Chapter 16 - Legislation Affecting Financing

Learning Objectives

At the completion of this chapter, students will be able to do the following:

1) List at least one requirement under TILA.

2) List at least one document required to be used by lenders under RESPA.

16.1

Transcript

The Truth in Lending Act, also known as Regulation Z, is a federal law enacted in 1968 to protect consumers. Specifically, TILA was designed to make sure consumers are provided with various types of disclosures by creditors when the consumer is looking to take on debt. After the recent mortgage crisis, the Consumer Financial Protection Bureau (C.F.P.B.) was tasked with making various changes to TILA to improve the disclosures and provide the consumers with additional time to make an informed decision.

There are three main requirements for lenders under TILA which are: (1) the disclosure requirements, (2) the three-day right of rescission, and (3) the advertising guidelines. In this lesson, we will discuss the three requirements of TILA and how those requirements can impact you as a real estate agent.

When you think about TILA, it is important to remember the law is in place to ensure the correct disclosures are given to the borrow so that they can make an informed decision. Put simply, the law requires certain disclosures be made to the borrowers so that they understand the actual cost of borrowing the money, and have the opportunity to compare offers with other lenders. Before TILA, consumers could be pressured at the last minute to agree to additional charges in order for the loan to be funded.

As an agent when you are discussing the loan process with a client, it is important to remember that TILA does not regulate the actual cost of borrowing, it just dictates the information that must be disclosed to the client about the cost of borrowing.

There are five different types of loans that are covered by TILA, and they are:

- residential,

- federally related,

- 1 to 4 family properties,

- non-commercial properties, and

- family farms

Commercial transactions are not covered by TILA.

TILA requires lenders to disclose all finance charges, including the true annual interest rate before the buyer can enter into the transaction.

In October of 2015, new rules were put in place to further protect the consumer from entering into a transaction in which they were not aware of the real cost of lending. The new rules include the TILA-RESPA Integrated Disclosure Rule which requires the lender to disclose particular information at certain points in the process.

The first disclosure which is called the Loan Estimate must me made three days after the purchaser submits specific information to the lender. Once the following information is provided to the lender the first disclosure must be made:

Name, Income, Social Security number, the address of the home they hope to purchase, an estimate of the home’s value (typically the sale price) and the amount they want to borrow.

The second disclosure that needs to be made is the closing disclosure which is often referred to as the CD. This is the disclosure that as a real estate agent you need to be most familiar with, to avoid closing delays. The lender must deliver to the buyer the closing statement 3 business days before closing. The three-day period gives the purchaser the opportunity to review the final numbers and compare them to the original loan estimate. If a change is made to the closing disclosure that impacts buyers cost of lending significantly, the disclosure must be redelivered and a new three-day review period is triggered.

The three top changes that trigger a new review period are as follows:

1.The APR increased more than ⅛ on a fixed rate loan or ¼ on an adjustable loan.

2.A prepayment penalty is added.

3.The lender changes the type of loan. For example, if the borrower applies for a fixed rate loan and then within the three day period it is switched to a new loan such as interest only loan the review period is triggered.

Let's take a moment to review how this might impact a buyer's settlement

If the purchaser is scheduled to close on Monday, April 1 then the disclosure must be delivered by March, 29. If the lender only provides the disclosure on March 30th then the buyer will not be allowed to settle until Tuesday, April 2nd. As a real estate agent, it is important to check in with your client and the lender to ensure the disclosure is sent out on time.

The second crucial aspect of the TILA is the borrower's three-day right of rescission.

This right covers people who are refinancing or taking out a home equity line; it does not cover the purchase of a home. To put it simply if you are using your home as collateral then, under TILA, you are guaranteed the right to change your mind within three business days. There are certain events that must take place to start the three day period, and they are as follows:

- The credit contract has been signed

- The borrower has received a closing disclosure

- The borrower has received two notices explaining the right to rescind.

Once all three of these events take place, the clock starts ticking and the review period is three business days.

In the notice, the lender provided to the borrower, there should be instructions on what they need to do if they want to exercise their right. If for some reason that is not included, the borrower should put in writing their intent to rescind and send it in a manner that the paperwork can be tracked.

IMPORTANT NOTE: It is imperative that real estate agents remember that when it comes to all things TILA, business days include Saturday even if the lender is closed!

Let’s take a look at an example in which the right to rescind might come in handy for a client.

As a real estate agent you might have clients who simply could not find the perfect home, so instead of buying, they decide to add an addition to their home. In order to do so, they take out a home equity loan to pay for the addition. One day after closing on the loan, the perfect house comes on the market. Under the three-day rule, they can cancel the loan and move forward with the purchase of their dream home.

The rules under TILA for advertising are also important concepts for real estate agents to be familiar with. The law outlines that when certain words or phrases are used in an advertisement, often referred to as “trigger” words, will result in the advertiser needing to make additional disclosures. Here we will review the trigger phrases and discuss what additional disclosures each one triggers.

There are five main triggers:

1.The amount or a percentage of a down payment.

2.The number of payments

3.The length of time for the repayment

4.The amount of any payment.

5.The amount of a finance charge or stating that there is no charge for credit.

One common misconception is that “no down payment” is a trigger when in fact that is not the case.

It is important to remember that if any of the five triggers is mentioned then ALL of the following must be disclosed:

- The terms of the repayment of the loan

- The annual percentage rate and any potential increases

- The total finance charge

- The total number of payments and the date those payments are due

- The amount or a percentage of a down payment.

In order for a lender to be subject to TILA advertising guidelines, they need to lend funds at least 25 times on an annual basis and/or five loans a year must be housing loans. This is important for real estate agents to remember!

For example: Let’s say your buyer sees an advertisement for a lot “by owner” with the words “own the land in just three payments.” Due to the fact that this owner is not subject to TILA, he or she is not required to make additional disclosures. As a real estate agent, you will want to make sure your client has all the necessary information on the transaction before moving forward with any type of “seller financing” plan.

Now we will review the penalties if the rules are violated.

When the changes to TILA became active in October of 2015, lenders worked hard to make sure their policies were in compliance with the new regulations. One of the reasons the banks and lenders worked so hard is the penalties for noncompliance of TILA are steep.

If a lender fails to deliver the proper disclosures they can be held liable as follows:

- Actual damages the borrower incurs as a result of the failure to disclose.

- Statutory Damages as defined by law which typically range from $400-$4,000.

As a real estate agent, you will be most concerned with the actual damages suffered by the borrower. For example, if the lender fails to make a disclosure to a borrower at the time of the loan estimate and the borrower signs a contract based on that estimate. When the borrower goes to close on the house, they realize certain charges are due, and the borrow is not prepared to deliver the extra funds at closing and must default on the contract. The borrower most likely loses the earnest money deposit being held in escrow, and this would be actual damages suffered by the borrower.

The major fines are levied by the Consumer Financial Protection Bureau in one of three tiers.

The first tier violation penalties can run $5,000 per day, per violation. Second Tier Violations are considered “reckless” actions that will cost the lender $25,000 per violation per day. Finally, third tier violation will cost the lender a whopping 1 million dollars per day, per violation. Third tier violations mean the lender knowingly broke the rules.

As a real estate agent having a reputable network of lenders to recommend to your clients will help them avoid lenders who violate the rules under TILA.

For the last part of this lesson, we will review how the TILA impacts your day to day activities as a real estate agent.

TILA was designed to help ensure consumers are provided with appropriate information prior to entering into a loan agreement, and the lender is ultimately responsible for ensuring the information is provided. However, as a real estate agent it is imperative you are familiar with the rules to help guide your client to a successful settlement.

As an agent, you should be familiar with the lender's requirement to provide the borrower with the final closing statement 3 business days before settlement. A good agent will confirm with the lender, client, and settlement company that this occurred prior to the deadline. If you are the agent representing the seller, you should confirm this information with the buyer's lender and agent to ensure your seller will be able to close the transaction as anticipated.

As an agent, it is crucial that you provide the lender with any credits or commission changes that need to be approved for the closing statement in ample time. If a last minute credit comes up, it could potentially change the closing statement enough that a new three-day review period is triggered.

Under TILA, the settlement agent must provide the lender with certain financial information with 10 to14 days of closing. As an agent it is imperative, you provide the settlement agent with your commission, administrative charges, commission credits and license information in a timely fashion, so that the title company can be in compliance, and provide this information in time to the lender.

Key Terms

Truth-in-Lending Act (TILA)

The name given to the federal statutes and regulations (Regulation Z) which are designed primarily to ensure that prospective borrowers and purchasers of credit receive credit cost information before entering into a transaction.

16.2 Equal Credit Opportunity Act (ECOA)

Transcript

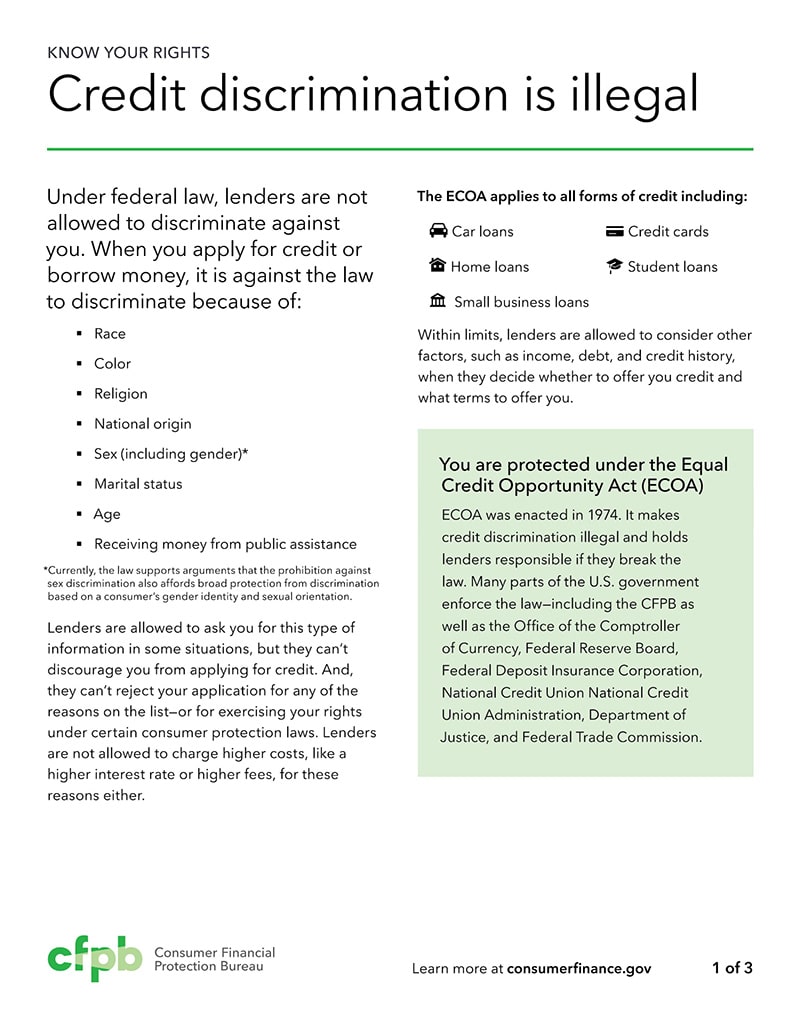

The Equal Credit Opportunity Act, better known by its acronym ECOA, was enacted in 1974. The ECOA has four main parts.

These are:

- First - the definition of discrimination in credit lending.

- Second - the credit applicant rights to a notice of credit decisions and related information.

- Third - the actual notice of the ECOA applying to the borrower, the credit decision made on his application and the reasons for the decision (approval or denial or change).

- And finally - recordkeeping.

The ECOA as a financing regulatory law is very broad. It covers all types of credit transactions, regardless of whether they are for a consumer or a business seeking commercial loans. And all lender types are included in this scope as well.

Now, let’s discuss what is prohibited under the ECOA

Under the ECOA when a consumer applies for a loan, a lender is forbidden from the following:

First, no applicant can be persuaded or stopped from applying, or have an application denied based on race, color, religion, national origin, sex, marital status, age, or due to receiving any kind of public assistance program. For example a woman cannot be denied the ability to apply for credit because she receives women, infants and/or children monthly support.

Second, using an applicant’s race, gender or birthplace as a factor for a credit decision is prohibited. However, this rule does not bar an applicant from providing the same information voluntarily. Applicant immigration status, on the other hand, is allowable because it goes to the heart of whether the person borrowing funds will be in the country long enough to pay them back.

Third, varying the terms of lending on an applicant due to being a member of a protected class (race, gender, religion, national origin etc.) or for a reason associated with a protected class, it is prohibited. For example, charging a higher interest on a borrower because he is buying a home in a predominantly African-American neighborhood.

And finally, asking for information on the marital status of an applicant to determine if he or she is divorced or widowed. The lender, however, can ask if a person is married, single or separated. A common issue prior to the ECOA was with lenders not wanting to lend to divorced or widowed women, assuming they couldn't generate sufficient income to pay a loan.

There are some additional concerns to watch out for regarding marital status. Lenders have some restricted leeway which they are able to use (carefully) when asking for information from the borrowers. It was recognized that lenders should be able to get to the true nature of an applicant’s income status but not use marital status alone as a reason for credit approval or denial. So, under the ECOA marriage status information requests are restricted as follows:

First, a lender can ask about marital status if an applicant is seeking his or her own individual account for unsecured debt. This information request types are most common in states with community property laws, i.e. where being married automatically gives a spouse 50 percent control of any property gained during the marriage.

Second, the information on marital status can also be asked for, at any time, in any state, where the account would be shared with a spouse or where the property is used as collateral. Again, this is needed in order to assert clear title status.

Third, any information about children or having children is not allowed to be requested either. Dependent care costs, however, can be requested.

And finally, child support, alimony or other legal arrangements can be sought out by the lender only if they warn the applicant in advance that he/she is not required to provide such information and that choosing to provide this information is deemed voluntary. However, if the applicant is paying out support expenses, then they are fair game for review.

Interestingly, age is not an area to worry about in terms of discrimination.

Age, as credit criteria is restricted to (1) whether the applicant is too young to enter into a contract (meaning the applicant is under 18 years of age) or (2) the applicant is over 62 years of age. Anyone’s age can be used as an indirect factor when it has an impact on income.

For example, if an applicant makes $100,000 annually, but he is about to retire in a year, that would be a big issue when deciding on a $50,000 credit line request.

Now, let’s discuss what the ECOA requires of lenders

The ECOA requirements for lenders begin with providing an application to a potential borrower (in terms of notice) and continue into the decision to approve, or not, as well as how that decision is communicated back to the applicant.

For all applicants, the following application notice (from a lender) is the best advised approach:

“Notice: The Federal Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, marital status, age because all or part of the applicant’s income derives from any public assistance program or because the applicant has, in good faith, exercised any right under the Consumer Credit Protection Act. The federal agency that administers compliance with the law concerning this credit is the Federal Trade Commission, Division of Credit Practices, 6th & Pennsylvania Ave., NW, Washington, DC 20580."

So, what is an adverse credit decision?

Under the ECOA, an adverse action can be any of the following situations regarding credit:

- Number 1 - denial of credit to an applicant.

- Number 2 - approving credit but the amount offered is less than what was originally requested by the applicant.

- Number 3 - denying a credit increase on an existing account when it is requested.

- Number 4 - closing an existing credit account…and

- Number 5 - changing the account terms that have a negative impact on the account holder.

However, an adverse decision does not include an across-the-board change by a lender to all of its accounts at the same time, even if negative. A common example would be a fee increase for cash advances on all credit card accounts. Since it affects all account holders, it is not an adverse decision under the ECOA even though the effect means a cash advance is now more expensive for all the customers of a given lender.

In terms of the credit decision process, lenders under the ECOA have to make sure their systems follow the law as well. For example, creditors are allowed to consider whether an applicant has a dedicated communication tool (for example: a confirmed phone account). This is logical as creditors want to be able to contact the borrowers in case problems come up.

Lenders also can’t apply or offer discounts to a borrower simply because of gender or marriage status. Other business practices banned from being a reason for denial include whether the applicant depends on an annuity, part-time versus full-time work, of if an applicant receives a pension or Social Security.

Finally, income from alimony, child support or another legal marital arrangement cannot be the reason for reducing the credit offered. Lenders can however require documentation of income sources to validate them. For example, Sarah gets half of her income from alimony and then works part-time as a graphic designer. Asking for both her work and alimony income would be a legitimate request by the lender in order to approve the credit.

The decision notice to the applicants under the ECOA depends a lot on the type of customer. The ECOA does make a difference between customers who are large-scale borrowers versus those who are smaller or private consumers.

For commercial borrowers, the decision notice differences are specific to their revenue levels. For example, if a commercial applicant generated over $1 million in prior year gross revenue, or is seeking credit via a line, or credit or a trade line, then the creditor providing the decision must:

- Provide an ECOA notice which can be in writing or as a verbal notice.

- Provide a credit decision within a reasonable time, once the application is submitted.

- Give a clear decision on a credit approval, provide a different offer than what was requested, or provide an adverse response… and

- Provide a written response within 60 days from an adverse decision where the response has to include the reason for denial and the general ECOA notice. For such a response to be provided the applicant must submit an official request.

On the other hand, if an applicant was a smaller business, such as one that generated less than $1 million in revenue, the creditor has to provide the credit decision within 30 days once an application has been received. The noticing and archiving of records is the same as the larger company applicant.

So, which approach is better with business customers? That decision depends on the given creditor’s operations and its customer base, at least in terms of commercial accounts. Some creative lenders have simply decided to combine both groups.

A typical hybrid approach would:

- Provide an ECOA notice in writing to anyone right from the start.

- Provide the decision notice within 30 days of an received application … and

- Provide the reason for any type of adverse action.

Another area of credit noticing that gets some attention is that of co-applicants. Under the ECOA, only one of the co-applicants, on a loan application, has to be notified about a decision, not both. So, if Henry and his partner Joe go in for a loan as co-applicants, the bank lender only has to notify one of them of the decision. However, many lenders just provide the notice to both co-applicants anyways as it avoids unnecessary conflicts.

Next, let’s discuss recordkeeping requirements under the ECOA

Like other types of federal law when it comes to financial transactions, recordkeeping is a big part of the ECOA. Specifically, the ECOA is intended to create a paper trail so that a decision can’t disappear quickly after it’s made.

On the consumer side, a lender must keep and maintain an applicant’s records for up to 25 months. On the commercial side, creditors with applicants who generate more than $1 million annually in income must keep records at least 60 days after providing an ECOA notice to the applicant. Where the credit line was not extended and the applicant wants to know why, the lender has to keep the records on file for 12 months (a full calendar year). The same applies if the applicant specifically asks for the records to be kept in place, regardless of credit being approved or not approved. And record retention applies completely in any case where an applicant generates less than $1 million in gross revenue annually.

What you’ve heard so far in this lesson is a detailed overview of the ECOA.

While the ECOA will not directly impact your day-to-day actions as a real estate agent, it is important to know what rules and regulations lenders are required to follow when determining if a homebuyer is eligible to receive a loan. A client’s ability to borrow is fundamental for purchasing a property and you must be aware of what could impact a borrower’s ability to purchase a property. About 95% of home owners are taking out a mortgage loan in order to afford purchasing a property. So, in most cases you will only be able to make a sale if your client has the ability borrow money for their mortgage.

Key Terms

16.2a ECOA: Know Your Rights

Please spend a few minutes reviewing the document below.

16.3 Legislation Affecting Financing: Fair Housing Laws

Transcript

As a real estate agent, you should be well versed on fair housing laws and how they relate to your actions, advertisements, and conversations with your clients. However, lenders are also responsible for adhering to various fair housing laws, and you should also be familiar with these concepts. In this chapter, we will review in detail fair housing laws and how they relate to financing.

First, we will examine what is prohibited under the Federal Fair Housing Act and then take a look at some real world examples. Lenders are prohibited from denying the following services based on race, color, national origin, religion, sex, familial status or handicap.

- Lenders cannot refuse to issue a mortgage or refinance a loan. This item is pretty straight forward. If someone feels they are financially sound enough to qualify for a mortgage but are denied for no apparent reason, they may want to consider filing a complaint.

- Lenders cannot refuse to provide information about loan programs.

- Lenders cannot try to impact an appraisal. This practice is also referred to as low balling (we will review this later in the chapter).

- Lenders cannot impose a higher rate or adverse payment terms. Applicants should be offered similar terms as anyone who has identical or similar finances.

- Lenders cannot offer different terms for purchasing a loan.

The courts have recognized three different types of lending discrimination. Now we will briefly review each one and provide a few examples.

Overt Evidence of Disparate treatment can be shown to exist through actual statements showing the lender took into consideration a prohibited factor when making a lending decision. Also, disparate treatment can be demonstrated by presenting evidence that one was treated differently which cannot be explained by the lender showing nondiscriminatory factors such as income or credit history.

Consider overt evidence of disparate treatment as blatant prejudice in lending practices. For example, if someone walks into a bank and is told they cannot have a loan due to their race, this is considered overt evidence.

The second type is Comparative Evidence of Disparate Treatment, and it is much more likely to occur. Comparative evidence often happens with applicants that are considered “on the line” applicants, meaning their approval criteria is the middle of the road and the lender has more discretion as to whether or not to issue an approval. Without a perfect financial history, the type of discrimination can be difficult to prove.

Let's take a look at an example.

Suppose you have two loan candidates with the same credit and income, both looking to purchase similar homes in the same neighborhood and both have the same amount of late payments on their credit history. The lender approves the white applicant for the loan, but a black person is denied. In the case, the applicant could claim disparate treatment. If looked at each case, on its own, the late payments might seem like a reason to deny the loan; however, if you look at these cases side-by-side you can see the comparative evidence.

Disparate Impact occurs when a lending institution applies a neutral policy equally across applicants; however, the policy results in a group of people being unfairly burdened or excluded. This type of discrimination may not be intentional, but it can have a negative impact on a large group of people for an extended period of time.

Let's take a look at an example that has occurred quite a few times in a real world.

A lender makes a policy that the minimum loan they will issue in a particular state is $250,000. This system is not put in place knowing it would hurt anyone but was purely a business decision. The policy remains in place for 15 years, and when the statistics are reviewed years later, it shows that this policy has led to almost no minorities being issued loans because their loans typically fall under the bank's minimum loan requirement in this state. While the bank did not initially go out to discriminate, this can be seen by the courts as disparate impact. It is important for banks to carefully review their policies and make sure they do not inadvertently discriminate.

As a real estate agent, it is not your responsibility to review your client's loan terms or denial of financing to determine if there has been discrimination. Lending can be a sensitive situation especially if your client is denied. It is, however, important for you to be aware of the resources available to your client in the event they feel they have been discriminated against.

They can file a formal complaint on the US Department of Housing and Urban Development website.

Also, they should hire an attorney to represent their interests in the legal matter.

Now we will review Redlining.

Unfortunately, redlining has played a large role in lending throughout history and as a result is an important part of real estate education that you should know and be aware of, when working with clients.

The Housing Act of 1968 explicitly prohibits the practice of redlining. Redlining involves denying a person based on their race, color, national origin, religion, sex, familial status or handicap in a particular area based on the demographics in that area. Redlining means that lenders are drawing lines around specific neighborhoods and decide, in advance, not to approve loans in that area based on the racial or ethnic makeup of the neighborhood.

Redlining does not mean lenders have to approve all loans in minority neighborhoods, or otherwise be accused of breaking the law. Lenders can take the following factors into consideration when approving or denying a loan:

- Credit History

- Income

- Property condition. Property condition includes not only the condition of the property in question but also the condition of the properties in the surrounding area.

- Neighborhood amenities and city services provided to the neighborhood. These types of considerations can impact the value of the home in question.

- Lender's portfolio: the lender can take into consideration how that particular loan will affect the organization's overall risk profile.

Let's take a look at a recent case that resulted in one of the largest settlements in history.

Hudson City Saving Bank was ordered to pay a $33 Million dollar settlement for avoiding issuing loans to Latinos and African Americans in minority neighborhoods. Prosecutors were able to show that even though the bank went through a significant expansion, less than 6% of the new branches were opened in minority neighborhoods. It was clear the bank was actively avoiding lending to minority groups. As a result, the bank had to make a large payout as well as open new branches in the minority neighborhoods they had avoided.

There are many real life examples in recent years that indicate redlining still remains an issue in minority neighborhoods. As an agent, you should be aware of the seriousness of the situation and be able to point your clients in the right direction if they feel they are being discriminated against.

Now we will review the various Regulations and Statutes that are addressed by the Federal Fair Housing Act and review some specific acts it prohibits. It is important to keep in mind that the act was written broadly to encompass a wide range of activities that could be considered discrimination.

One of the main parts of the act is focused on redlining, but since we covered that earlier in the chapter, we will concentrate on the other parts of the statue.

The Fair Housing Act specifically prohibits lowballing. Lowballing occurs when a low appraisal is made based on discrimination. This is a form of redlining and can force the borrower to have to cancel the sales contract or have to pay the difference between the price and the loan amount. If a lender wanted to discriminate against the borrower but could find no valid reason to deny the loan, trying to push for a low appraisal would be another way to deny the loan.

For example, let's say a lender does not want a loan to go through due to the applicant’s religion, but could find no reason to deny the application. They could try to get the appraisal to come in low knowing the buyer most likely does not have the cash to make up the price difference and will be forced to cancel the contract through the appraisal contingency. After the mortgage crisis, lenders and appraisers cannot be in contact anymore. There should be an independent third party between them to avoid conflicts. However, lowballing is a practice that as an agent you should be aware of.

The Fair Housing Act also prohibits the use of racially exclusive images. For lenders, this means making sure their advertisements do not appear to only be geared toward a particular race, religion or age group. This extends to advertisements when it comes to languages. For example, if a lender is located in a predominantly Spanish-speaking neighborhood, that does not mean that all of the ads should be geared towards the Latino community. The ads can show that there are Spanish-speaking loan officers; however, the ads should indicate the loan products are available to everyone.

As an agent, you should be aware of these laws and make sure your clients understand they cannot be discriminated against in the lending process. If they mention to you that they feel this may have happened to them, you should inform them about the ability to file a claim.

Also, you want to remind the client that you cannot give legal advice, and they may want to hire an attorney.

The Fair Housing Act also prohibits making the lending process more difficult for applicants as a result of race, color, national origin, religion, sex, familial status or handicap, at various stages of the lending process. There are three main ways that the act addresses the process to prevent potential discrimination.

The first way is to make sure lenders do not apply excessively burdensome qualification standards. Essentially the law indicates that if a lender makes qualifying so burdensome so that in effect is the same as just denying the applicant, then it can be considered discrimination.

The second way the statute accomplishes this is by making it illegal for lenders to impose more onerous terms. This includes interest rates, and terms and conditions.

Finally, the practice of making the application process more difficult in terms of paperwork, etc. for a particular class of people is also prohibited.

As an agent you will learn that the loan process can become very stressful for buyers, it is a lot of paperwork and for too many applicants it seems like the lender is asking for the same information over and over again. However, you should be able to tell if it seems like some of your clients are being forced to jump through hoops that your other clients are not. If this is the case, you may want to encourage your clients to ask a few more questions and consult with an attorney.

Finally, Racial Steering is prohibited under the act. Racial steering is when a lender pushes an applicant towards a particular loan product or geographic area based on race. For example, let's say a buyer is deciding on two properties in two different neighborhoods. If the lender finds out about the two houses and gives the buyer superior loan terms for one of the house in one of the neighborhoods, based on their race, this could be considered racial steering.

Key Terms

Redlining

An illegal lending policy of denying real estate loans on properties in older, changing urban areas, usually with large minority populations, because of alleged higher lending risks without due consideration being given by the lending institution to the credit worthiness of the individual loan applicant.

16.4 Real Estate Settlement Procedures Act (RESPA)

Transcript

RESPA is known as the Real Estate Settlement Procedures Act of 1975 or Regulation X. RESPA was written to ensure that borrowers are provided with important information about the cost of settlement services and ensure the process is free from kickbacks. The act accomplishes these goals in a few ways.

The regulation extends to lenders, mortgage servicers, and mortgage brokers who are required to fulfill the Act's requirements, or face penalties.

The Act prevents kickbacks that historically were taking place throughout the settlement process.

RESPA requires the disclosure of affiliated business relationships so consumers are aware of certain financial benefits a party may be receiving.

RESPA establishes various escrow and accounting guidelines for lenders.

In this lesson, we will review RESPA in detail, while helping you understand how it will impact your day to day dealings in the real estate industry.

The first topic to master with RESPA is to know what types of residential real estate transactions RESPA covers. The short answer is almost all of them.

RESPA was designed to encompass a broad range of real estate transactions by applying to any federally related loan. Since most real estate transactions end up federally regulated in some manner, a majority of transactions are covered including:

- Loans secured by a lien on residential property

- Loan assumption approved by a lender

- Refinancing of residential loans

- Home equity credit lines

- Reverse mortgages

As a residential real estate agent it is unlikely that you will have many transactions not covered by RESPA.

We touched upon the loan estimate and closing disclosure requirements in the TILA lesson. In this section, we will review the timeline for the disclosures and go into further detail about the information provided in the Loan Estimate and Closing Disclosure.

The lender must give the borrower a copy of the loan estimate within three business days of the consumer submitting an application. It is important to remember that a loan estimate does not constitute a loan approval, but is a guide for the borrower to compare various credit offers.

Now we will review the information included in a loan estimate and please pay attention to the following details:

- The estimated interest rate and if it is a fixed or an adjustable rate

- The estimated monthly payment. This is important because the month payment includes items such as insurance and taxes in addition to the principal and interest payment

- The estimate will include the closing costs the borrower can expect to pay

- The form will also include any charges unique to the loan such as a prepayment penalty or a balloon payment.

- A list of services and fees the borrowers cannot shop for, this will include the appraisal fee, credit fee, and fees related to flood monitoring and checks.

- A list of services borrowers can shop for including termite inspections, surveys fees, and title insurance costs.

- Finally, the cash needed to close.

For a real estate agent, the estimate of the money needed to close is important to discuss with your client. Before making an offer, you must talk with your buyers if they will have enough cash on hand to close based on the loan estimate. If not, you will need to make sure that you negotiate in the contract, for the sellers to cover some of the buyer's closing costs as part of the negotiation. It is important for your buyers to understand that the sellers do not have to agree to cover closing costs and they should have a plan to come up with the cash if need be.

The second disclosure made is the Closing Disclosure often referred to as the CD. The CD must be provided to the borrower three business days before closing. Remember when it comes to TILA and RESPA, business days include Saturdays even if the lender is closed!

We will now review the different information that is on the closing disclosure.

The CD should look familiar, as it should be very similar to the loan estimate. If it is not, the borrower should start asking questions! The CD is compared to the estimate and any large differences need an explanation. The entire point of TILA and RESPA is to have the cost of borrowing money to be disclosed ahead of time.

The closing disclosure includes the final numbers for the borrower's actual loan making it a critical document to review carefully. The CD consists of the following key pieces of information:

- Loan amount, interest rate, and monthly payment of interest and principal

- Prepayment penalty, if any

- Balloon payment, if any

- Estimated monthly payment with insurance, escrow, etc. If this differs from the loan estimate, the borrower should find out why.

- Closing costs and cash needed to close.

- Services the borrowers did not shop for

- Services the borrower did shop for

- Other fees: this section will include, real estate commissions, fees to HOAs or condo associations

- If the seller has agreed to pay a credit, this should be on the CD

- Cost of late payment

- Information regarding the escrow account

- Contract Details

As an agent, you should always review the CD and find out if your clients have any questions. It is important for you to check the commission portion of the CD as well as the contract portion which contains your information including license and broker information.

Section 10 of the RESPA regulation covers the rules lenders must follow when it comes to the buyer's escrow account including placing limits on the amount of escrow a lender can require. Almost all lenders will require an escrow account for a buyer that includes payments the lender will make on the borrower's behalf, such as taxes and insurance payments. RESPA requires lenders provide borrowers with an initial escrow statement and annual reports after that.

From an agent perspective, you will never be required to do the actual math on the escrow account. However, questions often come up on the closing disclosure regarding the lender escrow that you can answer for your client. Lenders typically do not attend settlements, so it is important to be familiar with these concepts. For example, if you represent the seller in the transaction, lenders typically hold escrow about 30-60 days post closing. A seller may ask why the mortgage payoff is less than they were anticipating and the answer is the escrow is not released at closing. If you are representing the buyer, there is often a credit from the lender on the closing statement; this is typically because the lender had estimated a higher escrow for the buyer than they are allowed to collect, and therefore the buyer receives a credit at settlement.

Section 8 is a critical aspect of the RESPA regulation that real estate agents should be well versed in. Section 8 of RESPA prohibits kickbacks or unearned fees in exchange for settlement services on mortgages covered by RESPA. Specifically, RESPA prohibits a settlement service provider from giving or receiving anything of value in return for business. Sections 8 protects the consumer from paying more in settlement charges which are a result of a fee being paid without any work performed for their specific settlement.

There are four required elements to be considered a violation of Section 8.

The first requirement is that the loan must be covered under RESPA. This was reviewed earlier in the chapter, but as a quick recap, this means it must be a federally related mortgage.

The second requirement is that there must be a referral of business related to a settlement service with an understanding of the relationship or agreement. You should note this does not have to be verbal or written consent but can be construed from patterns and actions.

The third requirement is that there must be a payment made or a receipt of something of value. It is important to remember that there are many different items that can be considered something of value. Here are some examples of “things of value”: discounts, participation in money making program, services at special rates, trips, and reduction of debt. It is important to remember that things of values are not necessarily money but encompass a full range of items that can lead to a RESPA violation.

The last component for a violation to occur is that the thing of value must be in exchange for a settlement related service.

Let's look at a real world examples were a RESPA violation can occur.

As a real estate agent, let's say your broker approached you and offered you a higher split on a transaction that closes at a particular settlement company. If the transaction in question, involves a federally related loan then this is a clear violation of RESPA.

Finally, RESPA covers Affiliated Business Arrangement (AFBA). This occurs when a real estate agent or broker has a financial interest in a settlement provider entity. AFBAs are allowed under RESPA as long as specific guidelines are followed. There are specific disclosures that need to be provided to the client to sign when these relationships exist.

It is important to relay to your client that they are under no obligation to use that service provider but should be aware of the financial relationship if they choose to do so.

As a real estate agent, it is important to know that there are harsh punishments for parties who violate RESPA especially Section 8. We reviewed penalties lenders face when violating the disclosure rules in the TILA chapter we will briefly recap here but focus on penalties under section 8 of RESPA.

People who violate section 8 are subject to both criminal and civil penalties. A consumer only has one year to file a claim that a kickback violation occurred; however, the government has up to three years to bring a claim. Penalties can be up to a $10,000 fine and include up to one year in prison. Also, the violator will have to pay up to 3 times of the settlement charge involved in the violation.

As discussed in the TILA lesson, lenders can face between $2,500 and $1,000,000 per day, per violation, depending on the nature of the violation.

As a real estate agent, it is critical that you pay close attention to anything that a title company provides to you, even if it seems like an innocent gesture. Remember a violation does not have to be a written agreement but can be construed through a pattern of activity.

For the last section of the chapter, we will review the most important aspects of RESPA and how it relates to your day to day real estate activities.

As discussed in the TILA chapter, it is imperative that you follow up to make sure the CD is provided to your client by the deadline. If it does not happen, closing will be delayed, and your clients will have breached their obligations under the contract.

Another critical concept of RESPA, to take away, is to be aware of your relationships with entities providing settlement services to your clients. Even if you are not engaging in an intentional act that violates RESPA, it is just important that you do not engage in activities with settlement services providers that could look improper.

Finally, if your brokerage has any affiliated business arrangement, it is crucial you make sure your clients are provided the appropriate disclosures, and the disclosures are signed by all parties in the transaction.

Key Terms

Real Estate Settlement Procedures Act (RESPA)

A federal law requiring the disclosure to borrowers of settlement (closing) procedures and costs by means of a pamphlet and forms prescribed by the United States Department of Housing and Urban Development.

COPYRIGHTED CONTENT:

This content is owned by Real Estate U Online LLC. Commercial reproduction, distribution or transmission of any part or parts of this content or any information contained therein by any means whatsoever without the prior written permission of the Real Estate U Online LLC is not permitted.

RealEstateU® is a registered trademark owned exclusively by Real Estate U Online LLC in the United States and other jurisdictions.