Chapter 4 - Home Ownership

Learning Objectives

At the completion of this chapter, students will be able to do the following:

1) Explain the pros and cons of owning a home.

2) List at least two forms of homeowners insurance.

4.1 Types of Housing Accommodations

Transcript

As a real estate agent, you'll encounter people looking for a variety of housing accommodation types from single-family homes to condominiums and time-shares to mixed-use commercial properties. While 88% of first time home buyers work with a real estate professional today, that wasn't always the case.

Did you know that Sears and Roebuck, sold approximately 100,000 ready-to-build house kits in the early 1900's? Often for less than $1,500, people could order a single or multi-story design, from a catalog, with as little as $1 down to cover the cost of mill work. The kits contained everything needed to erect a house in less than 400 hours – that means precut lumber, window glass, doors, paint, nails, varnish, carved staircases, flooring and even the hammer needed to build the wraparound porch (also included)! The kits arrived via railway and buyers typically towed the crates to their lot with a mule team, horses and a buckboard or one of the new Model T trucks – if you were fortunate enough to be able to afford the $600 price tag after buying a house kit.

Of course, things are more complicated today, with zoning laws, lot restrictions and a complex web of tax codes. That is why people hoping to invest in real estate need a well-informed agent to help them navigate the process. So, let's discuss a few of the different types of housing accommodations on the market now, starting with the single-family home.

The single-family home is probably the most common property sold and bought on the market today. The percentage of single-family dwellings compared to all residential units fluctuates, but has consistently ranged between 60% and 70% since the 1940's, according to the 2011 US Census. Like the Sears and Roebuck homes mentioned above, a single-family home is a residence that isn't connected to other buildings. There is space on all sides, although the surrounding area may be limited only to the required easement to comply with building codes or encompass acres and acres of green space, if built in a rural area.

Unlike stand-alone, detached dwellings, multi-family buildings, have two or more individual houses connected by at least one adjoining wall, floor or ceiling. There are many variations that include: duplexes, quads, Victorian homes converted to individual living quarters with cooking and bathroom facilities, and both low-rise and high-rise apartment buildings. Although there are some privately owned apartment homes in larger cities like New York City, Seattle and Los Angeles, most multi-family home units are investment rental properties.

Classifying apartment buildings is a bit tricky because architects use terms like low-rise, mid-rise and high-rise differently. Some identify all buildings over nine stories tall as high-rise, while others say that buildings with less than three floors are low-rise, four to twelve story buildings are mid-rise and anything over 13 floors is a high-rise property. The city or region could also influence how local authorities classify each building.

It is best to follow the International Building Code (IBC) guidelines which base classification on the height of occupied space. The IBC says that any structure with occupied living space higher than 75 feet above “the lowest level of fire department vehicle access” is considered a high-rise. Most modern high-rise apartment buildings have elevators, but also have stairs to accommodate safe, rapid egress during an emergency.

In a condominium, each unit is owned individually. The units may be owner occupied, or used primarily for rentals, or vacation homes. In a condominium building, all common areas, such as walkways, meeting rooms, swimming pools and other shared spaces in a condominium arrangement are jointly owned by all condominium owners. And, homeowners typically pay monthly or annual dues to cover the maintenance, repair and insurance expenses established by covenants and by-laws approved and voted on by a select board and owners.

Another housing type you may come across as a licensed real estate agent is the cooperative, or co-op. Unlike condominiums, where each dwelling is privately owned, cooperatives are apartment buildings owned by a corporation that sells shares which entitle shareholders to exclusive, private use of a residential dwelling, or housing unit. Here is something to remember when recommending this type of property to potential buyers. Co-ops aren't considered “real property,” since buyers only purchase the right to use the dwelling. Occupants are basically just renters, so some of the tax benefits of home ownership aren't available to co-op residents, although they may be able to take some expensive deductions, like the allowance for home office and certain qualified repairs. All shareholders must pay a common area maintenance charge, typically calculated based on the square footage of the unit they occupy.

Let's step away from traditional private housing types to a commercial example, the planned unit development (PUD) model. Even if you've never heard the term before, you have almost certainly seen a PUD. Commercial land developers may want to create a mixed-use area that doesn't fix any of the existing zoning and density guidelines by building individual homes, multi-family housing, retail space and recreational facilities such as hiking trails or a baseball diamond. To accomplish this, the developer must submit detailed plans to the appropriate agencies to get approval. Approval is often based on how well the developer incorporates business and residential uses, whether the builders have considered the economic and environmental impact for residents and the extended community beyond the borders of the PUD.

Speaking of mixed-use developments, there is another housing type that doesn't involve building an entire community from the ground up. Although many large cities have seen an uptick in multi-use properties in recent years, the practice of having retail space on the ground floor and apartments on upper floors isn't new. Remember those ready-to-build homes we mentioned earlier? At the same time those houses were popping up in many communities, there were boarding houses that offered private rooms for rent above a restaurant open to the public. Today, you'll find high-end apartment buildings with organic grocery stores, dry cleaners, bakeries and internet cafes on the street level while modern, well apportioned apartments occupy the upper floors.

Today, consumers are looking for houses to buy in neighborhoods with high walkability scores and access to everything from food to entertainment, so mixed-use properties allow property owners to maximize earning potential on every square inch of the investment. In many cases it is a virtual trifecta – cities increase tax revenue, investor-owners can charge higher rents and tenants enjoy the convenience of picking up their dinner or dry cleaning on the way to the elevator that will take them upstairs to their apartment.

Mobile homes account for roughly 8% of all housing units in the United States, but where those homeowners live is telling. Only 6% of metropolitan units are classified as mobile homes, while rural, or non-metro areas have three times as many mobile homes, according to Population Reference Bureau. There are positives and negatives to owning a mobile home – for one thing, as the name implies, they are easy to move. They typically cost less than other new home types, although buyers may pay a higher mortgage interest rate if they need to finance. For people with limited funds, trailers may be the only real property they can afford. There are some “hidden” expenses associated with this type of housing. For example, only about half of mobile homeowners own the land where their house is parked. This means on top of the mortgage, buyers have to pay a monthly rent for the space, or invest more money to purchase land, which increases the overall cost of ownership.

Manufactured homes today come in single- and two-story models, and a variety of lengths and widths. And, although all are portable, many larger manufactured homes assembled on site are never moved once they are anchored down. Some manufactured homes are also multi-family homes, built similar to a duplex where they are two distinct dwellings joined by a common wall.

A cousin of the mobile home is the modular home, or prefabricated home. In some ways, modular homes are like the kits Sears sold to twentieth-century home buyers, although the homeowner doesn't have to assemble the house. Modular homes are built in movable sections called modules in a factory according to a buyer's specifications or a particular floor plan designed by the company offering the home for sale. Where a new construction home typically takes many weeks to erect, once the modules arrive at the building site, professional builders can have the house ready for occupancy in about a week, baring extreme weather events. Unlike mobile (manufactured) homes, prefab houses are assembled on a permanent foundation, so moving is not usually an option.

We have two more types of housing accommodation to cover in this lesson: retirement communities and time-share. This first is more commonly seen as a primary residence option and the second as either an investment or strictly a vacation home. We'll start with time-shares.

Earlier we discussed cooperatives where buyers invest in shares of a corporation for the privilege of gaining exclusive use of an apartment home. Like co-op dwellers, time-share investors never fully own a piece of real property. They gain access to the land, a dwelling or other real property.

Time shares fall into three main categories:

-The first is a Fee Simple contract which results in deeded interest, with a title in perpetuity.

-The next is a basic Right-to-Use (RTU) arrangement where you have rights to exclusive use that expire on a given date and revert to the actual owner – this is usually ten to twenty years.

-The final category is called “leasehold”. Like the Fee Simple the property is deeded. However, it also has an expiration date, like the RTU. Some Leasehold contracts offer a first right to renew clause.

Regardless of the category, time-share investors are limited to the amount of time they can use the property. For example, you may have exclusive access two weeks out of the year, or for a specific calendar month, depending on how many other “owners” have an interest in the property.

And, now, the last housing type we will cover is retirement communities. Although there are many different types of retirement communities all have a few similarities. Most have a minimum age requirement, usually 55 or older. Some retirement developments have an 80-20 rule, where 80% of the properties are owned by people over 55 and the other 20% are owned or leased by younger families or singles.

Services that are available in retirement communities may include lawn care, housekeeping, laundry, and access to a handyman to help replace light bulbs or hang pictures. There is usually a monthly fee beyond the mortgage payments to cover maintenance of common areas and amenities. Some communities have an on-site recreation director who schedules shopping trips, arranges group discounts for local plays and movies, and invites instructors to teach classes on a variety of topics from painting and sculpting to finance and computer literacy.

It is important to consider why clients want to move to a retirement community before recommending specific properties. Some want the social engagement and security of living in a tight-knit community without having to commit to the daily structure of an assisted living property. Others aren't currently facing medical challenges, but they are looking for a property that can offer them different services as they age. One community in the Dallas, Texas area offers home buyers a chance to buy a private home initially, and trade up to a residence in the assisted living area on campus, if they develop medical challenges; then transition to a retirement dorm with 24 hour care when the time comes.

Homeowner preferences vary widely among different demographics and diverse geographic regions. Rural areas have a higher percentage of ownership than urban and metropolitan areas, approximately 75% to 68% respectively. People in a lower income bracket tend to buy more mobile homes, and baby boomers aging into retirement age may prefer a well-equipped retirement community close to physicians, hospitals and grocery stores than the mixed-use property in a thriving downtown neighborhood in the city. This lesson should give you the information you need to help your clients find a home in an area that fits their needs and their budget.

Key Terms

Condominium

An estate in real property wherein there is an undivided interest in common in a portion of real property coupled with a separate interest in space called a unit, the boundaries of which are described on a recorded final map, parcel map, or condominium plan.

Cooperative

An apartment building, owned by a corporation and in which tenancy in an apartment unit is obtained by purchase of shares of stock of the corporation and where the owner of such shares is entitled to occupy a specific apartment in the building

Mobile Home

A structure transportable in one or more sections, designed and equipped to contain not more than two dwelling units to be used with or without a foundation system.

Modular

A system for the construction of dwellings and other improvements to real property through the on-site assembly of component parts (modules) that have been mass produced away from the building site.

Time-Share

A form of subdivision of real property into rights to the recurrent, exclusive use or occupancy of a lot, parcel, unit, or segment of real property, on an annual or some other periodic basis, for a specified period of time.

4.2 Factors Affecting Home Ownership

Transcript

There are many factors affect home ownership rates in the United States, including age, ethnicity, location and the overall economy. Personal finances, poor credit and limited cash on hand also impact buying decisions. A 2015 study showed that while seniors want to stay in their homes, new renters across all age groups will outnumber new home buyers in 2030. Millennials may see the largest gap between those who want to buy a home and those who can afford it. Some 62% of today's Millennials will still be renting, or signing the first lease, ten years from now. And, the ownership rate for 35- to 44-year olds is projected to decline 12.2 percent in the coming decade, compared to 1990 rates.

In this lesson, we'll explore a few of the advantages of renting versus owning, and discuss financing options for those who are ready to embrace the benefits of buying their first home.

Let's start with a discussion about why people rent.

In 2014, the Federal Reserve conducted a survey of almost 5900 participants to learn more about housing preferences and household living arrangements. More than 4 out of 5 respondents (81%) said if they could afford to buy their own home, they would. Approximately 50% of survey participants stated they didn't have enough money for a down payment. Slightly less than one-third (31%) said financial or credit issues prevented them from qualifying for a mortgage.

While people who earn less than $40,000 annually cite finance and credit issues as the main barriers to owning their own homes, people earning more than $100,000 often cite personal preferences as the driving factor behind their decisions to rent. For example, the top earners were 20 percent more likely to rent for convenience compared to people earning $40,000, or less. And, 31 percent of people in the highest wage bracket thought it was cheaper to rent than invest in a homestead. People in all income brackets may rent because they are planning to relocate soon, buy a home in the future or just prefer to rent rather than commit to a long-term contract.

Renting usually comes with perks like not having to maintain a lawn, lower utility bills and sometimes free internet and cable. You can also pack up and move whenever you want, without the hassle of trying to sell your home or becoming an unwilling landlord who has to assume those mundane tasks like mowing the yard and fixing the leaking roof.

So, what about home ownership?

While roughly 10 percent of the adult population doesn't plan to ever buy a house, most of us dream of having our own place. Remember that 81percent of respondents who would buy a house of their own if they could? Buying into the American Dream has its own set of benefits that goes beyond pride of ownership. For one thing, there are some tax benefits. Buying a house or condo means owners can deduct points and interest paid on mortgage, home improvement loans and home equity lines of credit (HELOC) associated with repairs and renovation projects. You can also tap into your IRA penalty free to buy a home, as long as you don't draw out more than $10,000. Another financial benefit is long-term appreciation as your home value grows.

Other factors motivate people to leave rental property in search of a private dwelling. Just slightly less than half (44 percent) of the respondents in the Fed survey who preferred to own rather than rent, said, they wanted to build equity rather than throw away hard earned cash on rent. Others said they like knowing how much their payments were going to be from month-to-month and year over year. Having the flexibility to customize a home to personal preferences and style, along with having fewer rules to follow, also made the list of reasons people preferred to own. And, some people just don't like to move. Once they find a spot they like, they plant themselves and dig in.

Here's an interesting item that came to light in the Fed's survey. On average, 28% of all participants believe it is cheaper to rent than to own. This tells us two things. Perception influences buying decisions, and education is important to help first time buyers understand financing options available.

So, let's discuss a few mortgage plans for current renters who may be wondering if they can afford to buy a home.

Few individuals will ever save enough money to plunk down a stack of cash to buy a home. People, who have contributed faithfully to a 401K, saving for retirement, could borrow against the fund to cover a down payment or pay down points. IRS rules allow homeowners to withdraw up to half of their nest egg in the form of a self-loan, to purchase a home. The withdrawal may not exceed $50,000. There are no penalties or taxes to pay as long as you pay back the loan, with interest, on time. Theoretically, you aren't really losing anything. Right?... Not exactly!

There are some very important things to consider. Depending on the 401K plan you have through your employer, you may not be allowed to continue to make deposits into the account every payday until the loan is satisfied. And, if your employer matches your contributions, you will lose those extra funds. Plus, if you quit or get fired before the loan is settled, you only have a two-month window to pay off your loan. What happens if you can't pay it back on time? You'll be hit with a 10 percent tax bill on the balance. Unless you are positive, you can keep your job and afford to pay back the full amount of the loan, don't do it!

Fortunately, you don't have to dip into your retirement nest egg. There are plenty of mortgage options offering a low down payment and reasonable interest rates, and some programs are specifically tailored for people with limited credit.

Before we look at a four mortgage options, let's talk interest rates.

Interest rates directly impact a home buyer's ability to make monthly payments, but they aren't the be all and end all of getting a good mortgage. You must consider the interest rate, the length of the loan and down payment requirements to ascertain whether a mortgage is truly affordable.

Here is an example to show you why all three matter.

Let's say you're buying a $150,000 home and plan to pay taxes and insurance separately, which is not likely, but this is just an example. If you are approved for an FHA loan with a 3.5 percent down payment, you would only need to come up with $5,250, before origination fees and closing costs. With an interest rate of 4.25 percent on a thirty-year fixed mortgage, your monthly payment would be $712. An interest rate of 5.75 percent would push that payment up to $845 per month.

Shortening the term to twenty years, while keeping a 4.25 percent interest rate means you'd be paying $896, but you would shave ten years off the mortgage, saving $41,280 in the process, assuming you kept the home for the full term of the contract. Bumping the down payment to 10 percent, or $15,000, on a 30 year loan at 4.25 percent would drop the payments $48 a month. See what we mean? It is critical to carefully consider how much you can afford and then partner with a lender to find a loan package that works best for you.

Now let's look at those mortgage loan types.

The Federal Housing Administration (FHA) guarantees loans for people with exceptional credit and people with very low credit scores, no credit history and even past problems with bankruptcies. The 3.5 percent minimum down payment is a great solution for people who have a strong debt-to-income (DTI) ratio, but may not have a bundle of cash for upfront costs. People with a credit score below 600 may have to pony up a down payment closer to 10 percent to secure the loan.

Veteran Affairs finances up to 100 percent of the loan value, at competitive interest rates, for active duty, reservists, retired military personnel and qualified dependents. Interest rates are low, and you don't have to pay PMI or upfront mortgage insurance payments. Plus, seller contributions are allowed, capped at 4 percent.

Here's a great mortgage option for home buyers who need to use non-borrower income and nontraditional credit sources to qualify. The Fannie Mae “Home Ready” mortgage program has flexible underwriting policies, up to 97 percent financing and even a cancellable mortgage insurance option to lower payments.

We saved the best for last, a mortgage that only requires a $100 – yes, you read that right – $100 down payment. It's called the “HUD Good Neighbor Next Door” program. Basically, you get to buy a designated HUD property at 50 percent of the appraised value. If you qualify for any FHA lending program, you only pay $100 down. You must live in the house for 36 months, or you have to pay back the 50 percent discount, but this is a great way to buy a starter home, or even a future investment property.

As you can see, there are many factors to consider when buying a home. Just because a client can qualify for a high interest loan with a large down payment doesn't mean he should. As a real estate professional, you should point your clients toward mortgage solutions that are fiscally responsible. But again please do not give any mortgage advice and leave that to the mortgage professionals.

Key Terms

4.3 Tax and Investment Aspects of Ownership

Transcript

Home ownership comes with plenty of challenges, like taking responsibility for the overflowing toilet at two o'clock in the morning and keeping your trees well pruned so a storm doesn't result in damage from a limb crashing through your neighbor's roof. There are plenty of advantages, too. Overtime, well maintained real estate property usually increases in value, giving owners a healthy return on investment you can use to buy a larger home or borrow against for other needs – or wants.

Understanding the tax and investment aspects of home ownership will position buyers to capture all the benefits of home ownership available immediately and in the future.

As a real estate professional, you can guide first-time and experienced buyers toward wise investments by staying informed about changes in local, state and federal tax codes, new building regulations, and neighborhood amenities for every lifestyle.

In this lesson, we'll discuss some of the tax and investment aspects of home ownership every real estate agent needs to understand to become an advocate for both sellers and buyers.

Taxes are always on the minds of first time buyers, so let's begin there.

The tax code is like a lazy river, meandering downstream. On the surface, it looks like nothing really changes as the water moves along, but beneath the surface there are hidden hazards and treasures. Staying up-to-date on federal tax code changes ensures you never miss one of those beautiful treasures or trip over a hazard by claiming deductions that you aren't eligible for based on the type or use of your real estate.

Before we get into some examples of how homeowners can leverage tax deductions to reduce the costs of home ownership, let's look at a few important finance terms.

First time home buyers often don't recognize, or understand, industry jargon. Many are embarrassed to ask questions. Four words that usually show up in every initial mortgage conversation are: mortgage interest, discount points, loan origination fees and private mortgage insurance (PMI). These terms may come up when talking to clients about pre-qualifying and the true cost of financing, before making any offers.

You probably already know that mortgage interest is the fee lenders charge to offer loans secured by either a primary or secondary home, used primarily for personal use. This fee is structured much like a revolving loan. Interest is calculated every month, or after every scheduled payment, on the remaining principle over the term of the mortgage.

Loan origination fees, are a bit more complex. Lenders charge administrative fees for reviewing applications, verifying credit worthiness and processing paperwork prior to issuing a loan. The fee is based on the price of the real estate and typically equals 1% of the loan value. The origination fees cover the lender’s costs for funding the loan.

One term you will constantly come upon is “points”. What you have to remember is that one point is equal to one percent. So if you hear someone saying 3 points they mean three percent.

You will also hear the term “buydown” which is commonly used when buyers are looking to get discounted rates at least for the first years of their mortgage.

Discount points allow buyers to prepay interest in exchange for a reduced mortgage interest rate. You may opt to pay zero points, or go as high as 4 points, in some circumstances. As a rule of thumb, you can figure each point will cost about 1% of the loan amount.

So, a one point buydown on a $90,000 mortgage equals $900 which is in essence one percent of the mortgage amount. Two points equals $1800, three points equals $2700, on so on.

There are some conditions that govern the buy down. For example, homeowners must utilize the cash accounting method when preparing tax returns to claim deductions– most people do anyway. And, the size of the buy down must be customary for the neighborhood.

A word of caution before we move on to the last term on our list!

There are many types of points discussed during the mortgage application and funding stages. While discount points and loan origination fees are tax deductible, origination points are not. Some lenders tack on hidden fees under the label of origination points. If you ask for an itemize point statement, you may see charges for property inspections, a title search, lawyer fees, notary public services and other add-ons, all of which are not tax deductible items.

Just because you can't take an immediate deduction for origination points, it doesn't mean you should ignore them. Clients considering investing in rental property should know that discount points and origination points qualify as depreciation expenses, and can be amortized, along with certain other expenses of buying, building or improving real estate holdings over the life of the real property.

Private mortgage insurance, often referred to simply as PMI, is protection for the lender, if a buyer fails to make payments. This insurance premium is typically included in the total monthly mortgage payment; however a one-time payment may be made at closing. Some lenders allow a large PMI down payment and smaller monthly installments as part of the regular mortgage schedule. PMI may be dropped after the balance falls below a predetermined amount, because this type of coverage is usually only required on conventional loans with a down payment less than 20%, or if the buyer wants to refinance a home with less than 20% equity built up.

OK. Now, that you know some common mortgage terms, let's talk about the federal tax benefits of owning real estate.

Homeowners who file a 1040 and itemize deductions on Schedule A, can usually deduct mortgage interest paid, discount points, some real estate taxes, origination fees, and PMI associated with first mortgages, second mortgages, equity loans and lines of credit secured by your primary residence or a second home.

Let's go over a few of the most common deduction scenarios.

Homeowners may deduct mortgage interest paid on a debt secured by a primary or secondary home, wholly or partially owned. That simply means you can own 100% of the real estate, or share ownership with one or more people. The Internal Revenue Service considers any real property that has sleeping, cooking and bathroom facilities a qualified home. So, along with accessing tax benefits for traditional homes like condos, trailer houses and single-family residences, if you live in a mortgaged house boat, recreational vehicle or other structure that fits the description above, you can deduct interest paid, as long as you use the property solely for your own personal use, with a few exceptions.

Commercial and rental properties fall under different umbrellas in the tax code; will briefly talk about those items later.

Here are three examples that demonstrate how ownership percentages and use rules affect deduction allowances.

In the first scenarios, let's say Jeffry fully owns his residence, and occupies that home all year long. Each year, his lender provides a 1098 Form detailing the total interest, discount points and PMI paid in the previous year. If the 1098 Form shows Jeffry paid $2000, and that amount is less than the value of his home, he can usually deduct the full amount.

But, what if Jeffry shares an ownership interest? For this example, let's say Jeffry shares ownership equitably with four other people. Based on the details in the previous example where the annual 1098 statement reflects $2000 in payments, Jeffry can only deduct $400, which is the total divided equally among the five owners.

It is possible to structure ownership with different ownership percentages, based on the original purchase contract, or the amount each buyer invests in the purchase and/or property improvements. For example, Jeffry could own 60% and each of the other four owners own a 10% share.

Now imagine that Jeffry owns 100% interests in his home and wants to rent out a couple of rooms to earn some extra money or defray costs of ownership. As long as he does not lease any part of his home for purposes other than residential living, and the leased space is not self-contained, meaning it could not be construed as a complete home unit with separate cooking facilities, bathroom and sleeping quarters, Jeffry can treat the rented space as part of his personal home for tax purposes, and claim the full tax benefits based on 1098 figures. One caveat, he is not allowed to lease the same space or different parts of his house to more than two renters at any time during the tax year.

There are dozens of other special rules and exceptions within the tax code that directly and indirectly benefit homeowners. IRS Publications 936, 17, 550 and 530 provide general information worth reading, if you find yourself wanting to become more proficient in ways that could help homeowners. That is not to say that you should give any accounting advice though. Leave that to the trained professionals.

Before we leave tax benefits, turn your attention to real estate taxes for a few minutes.

Real estate taxes are a tax deductible item. Real estate tax rates vary widely by state, town and even neighborhoods and communities within cities. Each appraisal district offers a diverse set of discounts and exemptions including adjustments for people over 65, Disabled Veterans and Non-Veteran Disabled Persons. Fortunately, homeowners can contest the assessed value and participate in open discussions during the proposed assessment phase. All tax assessments are based on Market Value, and differ according to the benefiting entity.

As an example, a combined tax statement for a rural town in Texas assessed a county tax at 0.0457330, a city tax at 0.0735200, a local independent school district at 1.3080400, the junior college at 0.366350 and the regional water district at a rate of 0.008026 for a total annual tax of $494.60 on a property with a market value of $17,200.

You may not deduct special fees that only apply to individual homeowners within a tax district, such as late fees, interest on unpaid tax bills and water connection fees or financed meter upgrades. All allowable taxes must meet a “conformity” standard, which means that all real estate owners in a common district or community are billed for the same entities at the same rate.

We have focused heavily on tax deductions and first-time homeowners so far in this lesson; however as you work to grow and cultivate your farm, you may work with commercial buyers, people looking to sell their homes, and investors.

For those of you who aren't familiar with the phrase “cultivate your farm,” successful real estate professionals sometimes pick a particular subdivision or section with a county and proactively “plant seeds,” they hope will help them generate future sales. They take the time to get to know the residents, find out what they like and don't like about their homes, and maintain contact with these people hoping when it comes time to buy or sell, they will call them first. Part of farming an area means you have the knowledge and resources to serve the community.

So, let's talk about capital gains for a few minutes, and shift our focus to sellers.

Capital gain is the effective profit or loss realized based on the difference between the sale price of a piece of real estate and the cost of acquiring the asset. We mentioned earlier that orientation points aren't deductible expenses. However when it comes time to sell a property, the net profit reflects adjustments for transaction fees, such a real estate agent commissions, attorney's fees and sales tax, among other expenses.

There are short-term capital gains and long-term capital gains. Real estate investments purchased and sold within a one year period have higher tax rates than assets held longer than twelve months. The current tax rate is based on marital status, tax brackets, and how the property was acquired.

The sale of a property does not push a tax payer into another tax bracket.

For almost two decades, the short-term rate has remained the same as “ordinary” income. However, long-term capital gains have fluctuated significantly, with a maximum effective tax rate as high as 40% in the mid 1970s. The effective tax rate for long-term holdings ranges from zero to 20% for most homeowners.

However, the maximum rate currently includes an additional 3.8% added to the capital gains bracket for the top earners in the United States, making the highest tax rate 23.8%. Top earners are classified as a single taxpayer that earns more than $200,000 per year, or a married couple filing jointly, who earns more than $250,000 per year.

But, what about accidental homeowners?

An accidental homeowner is someone who inherits a piece of real estate and decides to make the property their primary residence. Fortunately, immediately after they legally acquire the property, the cost is bumped up to fair market value, which means they do not have to pay capital gains tax on appreciation realized during the previous tenancy, or face a huge tax burden when the property value is worth much higher than the original cost.

In some instances, homeowners may be required to recapture depreciation when a piece of real estate is disposed of; this is primarily called into play when the sale price exceeds the cost.

Which brings us to a discussion about depreciation.

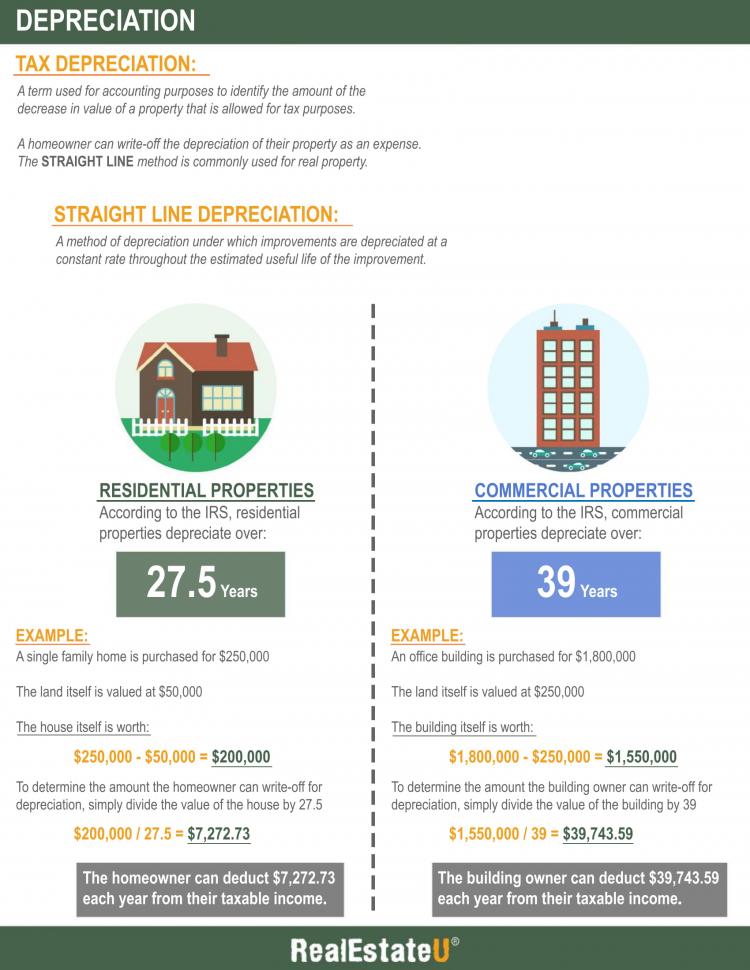

Tax depreciation is a gradual reduction in the value of your property that allows you to recover part of your cost or other basis in the form of a tax adjustment. You cannot depreciate land; however you can depreciate structures and improvements, including rental property. The most common depreciation method is known as the straight-line method, where you divide the value of your house by 27.5 to get the allowable annual depreciation deduction. So, assuming you have a rental home valued at $150,000, your annual deduction for residential property would be $5,454.54 which is the result of dividing $150,000 by 27.5.

Non-residential, commercial real estate is assumed to have a life-span of either 39 or 40 years, depending on whether you use the General Depreciation System (GDS) or the Alternative Depreciation System (ADS) to calculate annual loss in value based on wear and tear, damage and obsolescence. You calculate straight-line depreciation by dividing the difference in the salvage value and the purchase price, or cost to build the structures, by either 39 or 40. Land is not depreciated.

For now, let's leave ways to save money and move on to ways to make money and really capture the positive benefits of real estate investment activities.

From an investment perspective, taxes are not the only thing to consider when buying and selling real estate, maybe not even the most important consideration. A well-informed real estate agent understands the importance of building equity and exploiting appreciation as the market changes.

For example, single-family home values usually change based on market statistics (also called stats) and comparisons (also called comps). As transactions in a neighborhood generate higher sale prices based on normal inflation, as a response to the economy, or fluctuation in demand, property values increase for similar homes.

In multifamily environments, some investors proactively force the appraisal value to rise, by adding upgrades and amenity packages that boost revenue potential, then gradually increase base rents, which makes their properties more attractive to potential buyers.

Forcing appreciation doesn't work as well for personal homes as it does for apartments and planned communities. Over renovating a home in a modest neighborhood won't necessarily bring higher returns unless other home owners follow suit. Most home buyers who invest in a personal residence are more interested in growing their equity faster, to allow them to access available money for renovations or as a down payment on another home.

Buying low is the best way to grow an equity nest egg. Here's why. On a typical 30-year, fixed-rate mortgage it takes approximately 22 years to pay down half of the original loan principle. The first few years, the majority of each monthly payment goes to pay down the interest on the loan. Over the full term of the loan, a buyer with a $165,000 mortgage financed at 4.5% will pay a staggering $300,970. That's $135,970 in interest alone. More than 45% of total payments cover only interest.

It may not be a good idea to show potential buyers how much they will ultimately pay for a home if they plan to make payments that long, unless you plan to show them how they can save money by doubling up on their payments, or paying a little extra each month designated for reducing the principle – that shows them they have control over how quickly their equity builds up.

We've covered a lot in this lesson. The last section covers the Starker Exchanges also know as Like-kind or 1031 Exchanges.

If waiting impatiently for equity to grow, or trying to force faster appreciation, doesn't work for your real estate clients, you may introduce them to Exchanges as an investment tool.

Are you wondering what a 1031 Exchange looks like?

Here's a brief overview. The IRS code allows two property owners to literally trade like-kind property without paying capital gains taxes.

There are a few requirements that must be met for property owners to defer, or avoid tax liability. For one thing, these exchanges only apply to business and investment properties. You can't trade a private residence for another private residence. And, you can't exchange a piece of rental property for a moving van or construction crane, even if they are valued at the same price.

You could trade a four unit apartment home for a single-family rental, as long as the exchange results in the net market value and the property equity purchased is the same or greater than the property you're selling. You can also apply reasonable acquisition expenses to the cost of the new property.

Here's an example of what it would look like.

Say you have a multifamily apartment building valued at $1.5 million and a mortgage of $400,000. And you want to work an exchange to avoid paying any capital gains tax. You could purchase a single-family home, or several properties that have a combined market value of at least $1.5 million, and you would need to carry over a minimum of $400,000 in mortgage liability.

It isn't as easy as simply transferring the deeds, although that is allowed, because finding another business property owner with a similar valued property, as yours, who is looking for a quick swap would be like finding a specific grain of sand in the middle of the Sahara Desert. Usually an investor first sells a property, and then reinvests the proceeds in a property with a similar cash value, and functionality – equipment for equipment, structures for structures, etc.

Often investors involve a third party to act as a middle man, or open an LLC so their business can hold the assets in escrow until a suitable swap can be found. There are other options, but these are the most popular.

This strategy works very well for investors who are looking to change the type of business real estate they own. For example, a property owner may want to trade an assisting living property for seniors for a high rise that caters to college students. Or, a management company may be looking to expand single-family homes and move away from multifamily complexes. Sometimes companies want to invest in another area, so they look to real estate in other towns or states to complete a like-kind exchange.

One last thing to consider with 1031 Exchange transactions; buyers have several timing limitations. For example, the property seller only has 45 days to identify up to three potential properties that would qualify as like-kind properties. It is possible to swap four or more properties, providing the combined total does not add up to more than 200% of the real estate being sold. And, all transactions must be completed within six months, or 180 calendar days, of the first closing, unless the property owner files for a tax extension.

We've only touched on the 1031 Tax-Deferred Exchange options. It is quite entertaining to read through examples of how investors put their creative spirit to work negotiating deals. It is a high-stakes game for some people to see if they can find similar properties in areas they want and get all their I's dotted and T's crossed in time to avoid paying capital gains taxes.

You have a responsibility as a real estate agent or broker to learn as much as you can about helping your clients make wise decisions as they buy and sell in the market place. Armed with the topics covered in this session, you can better help your customers understand the tax and investment aspects of home ownership.

Key Terms

4.3a Depreciation Infographic

Please spend a few minutes reviewing the Infographic below.

4.4 Homeowner's Insurance

Transcript

The first insurance policies in the United States were issued around the middle of the twentieth century. Property insurance covers loss associated with a variety of damage and typically protects the homeowner against natural events, like forest fires, hail storms and hurricanes, as well as man-made causes, such as vandalism.

The typical American does not have the funds or available credit to replace the home and all of the things inside if a fire destroys everything. And, most mortgage companies require a minimum amount of insurance to protect their investment in your property. Protecting your assets, whether it is the dwelling and structures or the contents, is critical, unless you have financial assets available that could be used to replace your home after a significant loss.

Homeowners' insurance plans may cover the buildings, the contents, and/or liability in case someone is killed or injured on your property. Depending on the type of home you have, its age and where you live, you may only need one type of coverage, or you may need all three.

Here are a few of the most common insurance policies homeowners can consider.

Homeowners’ O (HO-0, Dwelling & Fire) is a limited perils policy that does not provide personal property, medical or liability coverage. If someone is hurt on your property, they may still sue you, but the insurance company is not obligated to defend you or help you reach a settlement.

Each insurance carrier has unique terms and conditions; however, most provide optional coverage for the damage specifically caused by the following events:

- Smoke infiltration related to natural causes and/or vandalism. By the way, vandalism, or malicious mischief are covered, even if arson isn't involved.

- Fire damage caused by lightning and accidents such as grease fires in the kitchen

- Riots or other civil disobedience activities

- Severe weather events, such as hail or driving winds

- Explosions

- Aircraft

- Volcanoes

Most policies have a limited reimbursement for damage caused by vehicles, providing you were not driving the vehicle or otherwise responsible for the damage. The thing to remember is that only listed perils are covered. So, if an old tree on your property falls and damages the roof of your house, you would only be covered if you can prove one of the listed perils, such as wind or lightning, was the stimulus.

Homeowners' 1 (HO-1, Basic) provides the same basic coverage for the ten perils listed above, plus glass breakage. This plan is not very popular and many agents don't recommend the coverage because it is too narrow. Contents may be added when the policy is purchased, providing each item is listed or valued at the time the policy is issued.

Homeowners' 2 (HO-2, Broad Form) policies are another example of named peril plans, only you get a little more coverage with the HO-2. All 11 of perils covered under an HO-1 plus six more are covered under an HO-2 policy. Along with protection against loss caused by fire and smoke, you have peace of mind that a heavy snowfall or ice that damages your roof or a faulty appliance in your home won't cost you a fortune to repair.

Homeowners' 3 (HO-3, Special Form) is one of the most common plans because everything is covered unless specifically excluded. HO-3 coverage is the minimum plan many mortgage lenders require to issue a loan. However, only structures and dwellings are covered. Personal property coverage only applies to perils listed. Some restrictions may apply, but general real property is covered at full replacement value, with no adjustment for depreciation.

Homeowners' 4 (HO-4, Tenant Coverage) While HO-4 is not for homeowners, real estate agents should recognize the term. HO-4 is similar to HO-2 and HO-3 in that these policies cover content perils typically seen in those two types of homeowner policies.

Homeowners' 5 (HO-5, Comprehensive) Some agents proclaim that HO-5 is the top of the line policy available in the United States. Unlike many of the other homeowners' insurance packages that only cover what is specifically listed, the HO-5 covers everything that isn't listed as exclusion and you can add endorsements to expand coverage. Both contents and the dwelling are covered against damage and loss. You can buy an HO-5 policy, or you can add riders to an HO-3 to bring it up to the same basic coverage.

Homeowners' 6 (HO-6, Condominium Insurance) This is a hybrid policy that is similar to HO-2 and HO-4. Designed specifically for condo owners, this type of coverage protects owners against content loss like the renters' policy and also covers the walls, ceiling, floors and other structural features in the home. Essentially, the policy covers personal liability and personal property under a named-peril umbrella for the structure.

Homeowners' 7 (HO-7, Mobile Home Insurance) is a policy specifically written to cover residences that fall into the manufactured home or mobile home classification. It is similar to the HO-3 coverage, with some limitations and exclusions; however this policy type is a comprehensive plan that covers many perils.

Homeowners' 8 (HO-8, Older Homes Coverage) is one of the common policies homeowners choose if they live in an older residence, especially if it would be a hardship to replace the property if severely damaged, or destroyed. Like other Named Perils Policies, HO-8 only covers specific items listed in the policy. The plan typically pays the actual cash value minus depreciation, because it would cost more to repair the dwelling and outbuildings than replace them in many instances.

Water damage is never covered under an HO-8 policy, or most other HO types, but you can add a rider that covers different kinds of water damage from overflowing a bathtub to damage caused by a flood. There may be coverage limits in any of the HO plans that affect the amount you can recover per claim, too. For example, theft, vehicle damage or vandalism may be limited to $1,000 per claim. It is very important to check exclusions and limitations carefully before buying or recommending an insurance policy.

Now, let's talk about flood insurance and whether you should invest in a rider or flood policy.

You probably noticed that none of the previously mentioned policies mention flood and water damage, although a non-peril based plan will provide water damage coverage, unless specifically excluded. Fortunately, there is another option for homeowners who live in flood-prone areas. The Federal Emergency Management Agency (FEMA) oversees and manages the National Flood Insurance Program (NFIP). While many people assume that FEMA funds are available to almost everyone, there are some restrictions.

For example, there is a narrow definition of what NFIP covers and what it will not. Loss initiated from a real flood is defined as an excess of water that covers at least two acres, or at least two properties, one owned by the homeowner who wants to file a claim. The initial cause may be a river overflowing, tidal waves coming on shore due to damaged flood gates or natural barriers, or even heavy rains that produce excessive runoff. The federal government building policy is not intended to replace content insurance, and this protection must be purchased individually.

A standard flood insurance policy is similar to any other peril-based policy. It only covers that specific peril and damage resulting in loss. As mentioned above, contents and liability are not covered unless you purchase content protection separately. Also, your NFIP policy covers replacement costs, but is not a guaranteed replacement cost policy. Actual cash value is calculated by deducting reasonable depreciation. For example, FEMA may deduct 10% to 15% of the value of wall-to-wall carpeting per year, depending on the quality of the flooring.

Whereas, homeowner policies may be value-based; flood insurance reimbursements are based on the cost to repair or replacement cost. So, for example, let's say that your home and contents are totally destroyed by a tornado and it costs you $175,000 to repair your home. If your homeowner’s policy had a maximum value of $250,000, you would receive $250,000. With NFIP, you would only receive the amount it takes to repair or replace based on the actual cost value up to the policy limit.

Determining how much coverage you need, can be tricky, but it is worth the time investment. Since NFIP policies never pay out more than the insurance plan limit, you must carefully consider how much it will cost you to repair or replace your property based on the same formulas that FEMA uses. Like auto insurance and medical insurance, if you establish a higher deductible, you will have lower payments. But, it may be hard to come up with enough money to recover from a flood situation if you set a deductible so high you cannot afford to complete the repairs.

Deciding how much coverage you need depends on your dwellings, or building property, your personal assets and uninsured items. When you talk with an insurance agent about coverage, ask plenty of questions and read the fine print. You may be surprised to learn that while drywall for walls and ceilings is covered in the basement, drywall isn't covered for elevated floors. And, furnaces and water heaters are covered under the building property, but refrigerators are not a covered appliance. Insurance usually covers the food freezers and food lost during an electricity outage.

In order to be eligible for replacement cost value (RCV) under a NFIP plan your residence must be a single-family home, and must be occupied at least 80% of the time by the homeowner. Additionally, building coverage must be 80% or more of the full replacement cost of the structure, or the maximum available under NFIP guidelines. It is important to meet all three of these requirements to qualify for RCV coverage.

When deciding how much coverage you should buy, keep in mind there are many items not covered under either personal property or building property. For example, window treatments, blinds, shutters and curtains are excluded along with most personal property like computers, kitchen utensils, plates, and other electronic equipment. You will be responsible for replacing most of these items and you shouldn't calculate replacement value when determining coverage limits. Talking with your mortgage broker or insurance agent may help you create an accurate estimate about how much it would cost to replace your home and covered contents if a flood event occurred in your neighborhood.

The reality is that most homeowners could benefit from flood insurance. The NFIP offers affordable policies for around $700 a year. And, when you consider that the average residential claim for flood damage a few years ago was more than $42,000, you can see the benefit far outweighs the costs. Currently the maximum coverage amount for flood related losses is $250,000 for buildings and $100,000 for eligible covered content, but you can buy additional coverage from private insurance agent. And, you can purchase policies with lower limits if you live in a low-risk area. There is also an option called the Fair Access to Insurance Requirements (FAIR) program designed for homeowners with unique challenges and risks. This state-mandated program helps high-risk homeowners gain access to affordable cover if they live in a flood-prone area or have had multiple FEMA claims.

Although many homeowners are underinsured in the United States, having insurance, is a wise choice. As a real estate agent working with potential home buyers, it is your responsibility to help them understand the benefits of protecting their assets.

Key Terms

Property Insurance

Provides protection against most risks to property, such as fire, theft and some weather damage.

COPYRIGHTED CONTENT:

This content is owned by Real Estate U Online LLC. Commercial reproduction, distribution or transmission of any part or parts of this content or any information contained therein by any means whatsoever without the prior written permission of the Real Estate U Online LLC is not permitted.

RealEstateU® is a registered trademark owned exclusively by Real Estate U Online LLC in the United States and other jurisdictions.