerk's office making it difficult to locate.

Extended policy coverage includes matters that are not found in the written records. These can include: violations of community association covenants, claims of adverse possession, unrecorded liens or claims on the property, mistakes in the survey of the property, and encroachment by neighboring buildings on the property.

When a claim is made on the title insurance policy there are a couple of ways the insurance company will handle the claim. If the matter is an unpaid lien or claim against the property, title insurance will try to defend against the claim, and will pay it off if necessary. Title insurance can pay the legal fees to draft and file corrective deeds, where such solution is available. For questions regarding the property line and encroachment, title insurance will file a quiet title lawsuit to protect the integrity of the property's boundaries. In worst case scenarios, title insurance can pay off a loan or re-pay the value of the property to the owner if title is ultimately lost.

A title insurance policy lasts as long as the owner holds title to the property, and sometimes for several years thereafter.

The cost of title insurance varies by state and company. There are dozens of title insurance companies operating in the United States with varying levels of coverage and customer service. Cost is usually calculated based on the purchase price or loan amount of the property, being a certain amount "per thousand." For example, if a property is $200,000, and the company charges $2.00 per thousand, the policy will cost $400.

Title insurance is a closing cost usually paid by the purchaser. It is entirely voluntary to buy an owner's title insurance policy, though it is strongly encouraged by most closing attorneys and real estate experts. The lender's policy will not be voluntary if you have a mortgage lender.

Key Terms

Certificate of Title

A written opinion by an attorney that ownership of a particular parcel of land is as stated in the certificate.

Title Insurance

Insurance to protect a real property owner or lender up to a specified amount against certain types of loses, e.g., defective or unmarketable title.

13.15 Title Problems and Methods to

Transcript

The chain of title to a parcel of real property traces its history from the current owner, backward in time, owner by owner. Occasionally, the chain of title has a break or an unresolved issue. These can include deeds that are out of sequence, unpaid liens, an incorrect legal description, or encroachment by an adjoining neighbor. This is referred to as a cloud on title. Any issue that throws the current ownership of a property, or the rights of the property owner into question, is a cloud on title.

Many title issues can be resolved by filing a corrective deed or paying off a lien. Sometimes an issue is so serious that an attorney must file a lawsuit to quiet title.

A suit to quiet title is an equitable action filed by the landowner against a specific person (causing the cloud), or against the entire world to make sure that no one has a claim against the property. The quiet title lawsuit will tell the court about the cloud on title, how it came to be, and why the law requires that the cloud be lifted and how it can be done.

A simple example is as follows: Smith owns a house with the land around it. When Smith wanted to refinance his mortgage, a title search revealed that a mortgage from 15 years earlier, signed by a prior own, had never been canceled by the mortgage company. Smith's attorney tried to contact the mortgage lender but it was out of business. So, Smith filed a quiet title lawsuit against the bank, and the entire world to make sure that no successor bank owned the rights to the mortgage. The bank's last known address and executives are served with the lawsuit. If no one answers, Smith presents his evidence to the judge that the mortgage must have been paid off because the property was sold multiple times, and no one has made a claim against the property for over a decade. Smith will show that the bank is out of business, and despite notice, has not objected to the relief sought. Smith asks the judge to issue an order voiding the mortgage and for the order to be recorded in the county real estate records. Thus, the cloud on title is lifted.

Key Terms

Cloud on Title

A claim, encumbrance or condition which impairs the title to real property until disproved or eliminated as for example through a quitclaim deed or quiet title legal action.

13.16 Uniform Commercial Code

Transcript

The Uniform Commercial Code, or UCC is a body of laws concerning chattel, or movable property. It has nine sections that deal with commercial transactions of goods. While commercial law is almost always state law, the UCC was adopted by nearly every state, though each state adds its own wrinkles and court-based law applying the UCC. Much of it involves common sense contract law. But a good deal is devoted to arcane and abstract concepts that most normal people will never see in their lives.

Since the UCC deals only with goods and movable property, why do we care about it in the real estate world? Primarily because of the UCC-1. The UCC-1 is a lien created by the code. Similar to a mortgage, the UCC-1 is a lien on property used as collateral for a loan. In the UCC, the lien involves a loan to purchase goods rather than real estate. The UCC-1 can cover the specific goods, like inventory for a store, or a couch in a person's home. But the UCC-1 can also be a blanket lien, which covers all property owned by the borrower, both movable property and real estate.

For the UCC-1 to be valid, it must be signed by the borrower. UCC-1 forms are usually filed separately from real estate records. Some states have the secretary of state handle these filings rather than the real estate clerk. Other states have a special section of the real estate clerk archive these filings. But to be valid against real estate, the UCC-1 lien must be recorded in the real estate records just like any other lien or mortgage. This way, when a title search is done, prospective buyers, or lenders, will know that there is a lien on the property and that is has to be paid off before the property can be sold free and clear.

Key Terms

Uniform Commercial Code

Establishes a unified and comprehensive method for regulation of security transactions in personal property, superseding the existing statutes on chattel mortgages, conditional sales, trust receipts, assignment of accounts receivable and others in this field.

COPYRIGHTED CONTENT: